Subprime loans can trap you in a cycle of high interest rates and damaged credit. If you’ve taken one out, you’re not alone-millions of Californians face this challenge every year.

At Bontrager Law, we’ve helped countless borrowers recover from subprime lending and rebuild their financial foundation. This guide walks you through concrete steps to improve your credit and understand your legal rights.

Understanding Subprime Loans and Their Real Impact

What Subprime Loans Are and How They Work

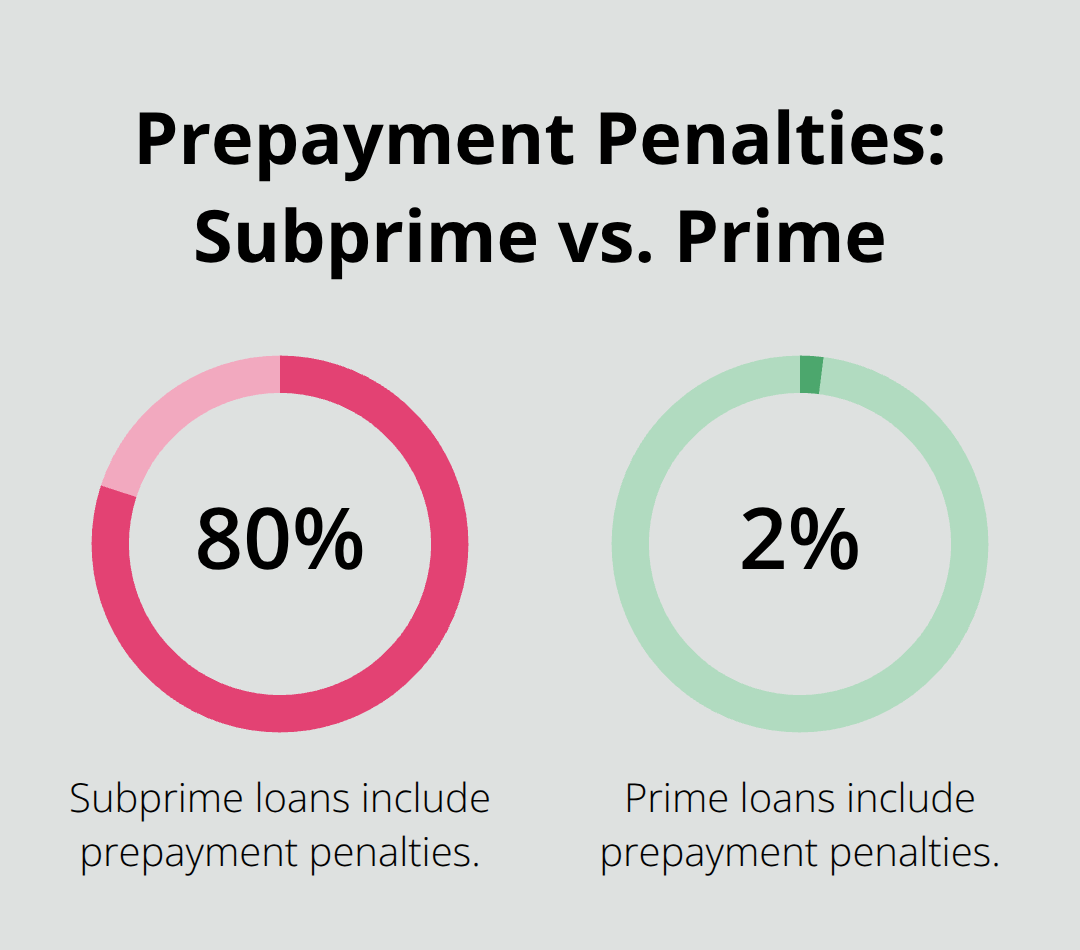

Subprime loans target borrowers with credit scores below 620, and lenders charge interest rates that run 3 to 10 percentage points higher than prime rates. These loans come with aggressive terms: prepayment penalties, inflated fees, and loan terms that stretch payments over 60 to 72 months or longer. Standard & Poor’s found that about 80% of subprime loans include prepayment penalties, compared to only 2% of prime loans. When you take on a subprime loan, you enter a financial structure designed to keep you indebted.

