A credit report error can feel like a financial setback, but the dispute process is just the beginning. Once the error is corrected, you need a clear strategy to rebuild your credit score and prevent similar problems from happening again.

We at Bontrager Law have helped many people navigate rebuilding credit after dispute and move forward with confidence. This guide walks you through the practical steps to monitor your report, strengthen your credit profile, and protect yourself going forward.

Understanding Your Credit Report After a Dispute Resolution

After the credit bureau investigates your dispute, the furnisher (the company that reported the information) has 30 days to respond. According to the CFPB, if they confirm the information is wrong or cannot verify it, they must notify all three bureaus-Experian, Equifax, and TransUnion-to update or remove it from your file. The bureaus then update your reports, which means the inaccurate item disappears or gets corrected. This is when you’ll see real movement on your credit profile. However, if the furnisher verifies the information is accurate, the item remains on your report. In that case, you have the right to add a consumer dispute statement explaining your position. This statement stays in your file and appears whenever someone pulls your report, which can help lenders understand your side of the story.

Verify the Dispute Outcome Within 45 Days

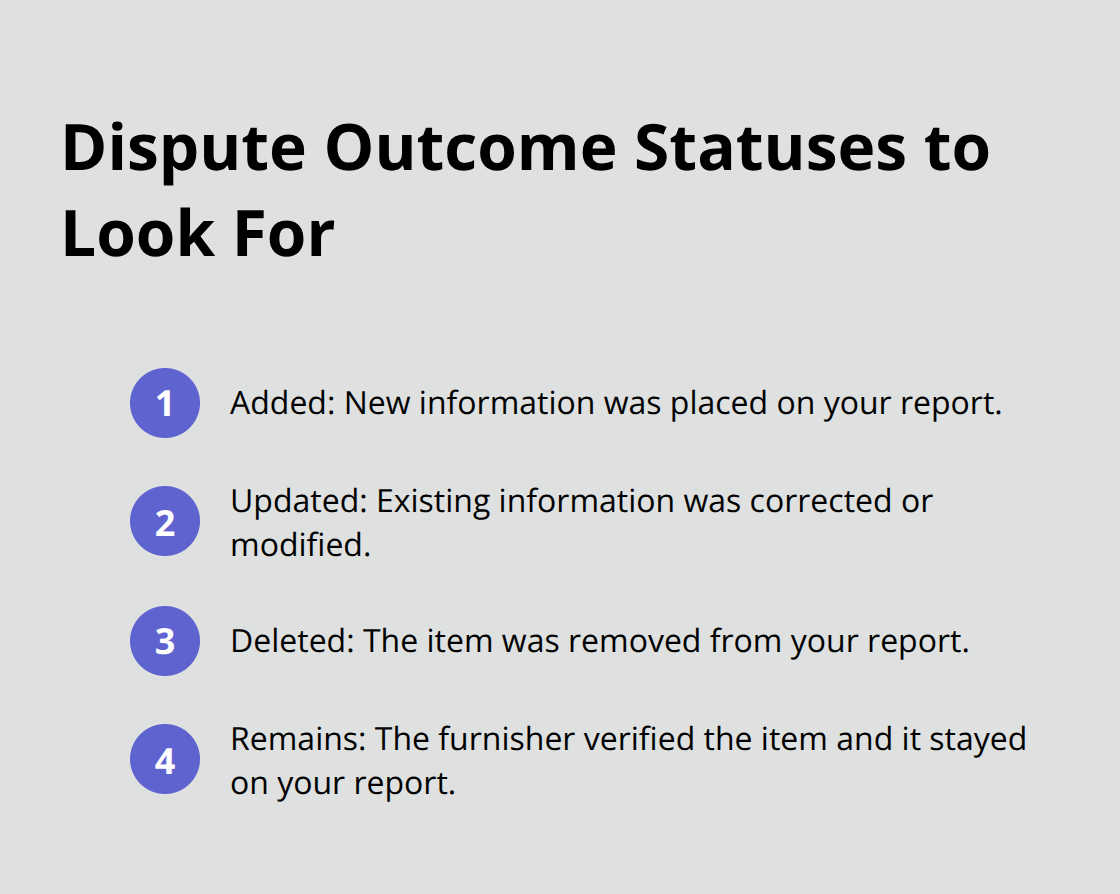

Pull your credit reports from all three bureaus within 45 days of filing your dispute. According to Experian, most disputes resolve in about 30 days, though complex cases can take up to 45 days. You can access one free report annually from each bureau through AnnualCreditReport.com, or check Experian’s free report anytime. Look specifically at the status of the disputed item-possible outcomes include Added, Updated, Deleted, or Remains. If the item was deleted or corrected, that represents your win. If it remains, contact the furnisher directly with additional documentation.

Do not wait months to check; the sooner you verify the outcome, the sooner you can adjust your credit-building strategy. Many people file a dispute and never actually confirm whether it worked, which represents a critical mistake.

Monitor Your Score After Resolution

Removing negative information can improve your score, though the impact depends on what was removed. Late payments, inquiries, and delinquencies significantly affect your FICO score, so correcting these items typically produces noticeable improvements. Conversely, removing certain positive items-like an old account with good payment history-might slightly lower your score because you lose that historical record. Start monitoring your score after the dispute resolves so you can see whether corrections actually moved the needle. This data helps you understand which negative items were dragging down your score most, informing your next steps for rebuilding. With your dispute resolved and your reports verified, you can now focus on the active work of strengthening your credit profile through strategic debt management and consistent payment behavior.

