Identity theft happens fast, and the financial damage can last years. California law gives you specific rights to fight back and recover losses, but you need to act quickly and know what steps to take.

At Bontrager Law, we help victims of identity theft claims in California navigate the recovery process and hold responsible parties accountable. This guide walks you through your legal protections and the concrete actions that work.

What Constitutes Identity Theft in California

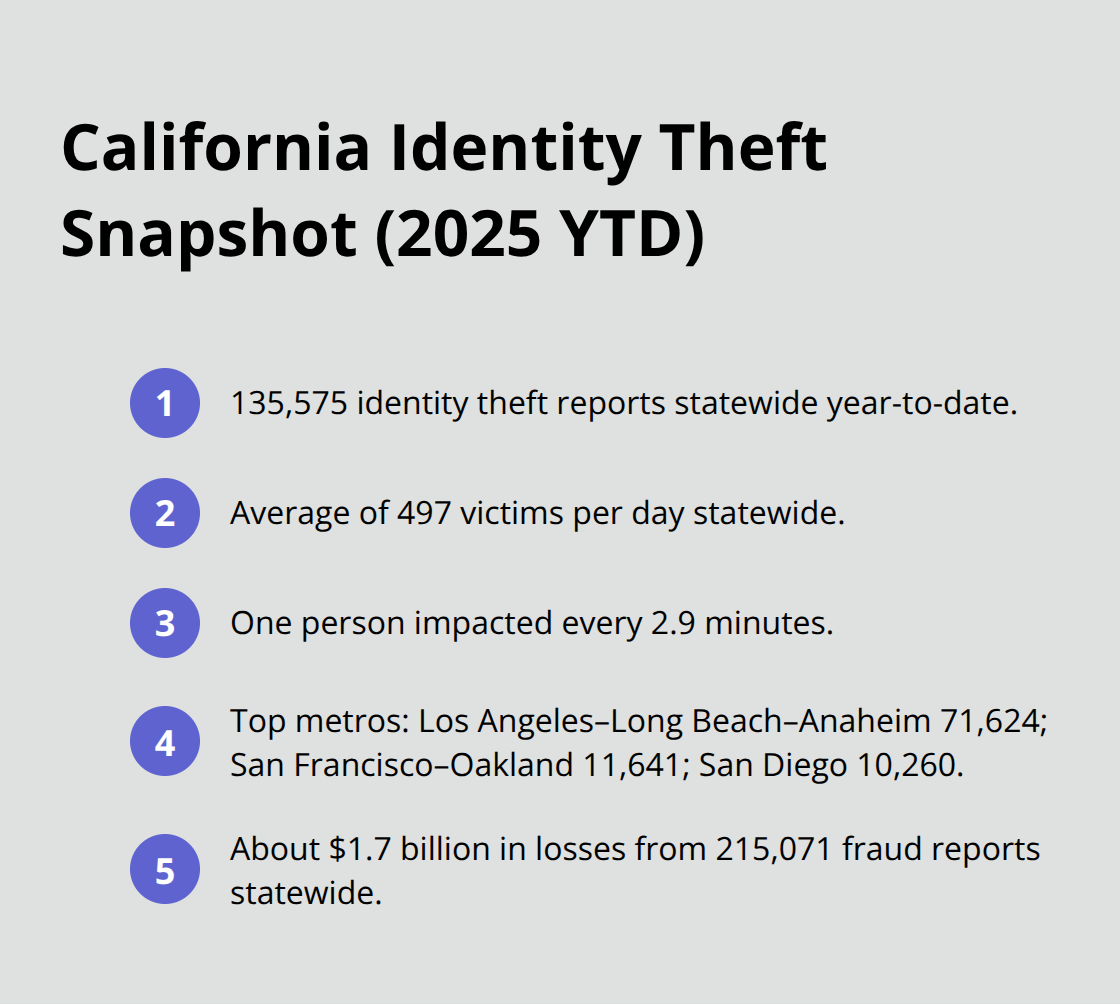

California Penal Code 530.5 defines identity theft as the willful obtaining and use of someone’s personal identifying information to commit fraud or other unlawful purposes. This covers far more than credit fraud. A thief can use your name, Social Security number, date of birth, bank account details, driver’s license number, or email address to open credit accounts, take out loans, file tax returns, claim unemployment benefits, or commit crimes in your name. The state treats this seriously-convictions carry jail time and fines, but that’s cold comfort when your credit is destroyed and you’re fighting fraudulent debt. According to the FTC Consumer Sentinel Network, California recorded 135,575 identity theft reports in 2025 year-to-date, averaging 497 victims per day. That’s one person every 2.9 minutes. Los Angeles-Long Beach-Anaheim led the state with 71,624 reports, followed by San Francisco-Oakland with 11,641 and San Diego with 10,260.

The financial toll is staggering-215,071 fraud reports statewide generated approximately 1.7 billion dollars in losses during the same period.

