Debt collectors call at all hours. Credit reports show accounts you never opened. When consumer protection violations happen, having a top consumer protection attorney in your corner makes the difference between losing and winning.

At Bontrager Law, we’ve seen how local representation changes outcomes. Knowing your state’s laws, understanding your court system, and having relationships with judges and court staff gives you real advantages that national firms simply can’t match.

Why Local Courts and Laws Give You the Edge

State Laws Determine What You Can Recover

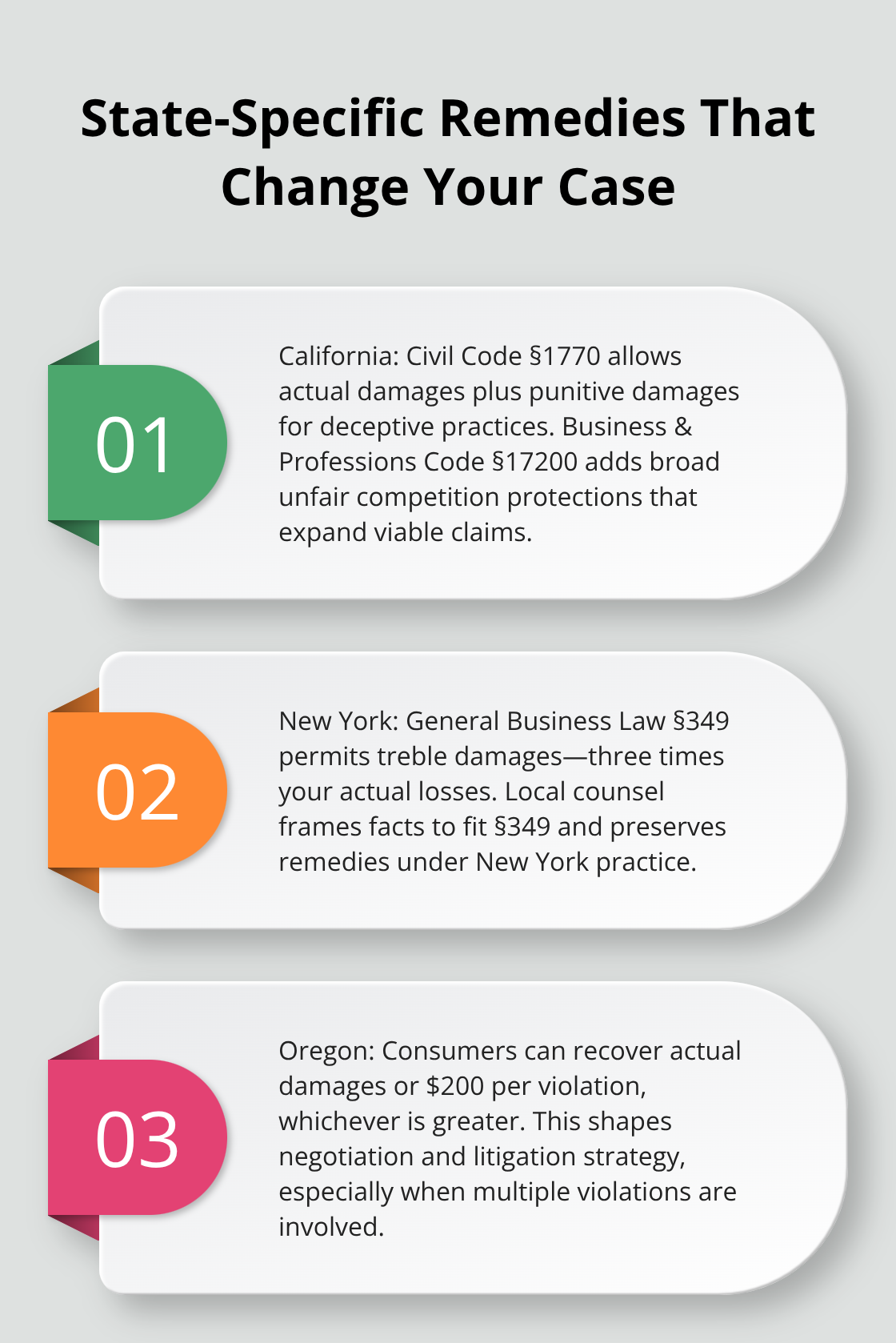

Every state writes its own consumer protection rules, and the differences matter enormously. California’s Civil Code Section 1770 allows actual damages plus punitive damages for deceptive practices, while Business and Professions Code Section 17200 provides broader unfair competition protections. New York’s deceptive acts statute, General Business Law Section 349, permits treble damages-three times your actual losses. Oregon offers actual damages or a $200 statutory minimum per violation, whichever is greater.

