Your credit report shapes your financial life. Errors on that report-whether from data mistakes, identity theft, or collection agency violations-can tank your score and lock you out of loans, housing, and jobs.

At Bontrager Law, we help California residents fight back against these reporting errors and recover damages from the companies responsible. This guide walks you through your rights and how legal action can fix your credit.

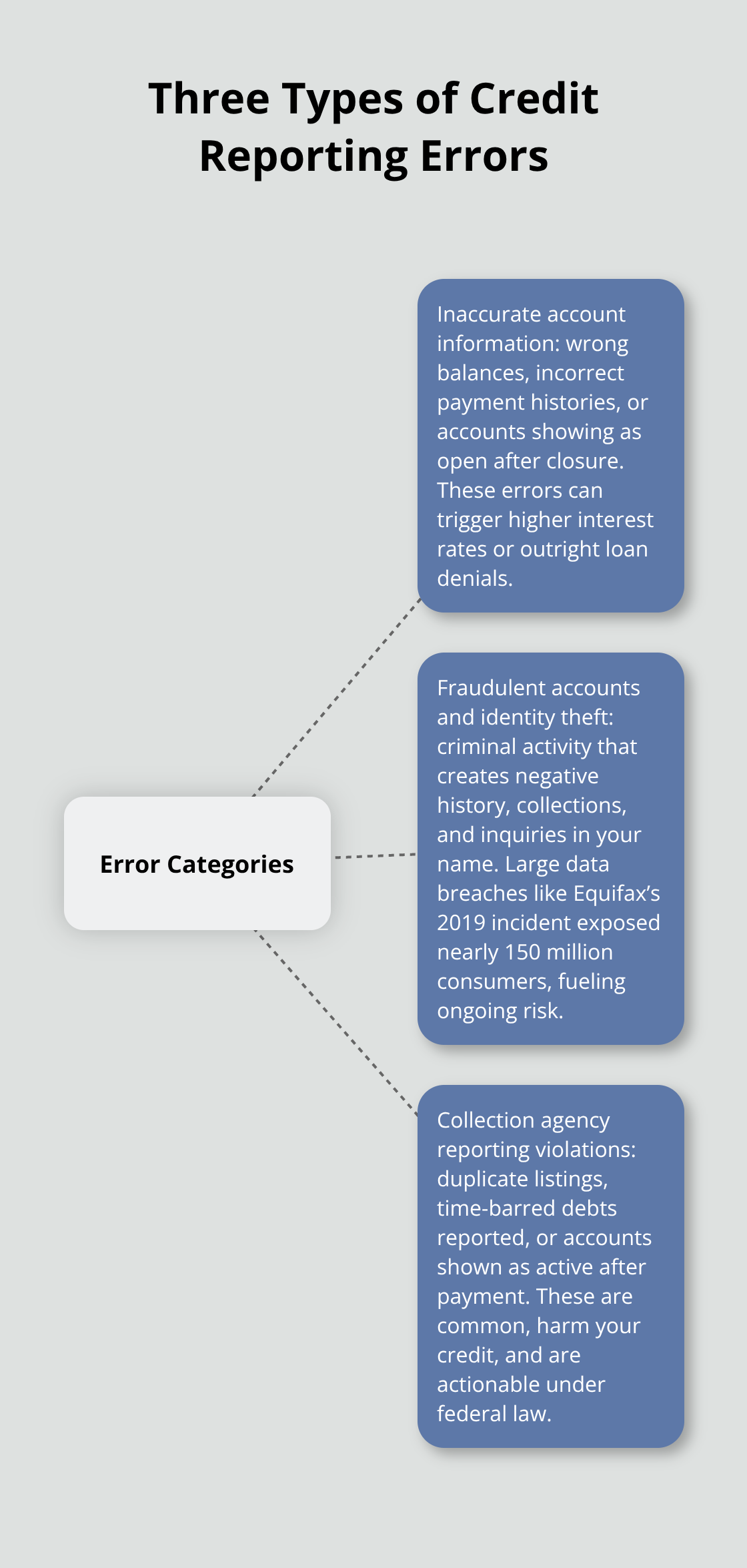

Common Credit Reporting Errors and How They Harm You

Inaccurate Account Information Damages Your Score

Credit reporting errors fall into three distinct categories, and each one hits differently. Inaccurate account information-wrong balances, incorrect payment histories, accounts listed as open when you closed them-appears on roughly one in five credit reports according to data from the Consumer Financial Protection Bureau. These mistakes cost you real money through higher interest rates or outright loan denials. A single error showing a 30-day late payment can drop your score by 100 points or more, making the difference between qualifying for a mortgage and getting rejected.

The bureaus-Equifax, Experian, and TransUnion-process millions of updates daily, and their systems frequently misfile information or fail to update closed accounts. You need to pull your credit reports from all three bureaus and compare them carefully. Look for accounts you don’t recognize, balances that don’t match your statements, and payment histories that contradict your actual payment records. Document every discrepancy with dates and supporting evidence from your own financial records.

Fraudulent Accounts and Identity Theft Create Serious Threats

Fraudulent accounts and identity theft represent a more serious threat because they’re not just errors-they’re crimes that can take months to unravel. When someone opens credit accounts in your name, those accounts generate negative payment history, collections, and inquiries that tank your score while the fraudster runs up debt. The Equifax data breach of 2019 exposed personal information for nearly 150 million consumers, and similar breaches continue creating vulnerable targets.

If you spot unfamiliar accounts, collection agency mistakes, or accounts reporting late payments you never made, act immediately by contacting the credit bureaus and the creditors involved. Send written disputes using certified mail to both the bureaus and the creditors who supplied the false information. The bureaus must investigate within 30 days and correct verified errors.

Collection Agency Violations Demand Legal Action

Collection agency reporting violations-accounts listed multiple times, debts reported after the statute of limitations expired, accounts showing as active when they’re actually paid-are particularly common and actionable violations. These violations harm your credit while violating federal law, and you have the right to challenge them through formal disputes and legal claims. Understanding which violations apply to your situation requires careful review of your reports and the applicable laws protecting your credit rights.