How Thieves Get Your Information

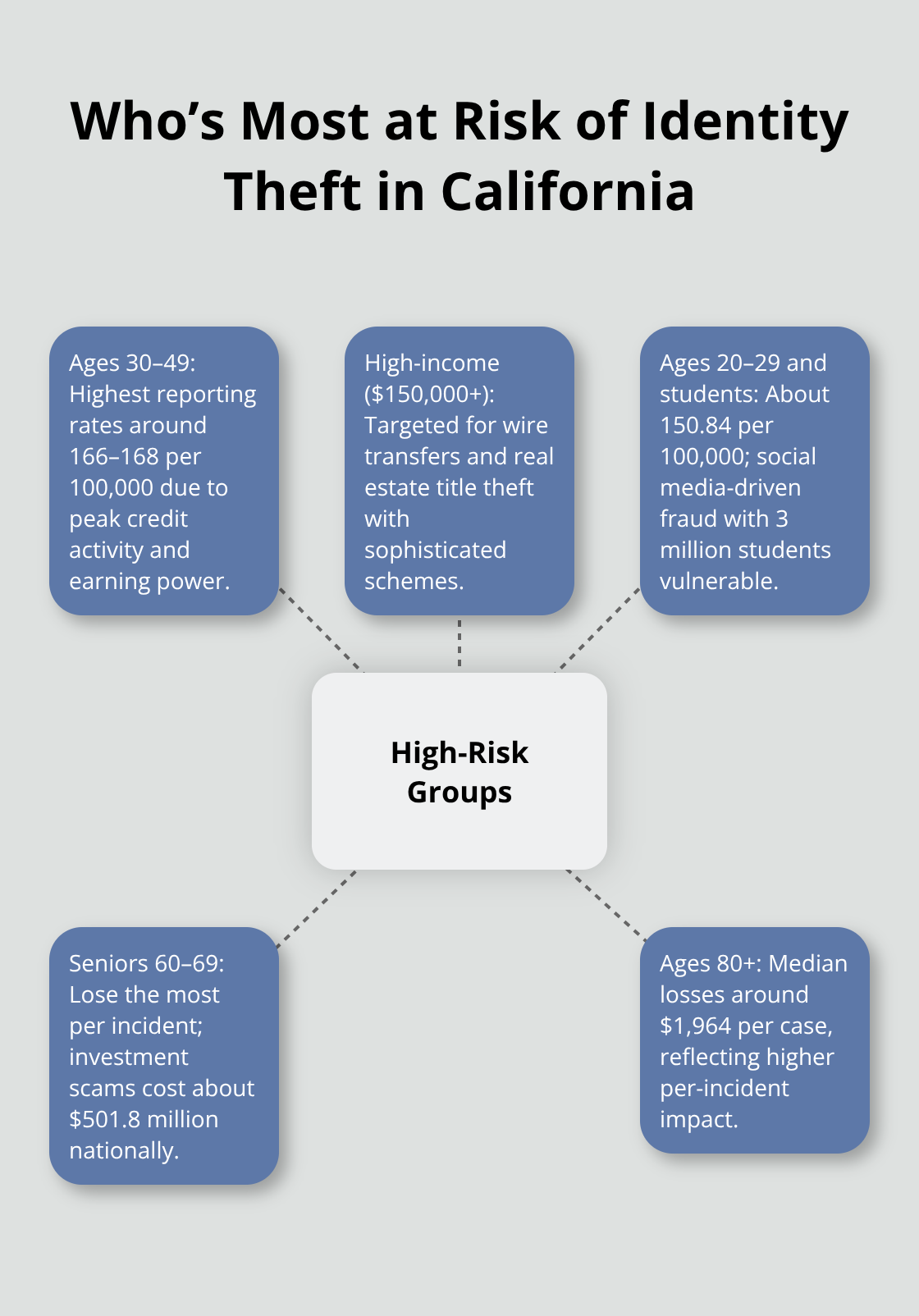

Criminals acquire personal data through data breaches, phishing emails that trick you into revealing passwords, mail theft from your mailbox, lost wallets, dumpster diving for discarded documents, employee misconduct at companies you trust, ATM or point-of-sale skimmers that capture card details, and the dark web where stolen data sells for pennies. You don’t need to be careless to become a victim-major retailers and financial institutions suffer breaches regularly. The 30-to-49 age group experiences the highest reporting rates at roughly 166 to 168 per 100,000 people, driven by peak credit activity and earning power. High-income residents earning over 150,000 dollars annually face sophisticated schemes targeting wire transfers and real estate title theft. Young adults aged 20 to 29 report at about 150.84 per 100,000, with California’s 3 million students particularly vulnerable to social media-driven fraud.

Seniors aged 60 to 69 lose the most per incident-investment scams alone cost this group about 501.8 million dollars nationally, with those 80 and older facing median losses around 1,964 dollars per case.

Spotting the Red Flags Early

Watch for bills that stop arriving on time-a thief may have changed your address with creditors. Check your credit card and bank statements weekly for unauthorized charges, not monthly. Missing statements or unexpected bills from companies you never opened accounts with signal trouble. Review your credit reports for unfamiliar accounts and hard inquiries from lenders you didn’t contact. You can obtain one free report annually from each of the three major bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com or by calling 1-877-322-8228. If you spot fraud, act immediately. The faster you report it, the faster you can limit liability and begin recovery. In California, you have the right to place a fraud alert with all three bureaus, which lasts 90 days and prevents criminals from opening new accounts using your name. You also have the right to request a credit freeze, the strongest protection available and completely free under state law. These protections form the foundation of your defense, but understanding what happens next-and how California law backs your recovery efforts-separates victims who regain control from those who remain trapped in the damage.

