Identity theft can turn your financial life upside down in minutes. Unauthorized accounts, fraudulent charges, and debt collection calls create stress that most people aren’t prepared to handle alone.

At Bontrager Law, we help California residents get identity theft attorney help when they need it most. The right legal advocate can recover your funds, fix your credit report, and hold the responsible parties accountable.

When to Hire an Identity Theft Attorney

California recorded 135,575 identity theft reports in 2025 year-to-date, with the Los Angeles-Long Beach-Anaheim area accounting for 71,624 of those cases. Most victims don’t realize they need legal help until the damage spreads across multiple accounts and creditors. Identity theft creates a cascade of problems that go beyond what credit monitoring or a fraud alert can fix. When unauthorized accounts appear in your name, creditors treat you as the responsible party. Debt collectors call your phone. Credit bureaus report false information on your file. You can place fraud alerts and freeze your credit, but if accounts are already open and charges are mounting, those steps alone won’t recover your money or stop collectors from pursuing you.

Accounts Opened Without Your Permission

Thieves open new credit cards, apply for auto loans, or establish utility accounts using your Social Security number and personal information. You may not discover these accounts for weeks or months, especially if the fraudster changes the mailing address. The damage compounds quickly-late payments appear on your credit report, collection agencies contact you, and your credit score drops significantly. Disputing these accounts yourself requires sending letters to creditors, credit bureaus, and sometimes debt collectors. Many creditors ignore disputes or respond slowly. An identity theft attorney handles these disputes directly, forcing creditors and credit bureaus to verify the fraudulent accounts and remove them from your file. The California Attorney General’s office recommends acting within the first 48 hours if you suspect identity theft, but even quick action doesn’t guarantee creditors will cooperate. When they don’t, an attorney applies pressure through legal channels that individual victims typically lack.

Fraudulent Charges and Debt Collector Harassment

Charges appearing on your existing accounts require immediate action, but the process involves more than calling your bank. You must file a dispute with the card issuer, report the fraud through IdentityTheft.gov, file a police report, and then follow up repeatedly as the investigation drags on. Meanwhile, if the fraud goes undetected, creditors report the unpaid charges to collection agencies. Once a debt collector contacts you, federal law limits what they can do, but many violate those rules anyway-calling repeatedly, threatening wage garnishment, or ignoring cease-and-desist letters. An attorney acts as a buffer between you and collectors, stopping the harassment immediately and forcing them to prove you owe the debt. If a collector violates the Fair Debt Collection Practices Act, you may have a claim for damages. Collectors rarely back down without legal pressure, which is why representation becomes necessary when harassment escalates.