Your Rights Under California and Federal Credit Laws

The Fair Credit Reporting Act Establishes Your Foundation

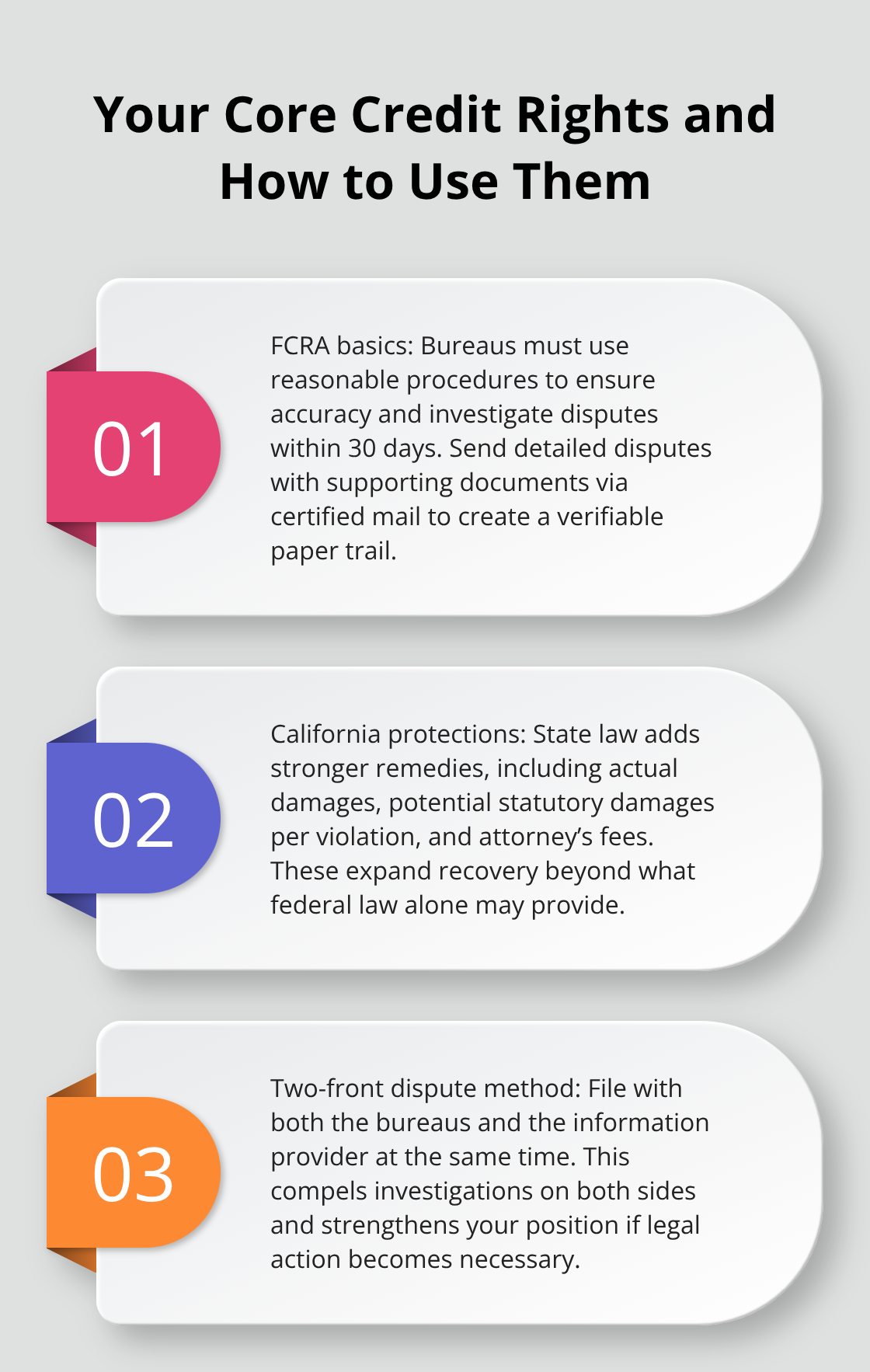

The Fair Credit Reporting Act gives you concrete rights that most people don’t know they have. Under federal law, credit bureaus must maintain reasonable procedures to verify accuracy, and they must investigate disputes within 30 days. If you dispute an error, send a detailed letter to Equifax, Experian, and TransUnion with copies of supporting documents using certified mail. The bureaus must respond and correct verified errors or add a dispute note to your file.

You’re also entitled to one free credit report from each bureau every 12 months through Annual Credit Report, the official source-avoid sites claiming free reports with hidden fees.

California’s Stronger Consumer Protection Framework

California layers additional protections on top of federal law through its Unfair, Deceptive, and Abusive Practices statutes, which provide stronger remedies than federal rules alone. State law allows you to recover actual damages, statutory damages up to $1,500 per violation in some cases, and attorney’s fees when companies violate your rights. This matters because violations that might seem minor under federal law can trigger real financial recovery under California standards.

How to Dispute Errors on Two Fronts

Disputing errors requires action on two fronts simultaneously. Send your dispute to the credit bureaus and simultaneously to the creditor or lender that supplied the wrong information-they must investigate and report back to the bureaus. Document everything: keep copies of your dispute letters, the certified mail receipts, and all responses. If the bureaus don’t correct errors within 30 days, you can request a dispute statement be added to your file for future reports.

The information provider-the bank, collection agency, or creditor-must also verify the accuracy of what they reported. Many people stop after disputing with the bureaus, but that’s incomplete. If the information provider fails to investigate or continues reporting inaccurate information, that violation opens a legal claim you can pursue. California residents with reporting errors benefit from understanding both federal credit protection law and California’s broader consumer protection framework, since California law often provides pathways to recovery that federal law alone doesn’t offer.

Building Your Case for Legal Action

When disputes with bureaus and creditors stall, legal representation becomes necessary. An attorney who understands both federal and state credit laws can identify which violations apply to your situation, assess the strength of your claims, and determine what damages you might recover. The next section explains how legal action against credit bureaus and collectors actually works and what compensation you can realistically pursue.