A national firm handling your case from across the country won’t know these distinctions or how judges in your specific courthouse interpret them. The Justice Index, which tracks access to justice across all states, found that only six states plus Washington, DC exceed two civil legal aid attorneys per 10,000 people below 200 percent of poverty. This shortage means most consumers face an uphill battle without representation that understands local terrain.

Court Procedures Vary by State and Jurisdiction

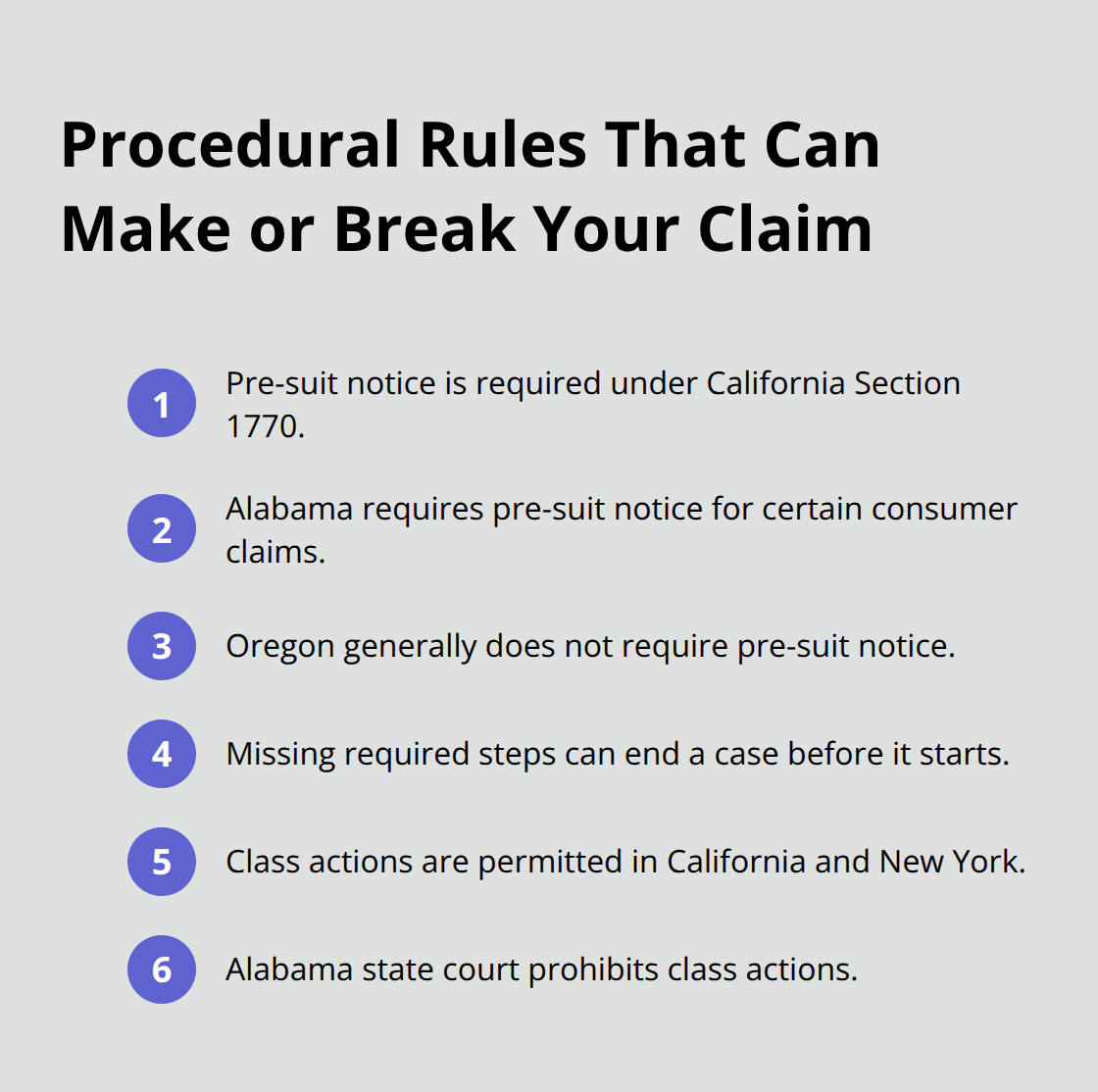

Court procedures matter just as much as substantive law. Some states require pre-suit notice before filing certain consumer claims, while others don’t. California’s Section 1770 requires pre-suit notice; Alabama does the same. Oregon generally does not. Missing these procedural requirements can kill your case before it starts.

