Your credit report shapes your financial life, yet many California residents don’t understand their rights under the Fair Credit Reporting Act. Violations happen regularly-from inaccurate information staying on your report to creditors pulling your credit without permission.

At Bontrager Law, we’ve seen how FCRA obligations in California get ignored by businesses and creditors. This guide walks you through what the law protects, what you can do about violations, and how to hold companies accountable.

What the FCRA Protects and Why California Residents Need to Know

The Federal Law That Governs Your Credit Information

The Fair Credit Reporting Act became federal law in 1970 and remains the backbone of consumer credit protection across all 50 states, including California. The FCRA governs how credit bureaus, employers, landlords, and creditors collect, share, and use your credit information. Without this law, companies could pull your credit report for any reason, share your financial data freely, and leave errors on your record indefinitely. California residents benefit from these federal protections, though many don’t realize how broad they actually are or what happens when businesses ignore them.

Who Must Follow FCRA Rules

The law covers credit bureaus like Equifax, Experian, and TransUnion, but also tenant screening companies, medical information providers, and background check services. If a company uses information about you to make a decision that harms you-denying credit, refusing to hire you, or rejecting your rental application-they must follow strict FCRA rules or face liability. The scope extends far beyond traditional credit decisions, affecting nearly every major financial and employment transaction in your life.

How Violations Happen in California

Violations occur constantly in California because many businesses either don’t understand the FCRA or cut corners to save money. Common violations include pulling credit reports without your written permission, failing to notify you when a credit decision goes against you, and ignoring your dispute requests when you find errors on your report. The FTC and the Consumer Financial Protection Bureau enforce the FCRA, and statutory damages for willful or negligent violations range from $100 to $1,000 per violation according to FTC guidance.

The Real Cost of FCRA Violations

In class action lawsuits, these violations add up fast. If a company pulls credit reports from 500 people without authorization, potential damages could reach $500,000 or more. California courts have been particularly active in FCRA litigation, and judges take violations seriously. Businesses that operate without a written compliance manual face even higher liability because they cannot demonstrate reasonable procedures to prevent violations.

Building Your Case Against Violations

If you’ve been denied credit, employment, or housing and suspect an FCRA violation occurred, you should document exactly what happened-including dates, names of company representatives, and copies of any notices you received. This documentation strengthens your case significantly and provides the foundation for holding companies accountable. Understanding your specific rights under the FCRA puts you in a stronger position to recognize when a violation has taken place and what steps you can take next.