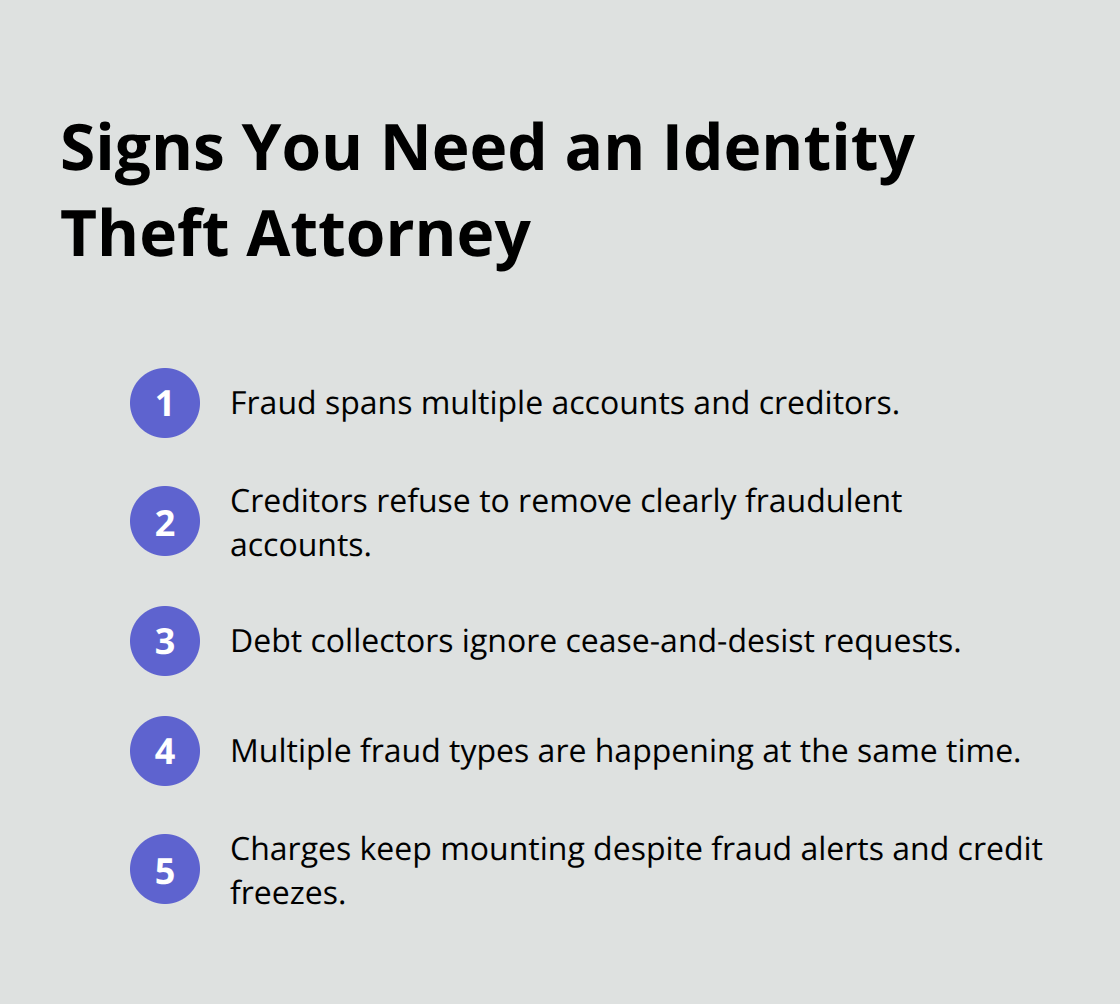

When Legal Help Becomes Essential

The right time to hire an attorney is when creditors refuse to remove fraudulent accounts, debt collectors ignore your requests to stop contacting you, or multiple fraud types occur simultaneously. These situations signal that self-help remedies have failed and that professional intervention can protect your rights and finances moving forward.