Your Legal Rights and Remedies Under California Law

Place a Fraud Alert and Credit Freeze Immediately

The moment you suspect fraud, you have the right to place a fraud alert with Equifax, Experian, and TransUnion simultaneously by contacting just one bureau-the alert spreads to all three within one business day. This 90-day alert prevents lenders from opening new accounts in your name without additional verification. A credit freeze provides even stronger protection by blocking creditors from accessing your credit file entirely unless you temporarily lift it. Unlike a fraud alert, a freeze costs nothing under California law and remains active until you remove it, giving you permanent protection against new account fraud.

Many victims worry that a freeze complicates their own borrowing-it does, but only when you want to apply for credit, and you control the timing by lifting the freeze for specific lenders. Request your freeze at each bureau’s website: Equifax.com, Experian.com, and TransUnion.com. Send written confirmation to each bureau and keep copies for your records.

Dispute Fraudulent Accounts and Charges in Writing

California law grants you the absolute right to dispute fraudulent accounts and charges. When you identify unauthorized transactions on credit cards or bank accounts, contact the card issuer or bank immediately and request a chargeback or reversal. Follow up in writing within 30 days of receiving your statement showing the fraud. For credit reporting errors, dispute items directly with the bureaus in writing using certified mail-include a copy of your police report and the FTC Identity Theft Affidavit, which you can obtain at IdentityTheft.gov.

The bureaus must investigate within 30 days and remove items they cannot verify. This process works because credit bureaus face substantial liability under the Fair Credit Reporting Act if they fail to investigate or maintain inaccurate information. If a debt collector contacts you about fraudulent debt, respond immediately in writing stating you are an identity theft victim and dispute the entire debt. Reference California Civil Code 1798.93 and include copies of your police report. Debt collectors who ignore this face liability under the Fair Debt Collection Practices Act and California law.