Class actions, which allow multiple victims to sue together and recover more collectively, are permitted in California and New York but prohibited in Alabama state court. A local attorney knows which strategy works in your jurisdiction and which doesn’t.

Local Relationships Accelerate Your Case

The relationships built over years of practice in your local courthouse create real advantages. Judges develop preferences for how cases should be presented. Court staff understand filing quirks and timing issues that affect outcomes. When debt collectors or companies violate the Fair Debt Collection Practices Act or engage in identity theft, a local attorney familiar with your court’s judges can anticipate how they’ll respond to evidence and arguments. This familiarity translates to faster resolutions and stronger settlements.

Local Networks Speed Up Resources and Recovery

Local representation also accelerates access to resources. Your attorney can quickly contact state attorney general offices, local legal aid organizations, and regulatory agencies without the delays that come from out-of-state coordination. When you need a housing counselor certified by the U.S. Department of Housing and Urban Development or credit counseling from a National Foundation for Credit Counseling member agency, a local attorney has those referrals ready. These networks shrink your timeline and improve your overall recovery.

Understanding how your state’s laws work and how your local courts operate sets the foundation for effective representation. But knowing the law isn’t enough-you also need someone who recognizes the specific violations debt collectors commit in your region and can respond to them fast.

How Debt Collectors Exploit Your Lack of Local Knowledge

Debt Collectors Operate with Regional Playbooks

Debt collectors use regional strategies tailored to specific neighborhoods and courts. They identify which threats work in which areas, which enforcement patterns local judges tolerate, and which violations they can commit without facing consequences. A local attorney who has handled dozens or hundreds of debt collection cases in your area recognizes these patterns immediately and stops them. The Fair Debt Collection Practices Act prohibits abusive calls, false statements about debts, and threats of arrest for consumer debts, yet collectors violate these rules constantly because most people don’t fight back.

Speed Matters More Than You Think

When you work with someone who practices in your local courts regularly, you gain someone who knows exactly how your judges penalize violations and can move quickly to stop harassment before it escalates. Collectors call at 6 AM and 9 PM because they’re betting you won’t respond. They threaten wage garnishment on debts already past the statute of limitations because they’re betting you don’t know the law. A local attorney has the relationships with court staff and judges to file emergency motions for harassment injunctions without the delays that come from coordinating across state lines.

State attorney general offices in your jurisdiction often have ongoing investigations into collector practices. A local attorney connected to these offices can amplify your case and sometimes trigger broader enforcement actions that stop the same collector from harassing others.

Your State’s Laws Determine What You Actually Recover

Your state’s specific debt collection laws matter more than you realize. Some states allow you to recover actual damages plus attorney’s fees when collectors violate the FDCPA, while others cap recovery at statutory minimums. New York permits treble damages for deceptive debt collection practices under General Business Law Section 349. Oregon offers actual damages or $200 per violation, whichever is greater.

A collector calling you repeatedly after you’ve requested they stop in writing commits a violation in every state, but the remedies available depend entirely on where you live and which attorney understands your local court’s interpretation of those remedies. When collectors send false debt verification letters, misrepresent the age of debts, or threaten illegal actions, the speed with which your attorney responds determines whether you settle for pennies or recover full damages.

Local Filing Knowledge Prevents Costly Mistakes

Local representation means your attorney files responses within days, not weeks, because they’re already familiar with filing procedures and don’t waste time learning your courthouse’s quirks. A national firm handling your case remotely will miss filing deadlines that exist nowhere in writing but are understood by every attorney who practices there regularly. Your local attorney also knows which housing counselors certified by HUD and which credit counseling agencies accredited by the National Foundation for Credit Counseling operate in your area, meaning you get connected to legitimate recovery resources without the research burden.