Choosing an Attorney Who Delivers Results

Track Record and Case Experience

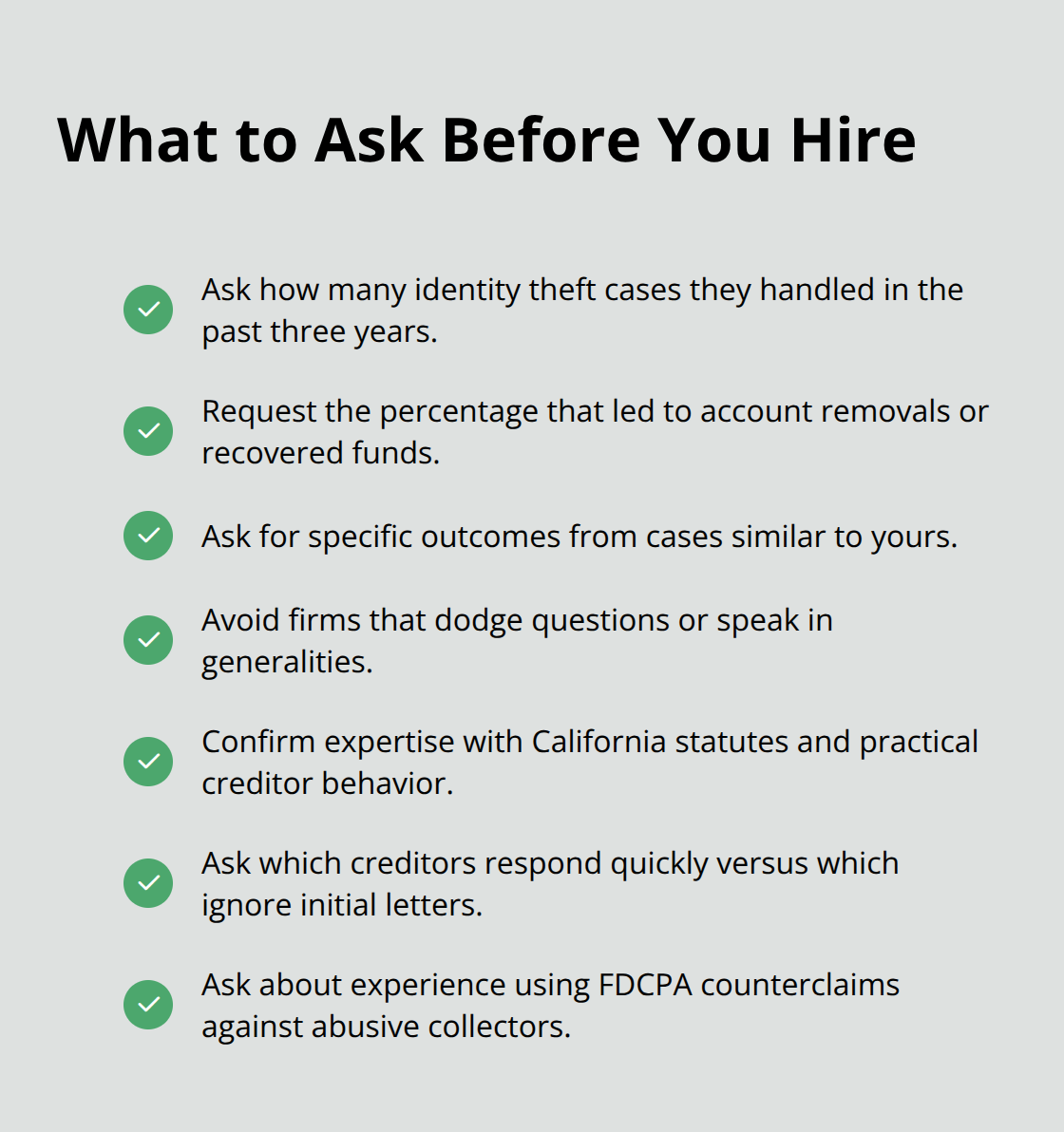

Finding the right identity theft attorney means looking beyond credentials and focusing on what matters most: whether they can actually recover your money and fix your credit. California identity theft cases require someone who understands both the state’s identity theft statutes and how creditors, debt collectors, and credit bureaus operate in practice. When you call a firm, ask directly how many identity theft cases they’ve handled in the past three years and what percentage of those cases resulted in account removal or fund recovery. A firm worth hiring will have specific numbers ready. They should also tell you about cases similar to yours and what happened-not hypothetical scenarios, but actual outcomes. If they dodge the question or speak in generalities, move on.

The best attorneys in California have handled hundreds of cases and know exactly how long disputes take, which creditors respond quickly versus which ones ignore initial letters, and when to escalate to litigation. They’ve also learned which debt collectors violate the Fair Debt Collection Practices Act repeatedly, making them targets for counterclaims that can shift the entire case in your favor.

Litigation Capability and Creditor Pressure

Ask whether the firm has successfully sued creditors or credit bureaus under California’s identity theft laws or federal statutes like the Fair Credit Reporting Act. Cases that go to litigation demonstrate the attorney’s willingness to fight when creditors refuse to settle, which increases leverage in negotiations. An attorney who takes cases to court signals to creditors that you’re serious about recovery, not just sending dispute letters that get ignored.

Understanding Fee Structures

Fee structure determines whether legal help is actually affordable when you’re already dealing with financial damage. Some attorneys charge hourly rates ranging from $150 to $400 per hour, which adds up fast when disputes stretch across multiple accounts and creditors. Others work on contingency, meaning they take a percentage of recovered funds only if they win. Contingency arrangements align the attorney’s incentive with yours-they profit when you recover money.

Always clarify what the fee covers: Do they handle paperwork, creditor negotiations, and credit bureau disputes? Will they represent you if litigation becomes necessary, or do they refer you elsewhere? Some firms charge a flat fee for specific services like filing a police report or disputing accounts, while others include everything under one agreement.