Recover Damages Against Responsible Parties

California Penal Code 1798.150 and related statutes give you the right to pursue damages against companies that fail to protect your data or mishandle your information after a breach. You can recover actual damages, statutory damages up to $100 to $750 per violation per consumer, and attorney’s fees-meaning a strong case often covers legal costs entirely. This shifts the financial burden to the responsible party rather than leaving you to absorb the loss alone.

For serious cases involving multiple fraud types, large losses, or business identity theft, the recovery process becomes complex and time-intensive. Understanding which remedies apply to your specific situation determines whether you recover partial losses or hold all responsible parties fully accountable. The next section walks you through the concrete steps that protect your credit and begin your recovery immediately.

What To Do Right Now After Identity Theft

Stop Fraud Immediately on Compromised Accounts

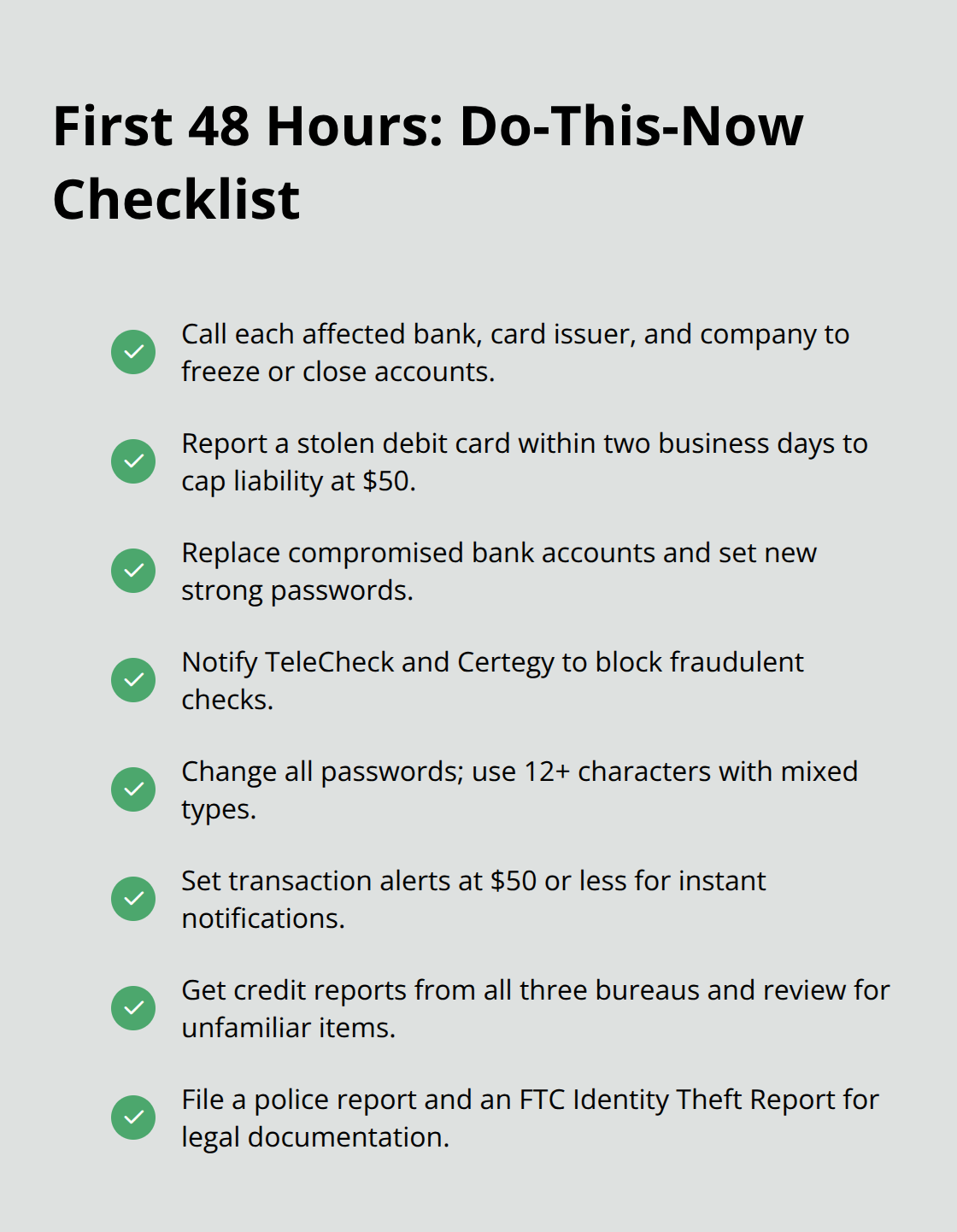

Stop the bleeding first, then investigate the damage. The 48 hours after you discover identity theft determine whether you contain the fraud or watch it spread across multiple accounts and creditors. Contact every compromised company immediately-your bank, credit card issuer, email provider, utility company, or retailer where you shopped. Tell them your account has been compromised and ask them to freeze or close it.

If your debit card was stolen, report it within two business days to limit liability to $50; delay beyond that and your liability jumps to $500 or more under federal law.

For bank accounts, close the account entirely and open a new one with a completely different password. Notify check verification services like TeleCheck and Certegy to stop fraud checks from clearing. Change every password across all accounts-use at least 12 characters mixing uppercase, lowercase, numbers, and symbols. Never reuse your mother’s maiden name or the last four digits of your Social Security number as a password component, which thieves guess within minutes.

Secure Your Mail and Tax Records

If mail was stolen or someone filed a change of address in your name, report it to the U.S. Postal Inspection Service immediately for investigation. Request an Identity Protection PIN from the IRS at IRS.gov to prevent fraudulent tax filings. Create a My Social Security account at SSA.gov to monitor for unemployment or benefits fraud. Set transaction alerts on every bank and credit card account for amounts as low as $50-most banks allow free alerts and notify you instantly of unauthorized activity.

File Reports That Establish Your Legal Standing