What You Can Actually Do About FCRA Violations

Your Right to Accurate Credit Information

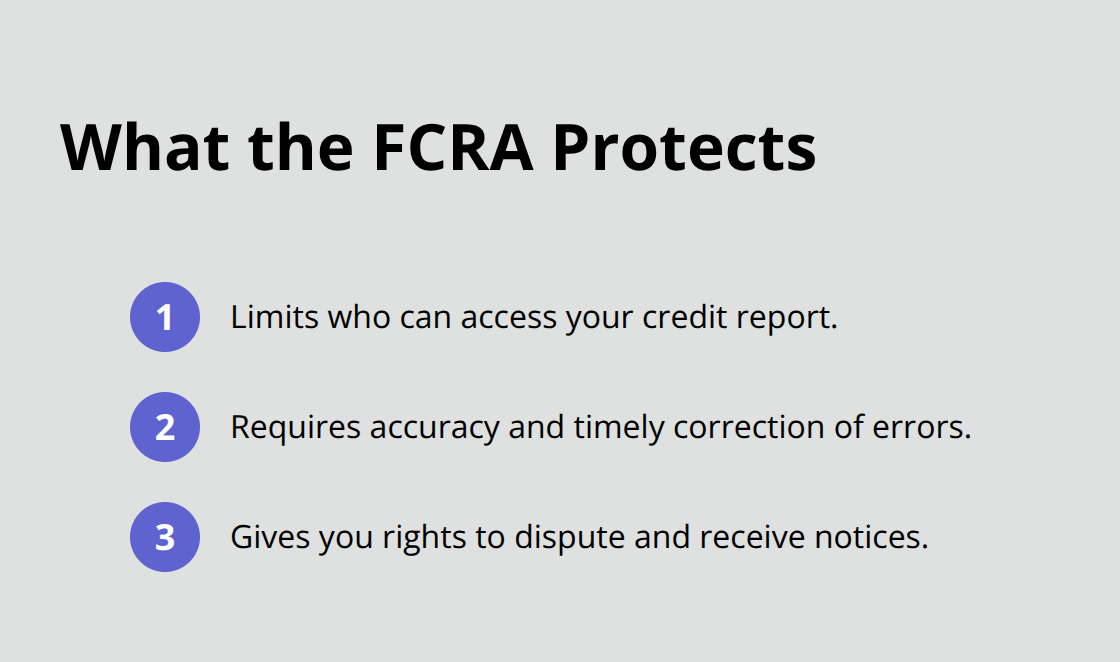

The FCRA gives you concrete rights, and understanding them means you can act fast when violations happen. California law protects your right to accurate credit information, access to your reports, and the ability to dispute errors directly with credit bureaus and the companies that reported the information. Since 2020, the three major credit reporting agencies-Equifax, Experian, and TransUnion-have offered free weekly credit reports instead of just one annual report, which means you can monitor your file constantly and catch problems immediately. Inaccurate information directly damages your credit score and costs you money in higher interest rates or rejected applications.

How to Dispute Errors on Your Report

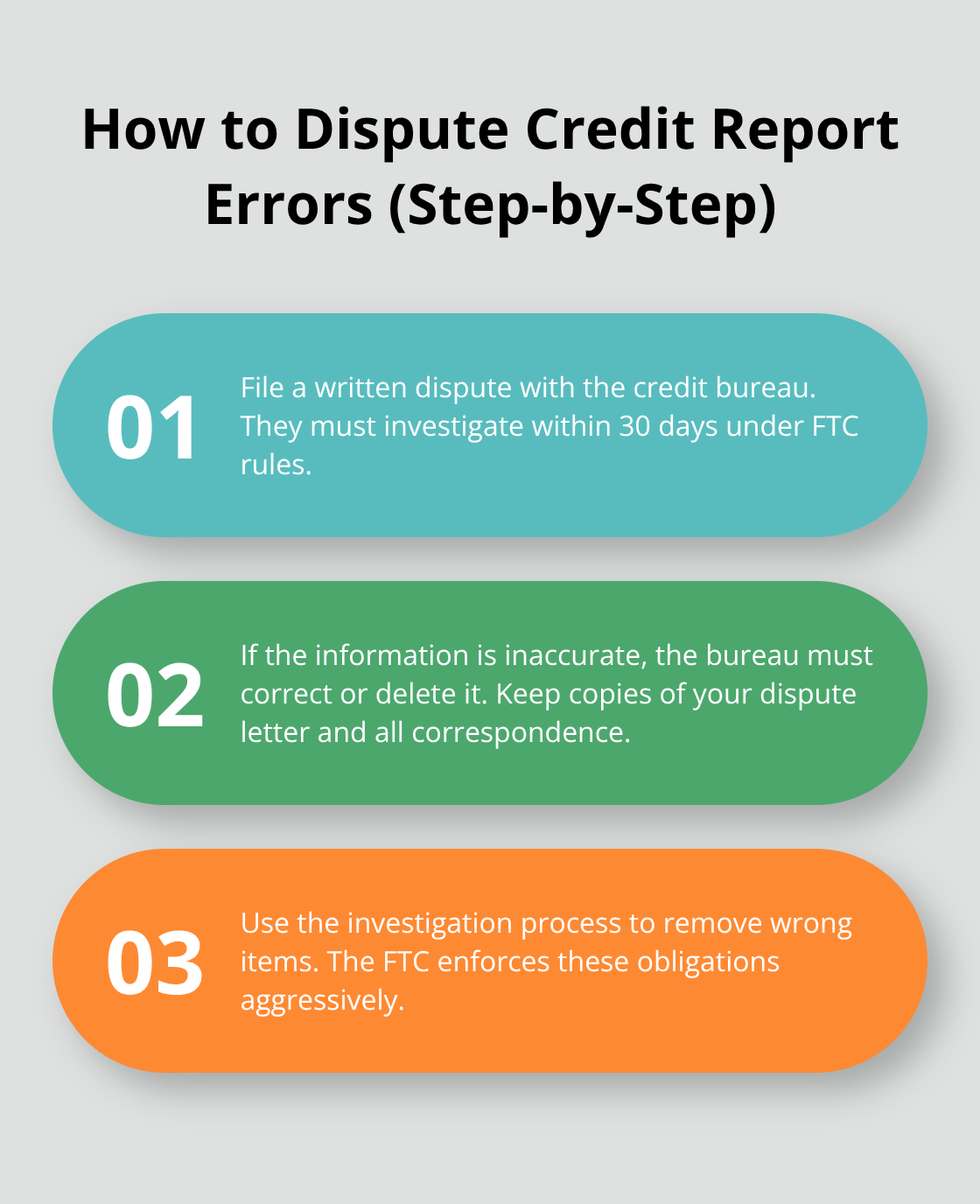

When you spot an error, you have the legal right to file a dispute with the credit bureau, and they must investigate within 30 days according to FTC rules. If the information is inaccurate, they must correct or delete it. Contact the credit bureau in writing and keep copies of your dispute letter. The investigation process is your strongest tool for getting inaccurate information removed, and the FTC enforces this process aggressively.

