A mistake on your credit report can cost you thousands in higher interest rates and denied loans. Yet millions of Americans have inaccurate listings they don’t know how to challenge.

We at Bontrager Law help people dispute inaccurate listings and reclaim their financial standing. This guide walks you through the process, your rights, and what happens when bureaus refuse to correct errors.

What’s Actually Wrong on Your Credit Report

Types of Inaccurate Information

Credit report errors fall into distinct categories, and knowing which type you’re fighting matters. Late payments that weren’t actually late, accounts opened in your name that you never authorized, duplicate listings of the same debt, and incorrect personal information like a wrong address all appear regularly on credit reports. A single error can tank your score by 100 points or more depending on what’s listed. If a paid-off account shows as still open, or if a collection account belonging to someone else appears under your name, lenders see higher risk and charge you more.

The Real Cost of Errors on Your Financial Life

Mortgage rates climb when your score drops, credit card approvals get denied, and some employers now check credit reports before hiring, so an error can literally cost you a job. Late payments stay on your report for seven years and bankruptcies for ten, which means correcting them quickly prevents years of financial damage. One in five Americans has errors on at least one of their three credit reports, and roughly 5 million consumers dispute inaccuracies annually, according to the Consumer Financial Protection Bureau.

How Errors Make Their Way Onto Your Report

Data furnishers-banks, credit card companies, landlords, and collection agencies-report account information to the bureaus monthly. When they submit data carelessly or use outdated systems, mistakes slip through. Identity theft remains a serious culprit; criminals open accounts in your name and the fraudulent activity lands on your report. Mergers and system migrations also introduce errors when companies transfer data between platforms. The bureaus themselves sometimes misfile information or fail to update accounts when creditors notify them of corrections.