Rebuilding Credit After Dispute

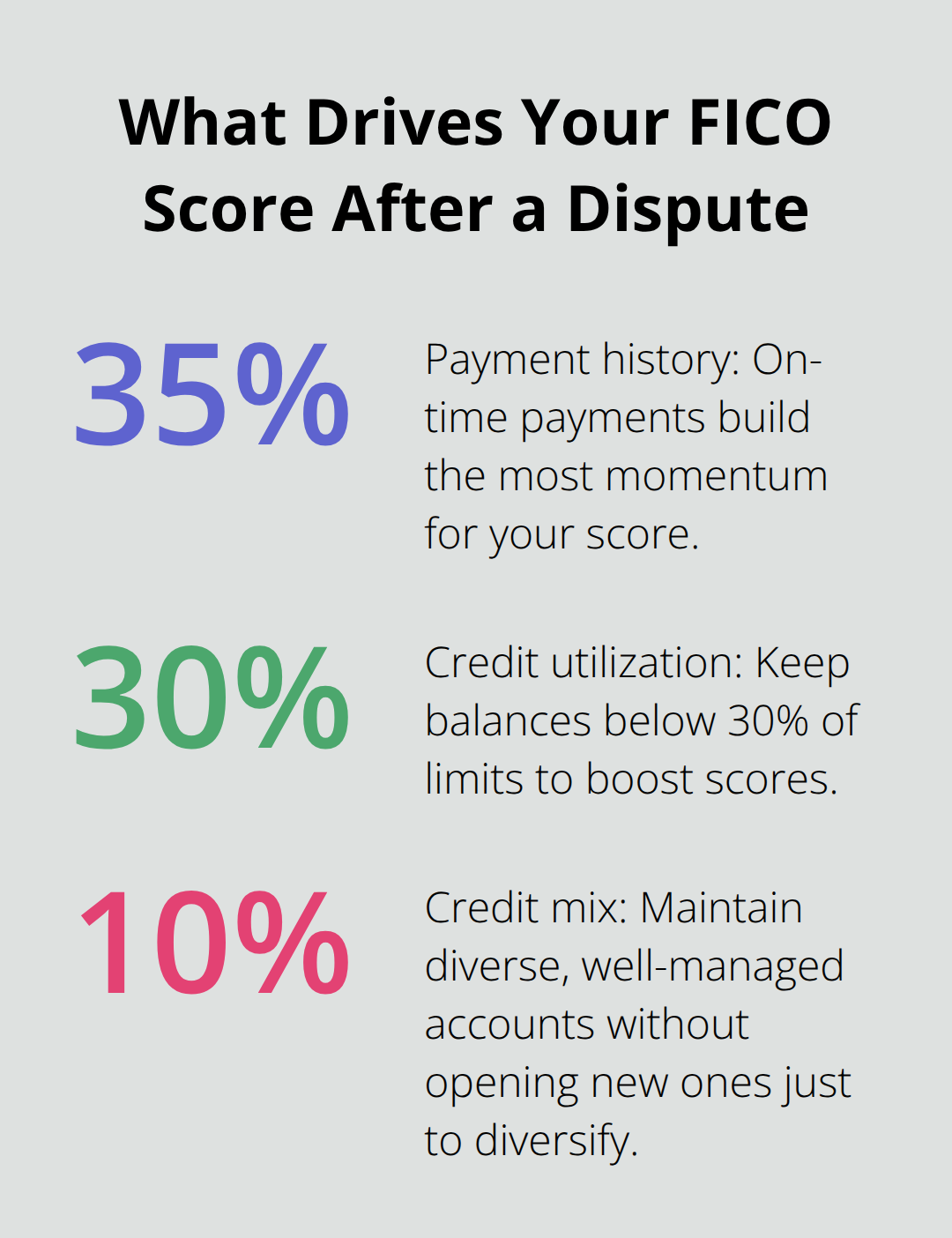

Once your dispute resolves and inaccurate items are removed from your report, your credit score won’t automatically bounce back overnight. The removal itself is just the foundation. What matters now is what you do next. If you had late payments, high balances, or delinquencies removed, you’ve eliminated some of the heaviest weight dragging down your score. According to FICO’s scoring model, payment history accounts for 35 percent of your score, so correcting errors in this category can produce meaningful gains.

Pay Down Your Balances First

Your credit utilization ratio-the percentage of available credit you’re actually using-accounts for another 30 percent of your score. This is where aggressive action pays off. If you have credit cards carrying balances, focus on paying them down to below 30 percent of your limits. Someone with a $5,000 limit should try to keep their balance under $1,500. This shift alone can produce a 50 to 100 point improvement in your score within a billing cycle or two. Don’t spread payments across multiple cards hoping to look better; instead, concentrate your payments on the highest-utilization accounts first.

Establish Consistent On-Time Payments

Once you’ve tackled utilization, shift your attention to establishing consistent on-time payments moving forward. Every single payment you make on time from this point forward strengthens your profile. Set up automatic payments for at least the minimum on every account, or better yet, the full balance if possible. This removes the human error of forgetting a due date. Your payment history going forward will gradually outweigh the damage from the error you just corrected. A person who makes 24 consecutive on-time payments will see their score trending upward noticeably compared to someone with sporadic payments.

Maintain Your Credit Mix Strategically

The final piece involves your credit mix, though this should not drive your decisions. Credit mix accounts for only 10 percent of your score, so don’t open new accounts just to diversify. Instead, if you already have multiple types of credit (credit cards, an auto loan, a mortgage), keep those accounts open and active. Closing old accounts actually hurts your score by reducing your total available credit and shortening your average account age. The longer your accounts have been open, the better. An account that has been open for ten years with positive payment history is far more valuable than a brand-new credit card. If you have no credit history beyond credit cards, a secured credit card or a credit-builder loan from a credit union can help, but only pursue this if you genuinely need to build profile diversity.