The networks matter because they compress your timeline from months of searching to days of resolution. This foundation of local knowledge and relationships positions you to handle not just debt collection violations, but also the credit reporting errors and identity theft that often accompany collector harassment.

What Happens When Credit Reports, Identity, and Debt Collection Collide

Identity Theft Triggers a Chain Reaction

Credit reporting errors destroy finances faster than most people realize. The Federal Trade Commission found that identity theft affects millions of Americans annually, and when collectors weaponize false debt claims against victims, the damage compounds. A local attorney understands how these three violations intersect in your jurisdiction and moves to stop them simultaneously rather than treating them as separate problems. When a collector calls about a debt you never incurred, that call often stems from identity theft, which then poisons your credit report with fraudulent accounts.

Your state’s consumer protection laws determine what you recover, and timing determines whether you recover anything at all. California’s Civil Code Section 1770 allows you to pursue actual damages plus punitive damages against parties responsible for identity theft or false debt claims, but only if you file within the statute of limitations and follow pre-suit notice requirements. A local attorney knows exactly how many days you have and what notice must say. National firms miss these deadlines because they don’t practice in your courts regularly and don’t understand your state’s specific procedural traps.

Credit Bureau Disputes Require Local Standing

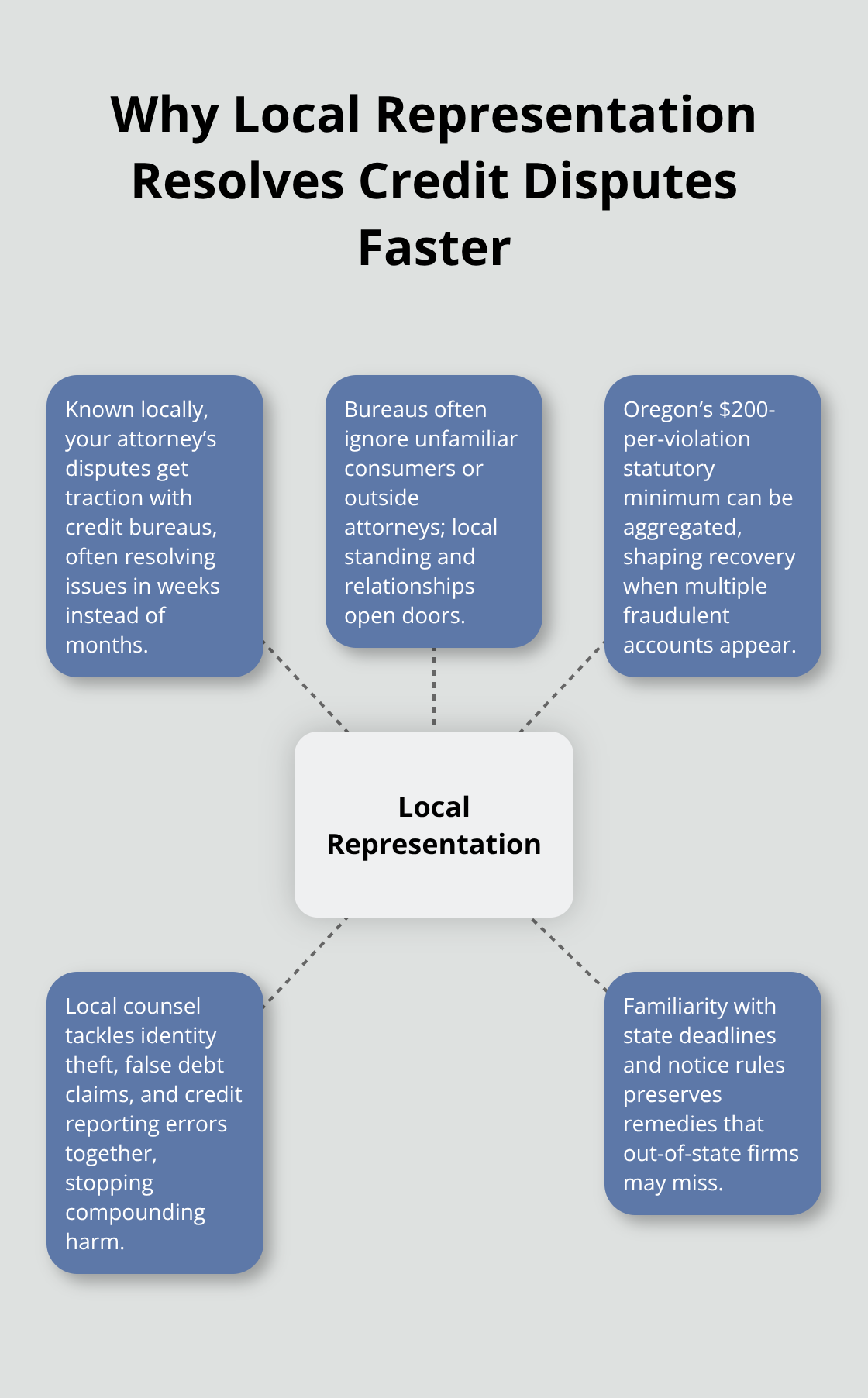

When identity theft occurs, the FTC recommends disputing fraudulent accounts with credit bureaus in writing, but disputes alone rarely work. Credit bureaus routinely ignore disputes from consumers they don’t know and dismiss them from attorneys they’ve never encountered. A local attorney with standing in your community and relationships with credit bureau legal departments resolves disputes in weeks instead of months.

Oregon allows actual damages or a $200 statutory minimum per violation, whichever is greater, meaning a single identity theft case with multiple fraudulent accounts can generate substantial recovery if handled by someone who knows how to aggregate violations under state law. Your local attorney understands these state-specific damage calculations and structures your claim accordingly.

Collectors Escalate Harassment When You Lack Representation

Unlawful debt collection harassment accelerates when collectors discover you lack local representation. They escalate calls, threaten illegal actions like arrest for consumer debt, and misrepresent the age of obligations because they’re betting you won’t fight back with someone who knows your court system. The Fair Debt Collection Practices Act prohibits abusive calls, false statements, and threats, yet collectors violate these rules constantly because enforcement requires an attorney who can file emergency motions and get judges to issue harassment injunctions without delays.