Red Flags in Fee Agreements

Before signing anything, request a written fee agreement that spells out exactly what you’re paying for and what happens if the case takes longer than expected. If an attorney demands a large upfront retainer without explaining what work justifies that cost, that’s a red flag. Legitimate firms explain their fees clearly because they know victims are already stressed about money.

The firm you choose should offer a free initial consultation so you understand your options before committing to representation. This conversation reveals whether the attorney listens to your situation, asks relevant questions about your accounts and creditors, and explains a realistic path forward. Once you’ve narrowed your options based on experience and fees, the next step involves understanding exactly how an attorney protects your rights against creditors and credit bureaus.

How an Attorney Recovers Your Money and Fixes Your Credit

Forcing Credit Bureaus to Verify Fraudulent Accounts

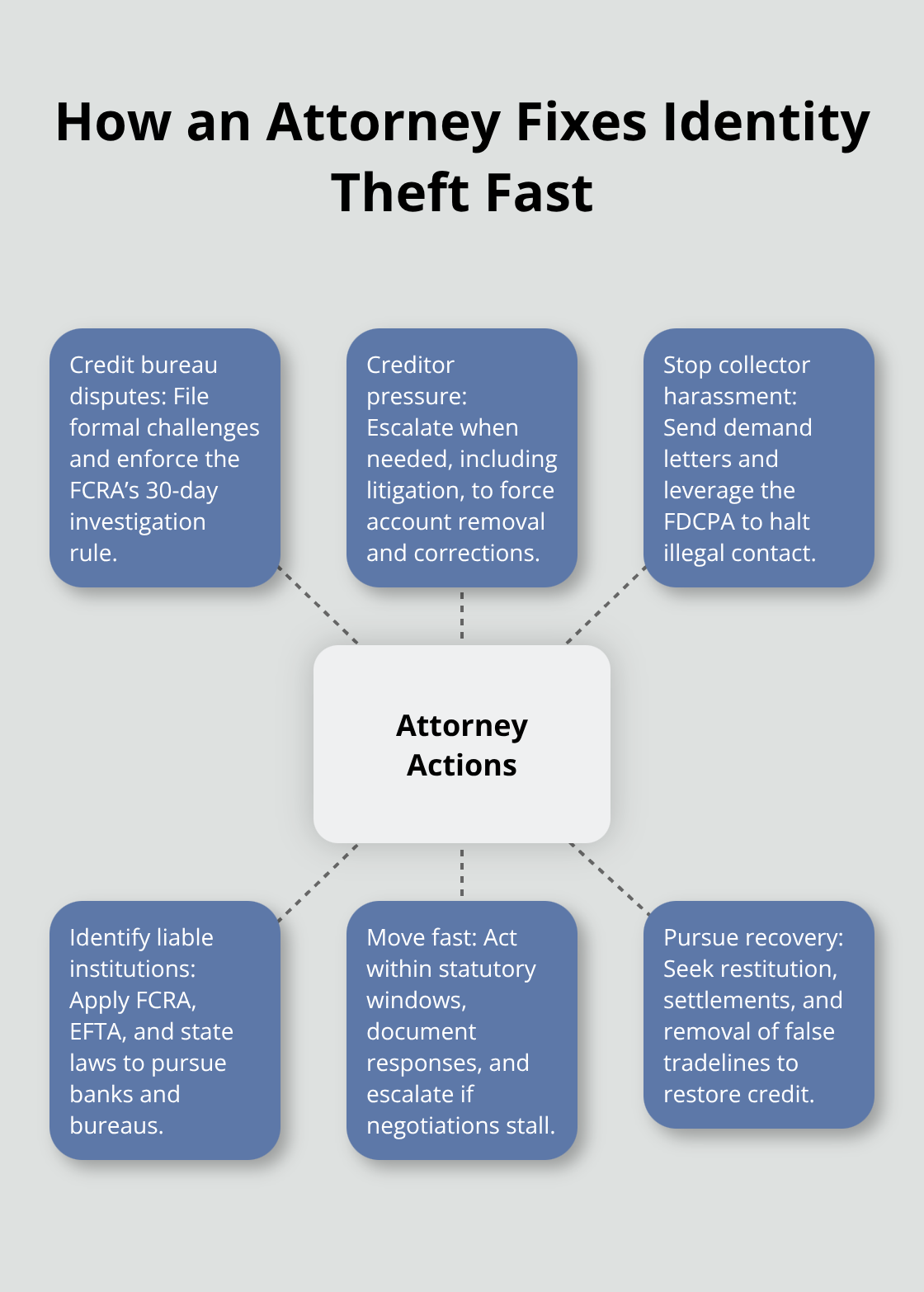

An identity theft attorney does not simply send dispute letters and hope creditors respond. They file formal challenges directly with credit bureaus and demand proof that fraudulent accounts are legitimate. The Fair Credit Reporting Act requires credit bureaus to investigate disputes within 30 days and remove accounts that cannot be verified. Most bureaus comply with this timeline only when an attorney files the dispute, because they understand non-compliance creates legal liability. When a creditor cannot prove you authorized an account, the bureau must delete it from your report. An attorney forces this verification process to happen quickly instead of waiting months while your credit score suffers.

Stopping Debt Collector Harassment

Debt collectors respond differently to attorney representation than they do to individual victims. Under the Fair Debt Collection Practices Act, collectors cannot contact you repeatedly, threaten wage garnishment without legal authority, or ignore cease-and-desist letters. Many collectors violate these rules routinely because individual victims rarely pursue legal claims. Once an attorney sends a demand letter, collectors stop calling immediately because they understand the risk of counterclaims for damages. An attorney who has sued debt collectors before knows which firms violate the law repeatedly and can leverage that history during negotiations. If a collector has ignored cease-and-desist letters or called your workplace despite being told not to, an attorney can file a counterclaim that shifts leverage entirely. Suddenly the collector faces potential damages of $100 to $1,000 per violation, making settlement far more attractive than continued harassment.

Identifying Liable Financial Institutions