Document everything-keep copies of applications, denial letters, emails, and records of any conversations with company representatives.

Unauthorized Credit Pulls and Your Legal Remedies

Creditors and employers who pull your report without written authorization commit a violation, and you can sue them for statutory damages of $100 to $1,000 per violation under the FCRA. Class action lawsuits against major employers and lenders have produced settlements worth millions because violations pile up across hundreds or thousands of people. Willful violations (intentional disregard of the law) carry higher damages than negligent ones, and companies without a written compliance manual face stronger liability because they cannot prove reasonable procedures to prevent violations.

The Adverse Action Notice Requirement

When a company denies you credit, housing, or employment based partly on your credit report, they must send you an adverse action notice explaining the decision and your right to obtain and dispute the report. Many companies skip this step or send vague notices that don’t clearly explain your rights, which itself violates the FCRA. If you receive a denial and no adverse action notice follows, that’s evidence of a violation. This failure to notify you represents a separate violation that strengthens your potential claim.

Taking Action Against Violations

If you find errors on your report or suspect unauthorized access, the documentation you gather becomes critical evidence. Willful violations carry higher damages than negligent ones, and companies without a written compliance manual face stronger liability. If you believe an FCRA violation has affected your credit, employment, or housing application, aggressive legal help from a California consumer protection firm can evaluate your claim through a free case review and determine whether you have grounds for legal action.

How Businesses Must Comply with the FCRA

Authorization Requirements That Protect Your Rights

Businesses that pull credit reports face strict legal requirements, and most fail to follow them properly. The FCRA requires written authorization before accessing anyone’s credit file, yet many employers, landlords, and creditors skip this step or use vague language that doesn’t meet legal standards. California courts have ruled on what counts as clear authorization-the disclosure must be standalone, readily noticeable, and explicitly state who will obtain the report and what types of reports may be used. In the Keefer v. Ryder Integrated Logistics case from Northern California, the court found that listing specific report types like education, credit history, and character helps applicants understand the scope of what will be reported. Branding elements and navigation buttons don’t automatically violate the standalone requirement if the core information remains clear and conspicuous.

If you’re a business, your authorization form must be a separate document that clearly identifies who you are, what reports you’ll pull, and why. Vague language like “third-party or consumer reporting agency” without clarity about identity creates liability. Courts have rejected technical challenges to disclosure wording when the essential standards are met, but that doesn’t mean cutting corners is safe-it means prioritization of readability and noticeability over overly strict formatting.

The Furnisher’s Duty to Investigate Disputes

When consumers dispute information on their reports, businesses that furnished the data must investigate within 30 days according to FTC rules, and this is where many companies fail catastrophically. The furnisher-the creditor, employer, or collection agency that reported the information-has a legal duty to investigate disputes, correct verified inaccurate information, and report corrections back to credit bureaus. Companies without a written compliance manual face higher liability because they cannot demonstrate reasonable procedures to prevent violations.

Statutory damages for willful violations range from $100 to $1,000 per violation according to FTC guidance, and negligent violations can still reach $100 per violation. If a company ignores your dispute or fails to investigate properly, that’s a separate violation that compounds damages in class actions.

Automation Cannot Replace Human Review

The increasing reliance on chatbots and automation in dispute handling creates additional risk-automation cannot replace human review for complex disputes, and companies that rely solely on automated responses face allegations of inadequate investigation. Businesses must maintain formal dispute procedures, train employees on FCRA rules, conduct regular audits, and document their processes. Without these safeguards, liability accumulates quickly, particularly when violations affect hundreds of people across the same compliance failure.

Human customer service representatives must remain accessible for disputes that require judgment calls or clarification. A company that routes all disputes through a chatbot without human escalation violates the spirit of the FCRA’s reinvestigation requirement and exposes itself to significant liability.