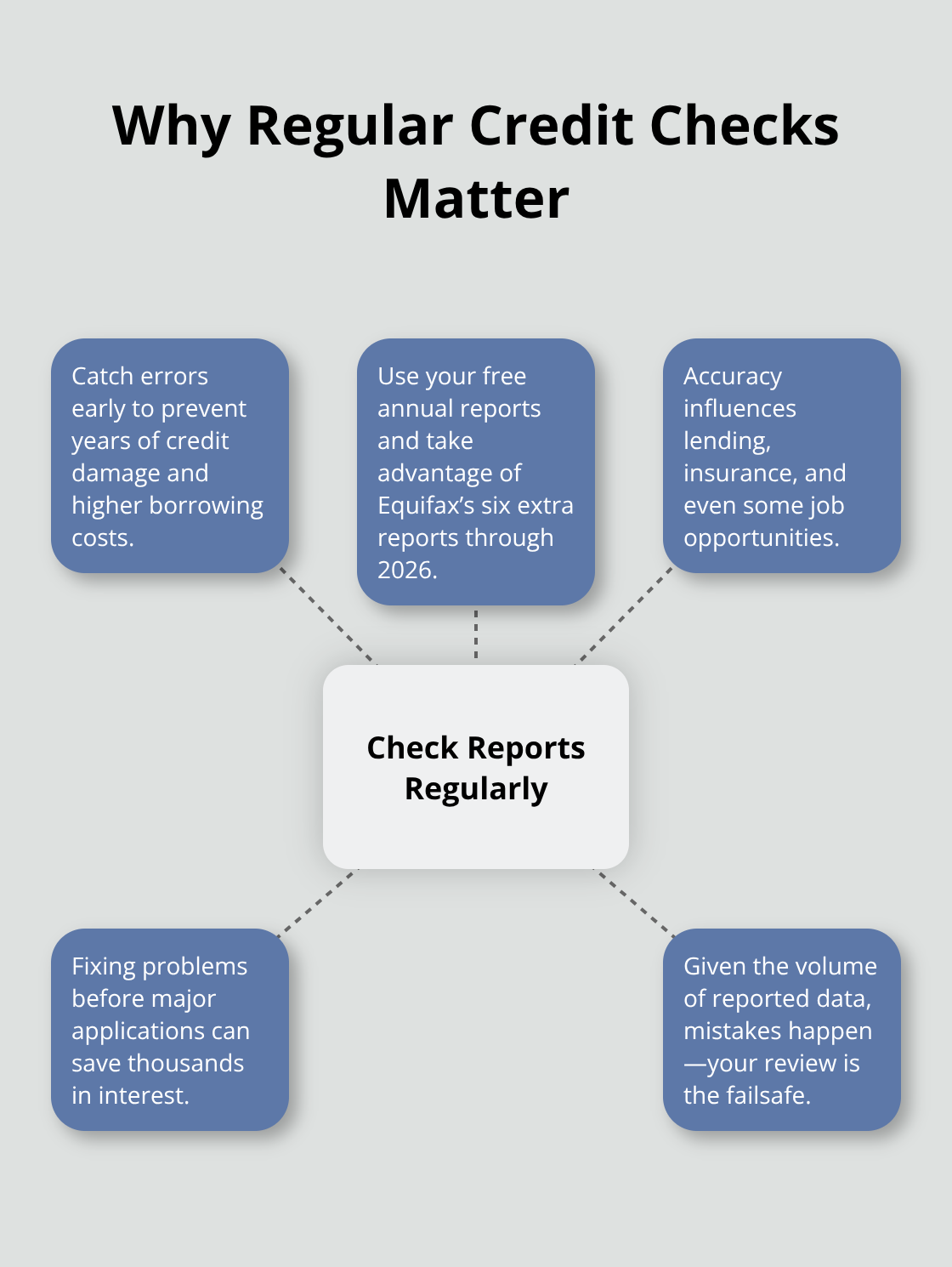

Why You Must Check Your Report Yourself

The burden falls on you to catch these mistakes, and most people never check their reports until they apply for a loan and get denied. You’re entitled to one free credit report annually from each bureau through AnnualCreditReport.com, and through 2026, Equifax offers six free reports per year. Checking your report regularly is the only way to spot errors before they damage your financial standing for years.

Equifax, Experian, and TransUnion handle billions of data points monthly, so mistakes happen-but you control whether you find them early or discover them too late.

Now that you understand what errors look like and why they happen, the next step is learning exactly how to identify the specific mistakes on your own report and prepare to challenge them.