Filing claims against financial institutions and credit bureaus requires understanding which laws apply to your situation. If a bank failed to detect fraudulent transfers or ignored your fraud report within required timeframes, you may have claims under the Electronic Funds Transfer Act or state consumer protection statutes. Credit bureaus face liability under the Fair Credit Reporting Act if they furnish inaccurate information after notice or fail to investigate disputes properly. An attorney identifies which institutions bear responsibility for your losses and structures claims accordingly. California’s identity theft statute also allows victims to sue perpetrators for restitution, and in some cases, to pursue civil claims against third parties who facilitated the fraud.

Acting Quickly to Maximize Recovery

The key to successful recovery is acting quickly-California law requires creditors to remove fraudulent accounts within specific timeframes, and delays weaken your position. An attorney files disputes immediately, documents every creditor response, and escalates to litigation if settlement negotiations stall. This aggressive approach prevents fraudulent accounts from aging on your credit report, which would require additional dispute rounds and further damage to your score. The longer fraudulent accounts remain on your file, the harder they become to remove and the more they harm your creditworthiness.

Final Thoughts

An effective identity theft attorney combines deep knowledge of California’s identity theft laws, a proven track record of recovering funds and removing fraudulent accounts, and the willingness to litigate when creditors refuse to settle. The attorney you hire should ask specific questions about your accounts, explain realistic timelines, and provide a clear fee structure upfront. They should also demonstrate that they’ve handled cases similar to yours and achieved measurable results.

Recovery from identity theft happens fastest when you act immediately. The first 48 hours matter most-contact your banks, place fraud alerts, and file a police report. Within the first week, dispute fraudulent charges in writing and review all three credit reports for unauthorized accounts. If creditors ignore your disputes or debt collectors continue harassing you after you’ve sent cease-and-desist letters, self-help remedies have reached their limit, and identity theft attorney help becomes necessary.

At Bontrager Law, we represent California residents across the state in identity theft disputes, credit reporting errors, and unlawful debt collection. We know exactly how to pressure creditors into removing fraudulent accounts and how to stop debt collectors from violating your rights. Contact us for a free case review to discuss your situation and learn what recovery looks like for your specific circumstances. Visit njb.legal to get started.