The mistake most people make is trying to fix everything at once. Focus first on utilization, then on consistent on-time payments, and let the credit mix develop naturally through accounts you already maintain. This sequenced approach produces faster, more sustainable score improvement than scattered efforts across multiple fronts. With these fundamentals in place, you can now turn your attention to protecting yourself from future errors and ensuring your credit file stays accurate.

Protecting Yourself from Future Credit Reporting Errors

The dispute you just resolved took time and effort, but the real protection comes from catching errors before they damage your score. Check your credit reports from Experian, Equifax, and TransUnion at least once every twelve months using AnnualCreditReport.com, which provides free annual access to all three bureaus. Better yet, pull reports every four months by rotating through the bureaus, so you review your file continuously throughout the year. Equifax currently offers six free reports annually through 2026, giving you even more opportunities to spot problems early.

Spot Inaccuracies Early

When you review your reports, look for unfamiliar accounts, incorrect balances, wrong payment statuses, and duplicate entries. A Reddit user who disputed a Chase credit card charge saw their score drop 100 points when the dispute flag appeared on their Experian and TransUnion reports, illustrating how quickly inaccuracies cascade across multiple bureaus. Early detection prevents this damage from accumulating in the first place.

Document Everything in Writing

Every conversation with a creditor or credit bureau requires written confirmation afterward. If you call a lender to dispute a charge or correct account information, send a follow-up email summarizing what was discussed, who you spoke with, and what was agreed upon. Keep copies of all dispute letters, supporting documents, and responses from bureaus and furnishers in a dedicated folder. The CFPB recommends using certified mail with return receipt when you dispute by mail, which creates an official record that your dispute was received and when. Save screenshots of online dispute submissions, including confirmation numbers and dates.

This documentation becomes invaluable if an error reappears on your report or if a furnisher claims they never received your dispute. When the furnisher has 30 days to investigate according to CFPB guidelines, your documentation proves the timeline and prevents disputes from falling through the cracks.

Know Your Rights Under the Fair Credit Reporting Act

The Fair Credit Reporting Act gives you specific rights that most people never exercise. You can demand that furnishers verify the accuracy of information before they continue reporting it to the bureaus. If a furnisher cannot verify an account is yours or cannot validate the balance they’re reporting, they must remove it or correct it within 30 days of your written request. You also have the right to request that the bureaus place a fraud alert on your file if you suspect identity theft, which alerts lenders to contact you before opening new accounts in your name. A security freeze goes further, completely blocking access to your credit file unless you temporarily unfreeze it. This prevents new accounts from being opened without your direct approval. Additionally, if a furnisher continues reporting information you’ve disputed and the bureau places a notice on your file, you can request that the bureau notify past recipients of your dispute statement within the past six months, or two years if the report went to employers. Understanding these tools means you control what gets reported about you rather than simply reacting to errors.

Final Thoughts

Rebuilding credit after a dispute marks a shift from reacting to errors toward actively managing your financial identity. Once your dispute resolves and incorrect items vanish from your file, you’ve removed the obstacles that held back your score, but the real progress happens in the months that follow when consistent on-time payments and lower credit utilization prove to lenders that you’re reliable. Accurate credit reports directly affect your ability to qualify for loans, secure favorable interest rates, rent housing, and land certain jobs-correcting errors on your report means reclaiming access to financial opportunities that inaccuracies had blocked.

A person who removes a false late payment or fraudulent account might suddenly qualify for a mortgage they couldn’t get before, or refinance existing debt at a significantly lower rate. Over the life of a loan, this difference translates to thousands of dollars in savings. Taking control of your credit future means staying vigilant through regular report reviews, documenting all communications with creditors and bureaus, and understanding the rights you hold under the Fair Credit Reporting Act.

If you encounter complex disputes, identity theft, or furnishers who refuse to correct inaccurate information, professional guidance can make the difference. We at Bontrager Law represent individuals across California in credit reporting disputes and can clarify whether your situation warrants legal action. Visit Bontrager Law to request a free case review and learn what options are available to you.