How to Find and Challenge Your Credit Report Errors

Get Your Reports and Spot the Mistakes

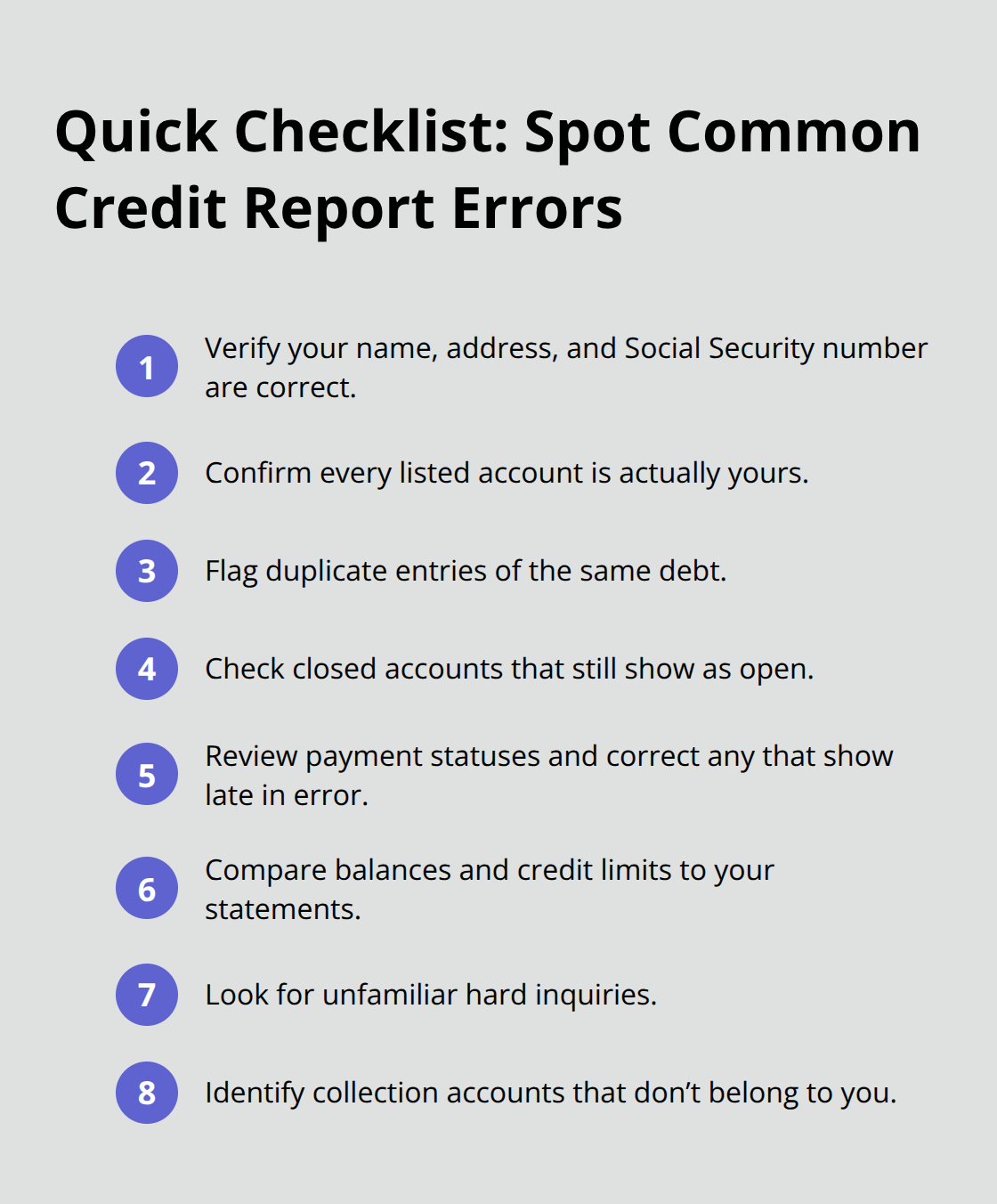

Start by obtaining your actual credit report, not a credit score. AnnualCreditReport.com gives you one free report from each bureau yearly, and Equifax provides six free reports through 2026 when you visit their website or call 1-866-349-5191. Download all three reports from Equifax, Experian, and TransUnion because errors appear on some bureaus but not others. Open each report and scan the personal information section first-verify your name, address, Social Security number, and employment history match your actual records. Then move to the accounts section and confirm you recognize every listed account.

Look for duplicate entries where the same debt appears twice, accounts showing as open when you closed them, and payment statuses marked late when you paid on time. Circle or flag anything that doesn’t match your records. This takes time, but one mistake could cost you tens of thousands in higher mortgage rates over 30 years.

Write Your Dispute Letter to the Bureau

Once you’ve identified errors, write a dispute letter to each bureau reporting the inaccuracy. Send it by certified mail with return receipt-this proves the bureau received your dispute and creates a paper trail necessary if litigation becomes required. Your letter should list each error with the account number, explain clearly why it’s wrong, and state exactly what you want removed or corrected. Include copies of supporting documents like bank statements, payment receipts, or correspondence proving the information is inaccurate, but never send originals. The bureau has 30 days to investigate and must contact the data furnisher-the creditor or collection agency that reported the item.

Understand What Happens During Investigation

If the furnisher confirms the information is inaccurate or cannot verify it, the bureau must correct your report and send you written results. If the bureau deems your dispute frivolous because you provided insufficient detail, they’ll notify you within five business days, so be specific and thorough. After the bureau responds, also dispute directly with the furnisher using the same letter format sent by certified mail. Many furnishers ignore bureau investigations but respond when contacted directly by consumers. If either the bureau or furnisher corrects the error, monitor your reports for 30 to 60 days to confirm the change appears across all three bureaus.

What to Do When Bureaus Refuse to Act

Sometimes bureaus reject your dispute or furnishers refuse to correct errors despite clear evidence of inaccuracy. When this happens, you have additional options available to protect your rights and force corrections onto your report.

What Happens After You File a Dispute

The 30-Day Investigation Window

Once the bureau receives your certified mail dispute, they must forward your claim and supporting documents to the data furnisher within two business days and investigate the information. The furnisher then has 30 days to respond to the bureau with their findings. This timeline matters because the bureau cannot ignore your dispute or delay indefinitely. If the furnisher confirms the information is wrong or cannot verify it within 30 days, the bureau must correct your report and send you written results at no charge. You’ll also receive a free updated copy of your credit report showing the correction, separate from your annual free report.