Obtain your credit reports from all three bureaus at AnnualCreditReport.com immediately and look for unfamiliar accounts, hard inquiries you didn’t authorize, and collection accounts you never opened. File a police report with your local law enforcement agency and obtain a copy of the report number-you will need this for every creditor, credit bureau, and debt collector you contact.

Go to IdentityTheft.gov and file a federal Identity Theft Report with the Federal Trade Commission, which generates an Identity Theft Affidavit accepted by creditors, banks, and debt collectors nationwide. Send written dispute letters to each credit bureau using certified mail with return receipt, including copies of your police report and the FTC affidavit, and demand removal of fraudulent items within 30 days.

Contact Creditors and Debt Collectors

Contact each creditor with fraudulent accounts and request information on how the account was opened using the Fraudulent Account Information Request Form from the California Department of Justice, providing your police report with each request. If a debt collector calls about fraudulent debt, send a certified letter stating you are an identity theft victim, dispute the debt entirely, and reference California Civil Code 1798.93.

Seek Professional Help for Complex Cases

For complex cases involving multiple fraud types-tax fraud, real estate title theft, unemployment benefits fraud, or business identity theft-contact a consumer protection firm. A Los Angeles-based firm with nearly 20 years of experience handling identity theft claims across California offers a free case review to assess whether you can recover damages from companies that failed to protect your data or negligently handled your information after a breach.

Final Thoughts

California law provides concrete protections for identity theft claim victims, but knowing your rights means nothing without acting on them. You have the right to place fraud alerts and credit freezes at no cost, dispute fraudulent accounts in writing, and recover damages from companies that failed to protect your data. The FTC Identity Theft Affidavit, police reports, and written disputes to credit bureaus form the foundation of recovery.

For straightforward cases involving a single fraudulent account, you may resolve the matter within weeks by following the steps outlined above. For complex identity theft claims in California involving multiple fraud types, substantial losses, or business identity theft, the recovery process demands sustained effort and legal knowledge most victims lack. We at Bontrager Law represent individuals across California in identity theft disputes against banks, credit reporting agencies, debt collectors, and corporations responsible for data breaches.

A free case review lets you understand whether your situation qualifies for damages under California law and what recovery looks like in your specific circumstances. Contact Bontrager Law today to discuss your claim and take the next step toward restoring your credit and financial security.