How a Credit Protection Attorney Recovers Damages From Credit Violations

Federal and State Laws Create Real Financial Exposure

When credit bureaus and collection agencies violate your rights, disputes alone rarely force corrections. An attorney shifts the dynamic by making violations costly for the companies responsible. Federal law under the Fair Credit Reporting Act allows you to recover actual damages-the real financial harm from denied loans, higher interest rates, or identity theft costs. California law adds statutory damages of up to $1,500 per violation under unfair and deceptive practices statutes, meaning a company that reports false information to all three bureaus faces exposure far beyond what the violation itself cost you.

Past settlements illustrate the scale: Rose v. Bank of America recovered $32 million in credit-related violations, and Pastor v. Bank of America settled for $1.645 million in Fair Credit Reporting Act claims. These outcomes happen because attorneys force companies to face real financial consequences for ignoring consumer rights.

How Legal Representation Stops Harassment and Accelerates Resolution

When you hire representation, debt collectors must cease contacting you directly and instead communicate through your attorney-a federal requirement that immediately stops harassment and gives you control over communications. Collectors and bureaus often settle disputes faster when they know an attorney is involved because litigation costs and potential damages exceed what they’d spend resolving your claim.

An attorney also identifies violations most people miss: accounts reported after the statute of limitations expired, duplicate reporting of the same debt across multiple collection agencies, and failures to investigate disputes within required timeframes. These technical violations carry statutory damages even if your credit score already recovered, because the law penalizes companies for violating procedures, not just for causing measurable financial harm.

Building Your Case With Documentation and Legal Analysis

Building a strong case requires documenting your credit reports from all three bureaus, your dispute letters and their responses, communications with collectors, and evidence of the actual impact-loan denials, rate increases, or identity theft costs. Your attorney reviews these materials against applicable laws and identifies which companies violated which requirements.

The Fair Credit Reporting Act requires bureaus to maintain reasonable procedures to verify accuracy and to investigate disputes within 30 days; failures here are violations. California’s consumer protection framework imposes additional obligations: companies must not engage in unfair, deceptive, or abusive practices, and California courts interpret this broadly. An attorney determines whether to pursue settlement negotiations or file suit.

Settlement Negotiations and Litigation Strategy

Many cases settle during pre-litigation negotiations once attorneys present the legal violations and potential damages-companies recognize that defending litigation costs more than paying reasonable settlements. If negotiations stall, filing a lawsuit in California state court or federal court opens discovery, allowing your attorney to obtain internal documents from credit bureaus and collectors showing how widespread violations were or whether companies ignored consumer complaints.

Class actions also apply when violations affect many consumers identically, consolidating leverage and making it economical for your attorney to pursue claims that individual damages alone wouldn’t justify. Your role shifts from fighting alone to working with someone who understands how to value your claim, pressure companies to settle, and litigate if necessary.

Final Thoughts

Credit reporting errors don’t fix themselves, and waiting costs you money every month through higher interest rates, denied loans, and damaged financial opportunities. Acting quickly matters because the 30-day investigation window under federal law starts when you file your dispute, and delays mean months of additional damage to your creditworthiness. If you spot fraudulent accounts or collection violations, contact the bureaus and creditors immediately with written disputes using certified mail.

When disputes stall or companies ignore your rights, a California credit protection attorney shifts the entire dynamic by stopping debt collectors from contacting you directly and forcing companies to take violations seriously. Legal representation identifies claims you wouldn’t spot alone and understands which violations carry statutory damages under California law, how to value your actual losses from denied credit or identity theft, and when settlement negotiations make financial sense versus litigation. The difference between handling this alone and having representation often means the difference between accepting a partial correction and recovering real damages from the companies responsible.

Contact Bontrager Law to discuss your credit situation and explore what legal action might recover for you. We represent California residents in credit reporting disputes, identity theft claims, and unlawful debt collection cases with personalized representation starting with a free case review.