When Furnishers Claim Information Is Accurate

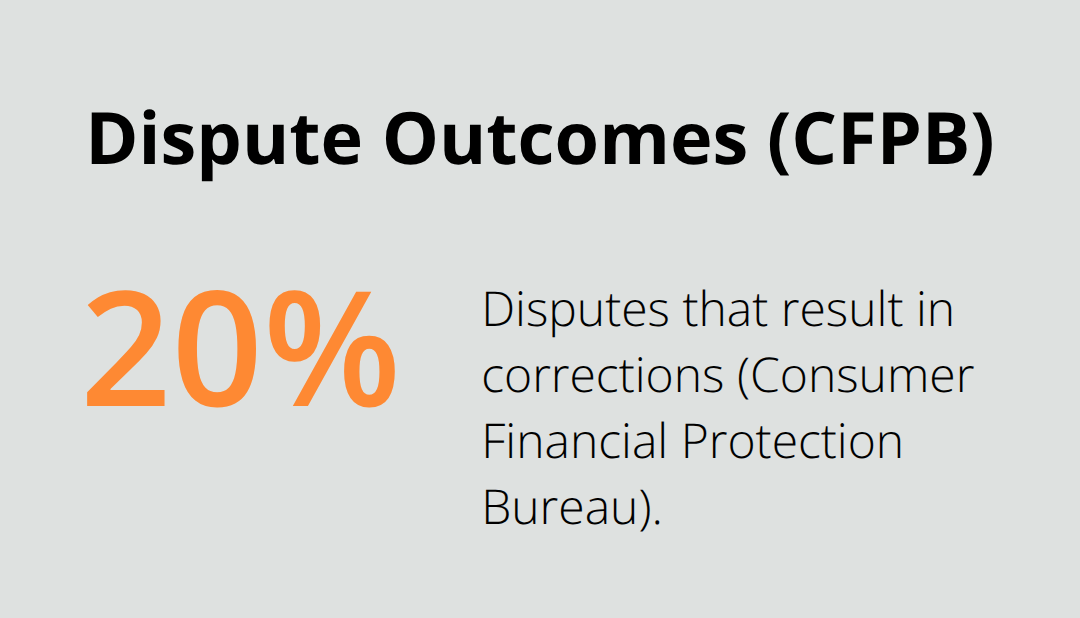

If the furnisher claims the information is accurate and the bureau agrees, the investigation closes without correction. This is where most disputes stall. The furnisher has no financial incentive to admit mistakes, and many use outdated systems that cannot verify whether an account belongs to you or was reported correctly. The Consumer Financial Protection Bureau reports that roughly 20 percent of disputes result in corrections, meaning four out of five disputes are either rejected or partially resolved.

Adding a Dispute Statement to Your File

Your rights don’t end when the bureau says no. If you disagree with the investigation results, you can add a dispute statement to your file explaining your position in up to 100 words. This statement appears on future credit reports when lenders pull your file, giving you a chance to tell your side. You can also file a complaint with the CFPB if the bureau or furnisher violated fair credit reporting laws.

Contacting the Furnisher Directly

Contact the furnisher directly using certified mail if you haven’t already. Many furnishers ignore bureau investigations but take consumer complaints seriously because they fear regulatory scrutiny. If the furnisher continues reporting the disputed information after you contact them, they must inform the bureau that you’re disputing it. When bureaus still refuse to correct clear errors despite overwhelming evidence, you may have grounds for legal action under the Fair Credit Reporting Act.

Pursuing Legal Action

At that point, we at Bontrager Law can review whether the bureau or furnisher violated your rights and whether pursuing a claim makes financial sense for your situation.

Final Thoughts

Disputing inaccurate listings on your credit report is your legal right under the Fair Credit Reporting Act, and the process works when you follow it correctly. You have the power to challenge errors, demand investigations, and force corrections across all three bureaus. The law requires furnishers to investigate within 30 days and bureaus to update your report if information is wrong or unverifiable.

Most people handle disputes alone and succeed, but some face furnishers who refuse to correct clear errors or bureaus that dismiss legitimate claims without proper investigation. A single error can cost you tens of thousands in higher interest rates, denied credit applications, or lost job opportunities. The Fair Credit Reporting Act allows you to recover damages and attorney fees if bureaus or furnishers violate your rights, but only if you understand which violations occurred and how to prove them.

If you’ve disputed errors and hit a wall, or if you suspect a furnisher is deliberately ignoring your dispute, contact us for a free case review to clarify your options. We represent California consumers in credit reporting disputes and related claims against banks, collectors, and large corporations. A conversation with our team can show you whether your situation qualifies for representation and what recovery might look like for your case.