Auto subprime lending alone surpassed $1.1 trillion in total debt, with monthly originations around $43 billion. The average used-car loan in subprime markets now runs 65 to 69 months, meaning you pay for nearly six years. Mortgage-style subprime loans prove even worse: borrowers end up paying as much as three times the original loan amount over the life of the loan.

How Subprime Loans Damage Your Credit Score

Your credit score drops immediately when a lender pulls your report for a subprime application, and it drops again when the loan reports to the credit bureaus. The real damage comes from the loan’s structure: missed payments become nearly inevitable when monthly payments consume 15 to 20% of your gross income. One late payment can drop your score 100 points or more, and subprime loans are designed so that default becomes profitable for the lender through repossession, fees, and collections. If you pay $500 per month on a subprime auto loan for six years, that’s $36,000 in total payments-yet the vehicle depreciates to nearly worthless in half that time. Collections accounts, charge-offs, and repossessions then stay on your credit report for seven years, blocking access to housing, employment verification, and any future credit at reasonable rates. California renters with subprime loan damage face higher security deposits and rental rejections, since landlords review payment history heavily when screening tenants.

Why Californians Fall Into Subprime Lending

Most borrowers turn to subprime lenders because they have no other choice: traditional lenders reject them, and the alternative is no car, no home improvement, or no access to credit at all. Subprime lenders exploit this desperation through deceptive sales tactics like yo-yo financing, where you drive off the lot believing you own the car, only to receive a call days later that demands a larger down payment or higher interest rate-or the car faces repossession. Aggressive marketing targets low-income neighborhoods and communities of color; Black homeownership in California fell nearly 15% from its 2004 peak of 50.98%, largely due to predatory subprime lending during the Great Recession. Job loss, medical emergencies, and divorce push working Californians into subprime territory when they need credit fast. Starter-interrupt devices and GPS tracking installed in financed vehicles give lenders extraordinary control: they can remotely disable your car if you miss a payment, stranding you at work or trapping you miles from home. About 1.8 million auto repossessions occurred in 2017, many of them in subprime markets, and wage garnishment follows for those who cannot recover the deficiency after repossession. The truth is that subprime lending is predatory by design, not by accident.

Moving Forward: Understanding Your Situation

Subprime loans create immediate financial pressure and long-term credit damage that affects your ability to rent, secure employment, and access fair credit in the future. The structure of these loans-high rates, long terms, and aggressive collection tactics-means that your financial recovery requires both immediate action on your credit report and a clear understanding of your legal rights. California law provides protections that many borrowers don’t know exist, and knowing these protections is the first step toward rebuilding your financial foundation.

How to Fix Your Credit Report and Rebuild from Subprime Damage

Pull Your Credit Reports and Audit Them for Errors

Start with your credit report itself. Pull your reports from all three bureaus at AnnualCreditReport.com, which is the official free source mandated by federal law. Many borrowers skip this step and jump straight to payment plans, but that’s a mistake-your report likely contains errors that artificially tank your score. Look for accounts that don’t belong to you, duplicate entries, incorrect balances, accounts marked as delinquent when you actually paid them, and hard inquiries that shouldn’t be there.

File Disputes With Evidence and Precision

The Fair Credit Reporting Act gives you the right to dispute any inaccuracy, and the investigation window runs 30 to 45 days. Create a simple evidence packet for each dispute: write down the date you first saw the error, the exact account number, and any proof you have (payment confirmations, loan documents, anything showing the bureau got it wrong). Draft a precise dispute letter that cites the specific account and the section of the report you’re challenging. Send it via certified mail to both the credit bureau and the furnisher-that’s the lender or collector who reported the data. This dual approach matters because furnishers often update their records faster than bureaus do. Don’t expect instant results; the 30 to 45 day timeline is standard, but real changes take longer. Once you’ve filed disputes, pull a fresh report from one bureau every four months to monitor what’s changing across all three bureaus.

Automate Payments and Tackle Collections Head-On

While disputes work, attack the second problem: your payment history going forward. This is non-negotiable. Automate your minimum payments on every account so you never miss a due date-even one late payment can drop your score 100 points. Collections and charge-offs take priority: negotiate these in writing and request that the furnisher report the status as paid in full or closed once settled.