Building a Compliance Program That Works

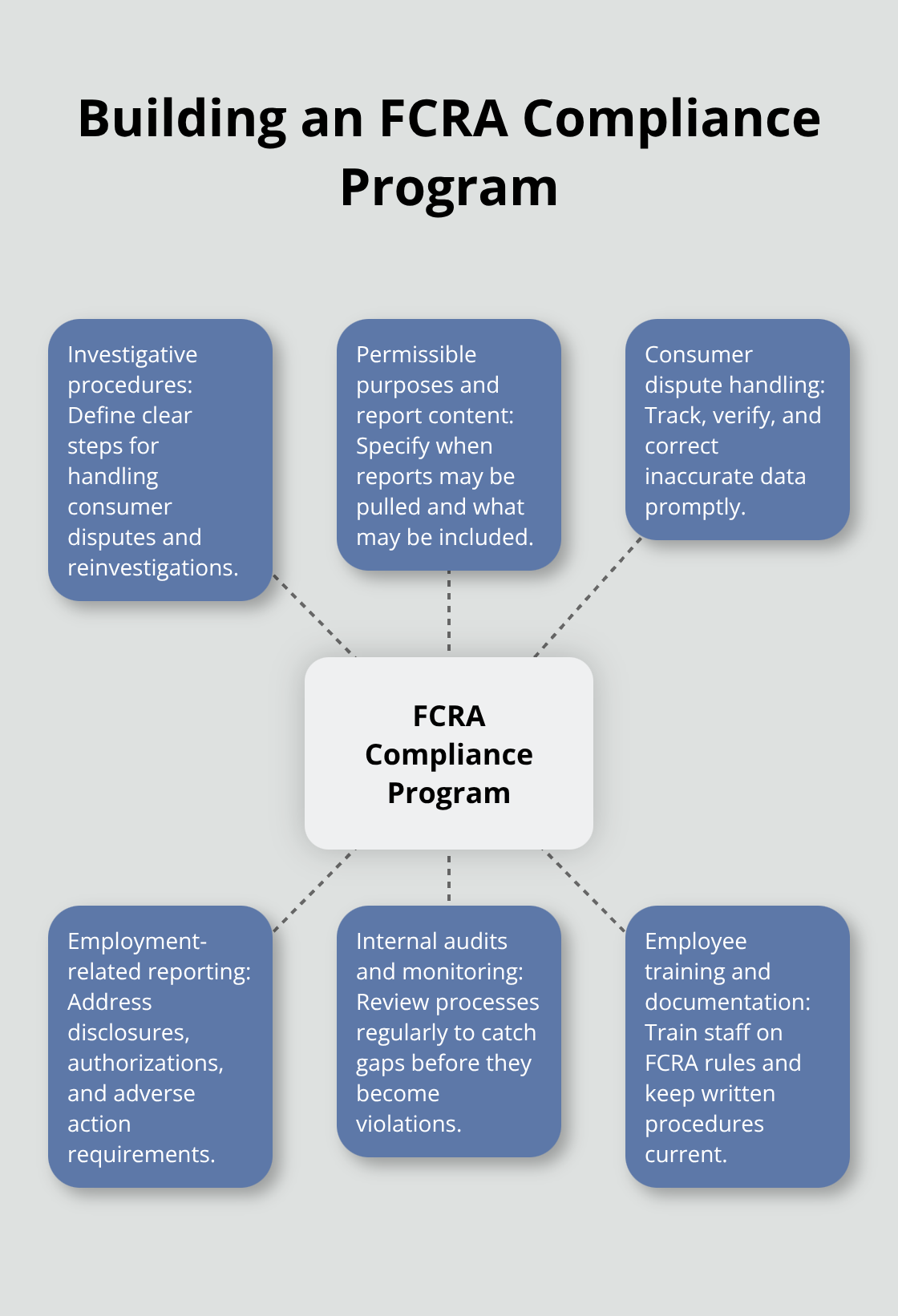

Companies that operate without written compliance procedures face substantially higher liability exposure. A formal compliance manual should cover investigative procedures, permissible purposes and report content, consumer disputes and reinvestigations, and employment-related reporting requirements. Regular internal audits and process monitoring help maintain ongoing FCRA compliance and reveal gaps before they become violations.

Businesses that take compliance seriously implement regular employee training on FCRA rules and maintain documented procedures for every stage of the credit-reporting process. This documentation becomes critical evidence if a violation claim arises, as it demonstrates the company attempted to follow the law through reasonable procedures.

Final Thoughts

The FCRA obligations in California are clear, but enforcement falls on you to recognize violations and take action. Your right to accurate credit information, access to your reports, and the ability to dispute errors represents real legal protection that companies must respect. When businesses pull your credit without authorization, ignore your disputes, or fail to send adverse action notices, they violate federal law and expose themselves to significant liability.

If you suspect an FCRA violation has affected your credit, employment, or housing application, document everything immediately-gather copies of denial letters, authorization forms you signed, dispute correspondence, and any adverse action notices you received. This documentation forms the foundation of a strong claim and helps establish whether a company acted negligently or willfully. Willful violations carry higher damages, and companies without written compliance procedures face substantially greater liability exposure.

We at Bontrager Law represent California residents in FCRA disputes, credit reporting errors, identity theft, and related claims against banks, collectors, landlords, and large corporations. If you believe your rights have been violated, contact us for a free case review to evaluate your claim and determine what legal options are available to hold companies accountable.