Your local attorney connects you with credit counseling agencies accredited by the National Foundation for Credit Counseling or certified housing counselors through the U.S. Department of Housing and Urban Development to address the underlying financial stress while litigation proceeds. This combination stops the immediate harassment and prevents future violations by the same collector.

Regional Collector Tactics Require Local Court Knowledge

Collectors operate with regional playbooks tailored to specific courts and neighborhoods, identifying which threats work locally and which judges tolerate certain violations. A local attorney who has handled dozens of debt collection cases in your courthouse recognizes these patterns immediately and files responses within days rather than weeks, preventing default judgments that destroy your ability to defend yourself.

The Justice Index found that most states lack standardized defenses for debt claims and that many defendants fail to respond to lawsuits because they lack representation. Your local attorney ensures you respond on time, present evidence of violations, and recover damages under your state’s specific statutory framework rather than accepting settlement offers that undervalue your claim. When collectors send false debt verification letters, misrepresent the age of debts, or threaten illegal actions, the speed with which your attorney responds determines whether you settle for pennies or recover full damages.

Final Thoughts

Debt collectors count on you standing alone. They bet you won’t know your state’s laws, won’t understand your local court system, and won’t have someone who can respond fast enough to stop the harassment. A top consumer protection attorney who practices in your jurisdiction changes that calculation completely. Your attorney knows which judges penalize violations harshly and which ones move quickly on emergency motions. They understand your state’s specific damage rules-whether you can recover treble damages, statutory minimums, or actual damages plus attorney’s fees. They have relationships with court staff, state attorney general offices, and credit counseling agencies that compress your timeline from months to weeks.

When collectors call at 6 AM threatening wage garnishment on debts past the statute of limitations, your local attorney recognizes the violation immediately and files a response within days, not weeks. Personalized representation means your attorney treats your case as their case, not as one file among thousands handled remotely from across the country. They know your courthouse’s filing quirks, understand how your judges interpret consumer protection statutes, and anticipate how opposing counsel will respond to evidence. This familiarity translates to faster settlements, stronger outcomes, and recovery that reflects what your state’s laws actually allow.

At Bontrager Law, we represent individuals across California in credit reporting errors, identity theft, unlawful debt collection, and related claims against banks, collectors, and large corporations. Contact njb.legal to discuss your situation and learn what your state’s laws allow you to recover.