Build Positive Credit With Multiple Account Types

Add different types of accounts to your credit mix. Get a secured credit card if traditional approval is unlikely; you deposit cash as collateral, and the card reports to all three bureaus as you pay on time. Credit-builder loans work similarly-you borrow a small amount, make payments, and the lender reports each payment to the bureaus. Six to twelve consecutive on-time payments across multiple accounts signal reliability to future lenders. Keep your oldest account open even if you rarely use it; account age helps your score, and closing old accounts shortens your credit history. Try keeping credit utilization under 30 percent on any revolving credit, ideally under 10 percent.

Track Your Progress and Prepare for the Next Phase

Meaningful score movement typically appears within three to six months of consistent on-time payments, though major negatives like charge-offs or repossessions may take 12 to 24 months to fade. This isn’t fast, but it’s the only path that works. As your credit improves, you’ll gain access to better loan terms and rental opportunities-but California law also provides additional protections that can accelerate your recovery beyond what credit repair alone can achieve.

What California Law Does for Subprime Borrowers

California’s Predatory Lending Protections

California’s consumer protection statutes rank among the strongest in the nation, and they give you real leverage against predatory lenders and aggressive collectors. Division 1.6 of the California Financial Code, effective since 2002, directly prohibits lenders from financing loans without verifying your ability to repay, from burying credit insurance into your loan without explicit consent, and from using prepayment penalties as a trap. If a lender violates these rules, you can recover actual damages plus attorney’s fees, and willful violations trigger minimum damages of $15,000 or your actual losses plus fees-whichever is greater. California Business and Professions Code Section 17200 creates an additional avenue for relief against deceptive practices, meaning predatory sales tactics like yo-yo financing or misrepresented loan terms expose lenders to multiple legal theories simultaneously.

Federal and State Credit Reporting Rights

The Fair Credit Reporting Act protects you federally, giving you the right to dispute any inaccuracy within 30 to 45 days. California’s Consumer Credit Reporting Agencies Act adds state-level protections by allowing you to place free fraud alerts or credit freezes to block new accounts from opening in your name. These tools work together to stop identity theft and limit damage from reporting errors.

Debt Collection Limits That Protect You

Debt collectors in California face strict limits under the federal Fair Debt Collection Practices Act and California’s own debt collection statutes: they cannot contact you before 8 a.m. or after 9 p.m., cannot use threats or harassment, cannot contact you at work if your employer objects, and cannot collect amounts beyond what the original debt actually was. Wage garnishment occurs only through court judgment, not unilaterally, and California limits garnishment to 25 percent of disposable income or the amount above 40 times the state minimum wage-whichever is lower. Many collectors ignore these rules, which is exactly why documenting every call, letter, and threat matters: violations are actionable and can result in damages of up to $1,000 per violation plus attorney’s fees.

Free Counseling and Financial Assistance Programs

Free housing counseling through the National Mortgage Settlement Housing Counseling Program and HUD-certified counselors across California helps you understand loan options, compare products, and stabilize your situation if you face foreclosure or eviction-services that cost nothing and remain confidential. CalHFA offers down payment and closing cost assistance through its Single Family Lending programs, and the organization has launched the Building Black Wealth initiative specifically to address homeownership gaps in communities disproportionately harmed by subprime lending during the Great Recession.

When to Seek Legal Help

If you suspect a lender violated California’s predatory lending laws or if a collector is harassing you illegally, contact Bontrager Law for a free case review. The firm represents Californians in credit disputes, identity theft, unlawful debt collection, and auto repossession claims against banks, collectors, landlords, and large corporations.

Final Thoughts

Subprime loan credit help starts with action, not waiting. You now understand how subprime loans damage your credit, what errors to look for on your reports, and how to build positive payment history going forward. Meaningful score improvement takes three to six months of consistent on-time payments, while major negatives fade over 12 to 24 months.

California’s legal protections give you additional leverage that many borrowers never use. Division 1.6 of the Financial Code prohibits lenders from financing loans without verifying your ability to repay, and violations trigger minimum damages of $15,000 plus attorney’s fees. Debt collectors face strict limits on contact times, harassment, and collection amounts, and wage garnishment requires a court judgment (if a lender or collector has violated these rules, you have a legal claim worth pursuing).

If you suspect a lender violated California’s predatory lending laws, if a collector is harassing you illegally, or if your credit report contains errors tied to a subprime loan, contact Bontrager Law for a free case review. The firm represents Californians in credit disputes, identity theft, unlawful debt collection, and auto repossession claims against banks, collectors, landlords, and large corporations. Your financial recovery is possible, and you don’t have to navigate it alone.