A credit reporting error can tank your credit score and lock you out of loans, housing, and jobs. If you’re facing inaccurate information on your credit report, filing an FCRA complaint in California is your legal right.

We at Bontrager Law help people fight back against credit reporting violations every day. This guide walks you through the complaint process and what happens next.

What the Fair Credit Reporting Act Protects and Why It Matters

The FCRA’s Core Protections

The Fair Credit Reporting Act, passed in 1970, gives you the right to accurate information in your credit file. The law applies to credit bureaus, debt collectors, employers, landlords, and lenders who pull your report. Under the FCRA, these entities must follow strict rules about how they collect, use, and share your credit data. The Federal Trade Commission and the Consumer Financial Protection Bureau enforce the FCRA at the federal level, while California’s Attorney General adds state-level oversight.

What Counts as a Violation

If a credit bureau reports false information about you, fails to investigate your dispute within 30 days, or shares your report without a legitimate purpose, that’s a violation. The FCRA lets you sue for actual damages plus statutory damages ranging from $100 to $1,000 per violation if the violation was willful, according to cases like Omar Santos v. Experian Information Solutions. This means even if you can’t prove you lost money, you can still recover significant compensation.

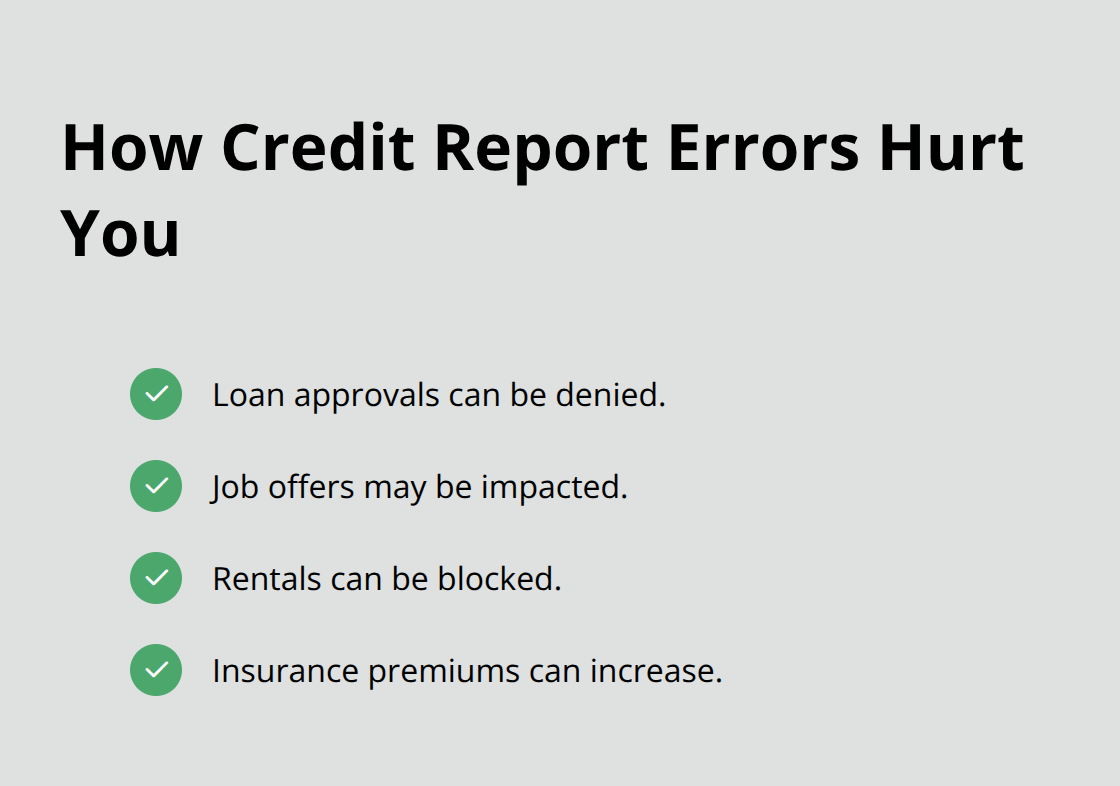

Real-World Impact of Credit Reporting Errors

Credit reporting errors hit hard in real life. An inaccurate late payment, a debt that isn’t yours, or a charge-off on your report can slash your credit score by 100 points or more, making it nearly impossible to qualify for mortgages, auto loans, or credit cards. Employers sometimes pull credit reports for hiring decisions, and inaccuracies there can cost you a job. Landlords use credit reports to screen tenants, so errors can block you from renting. Insurance companies check credit information too, potentially raising your premiums.

California’s Additional Protections

The CFPB receives thousands of credit reporting complaints annually, with inaccuracy and dispute handling topping the list. California residents have extra protections through the California Consumer Credit Reporting Agencies Act, which provides additional remedies beyond federal law. These state-level safeguards strengthen your position when you file a complaint.

Taking Action Now

If you spot an error, act fast. Pull your free annual credit reports from AnnualCreditReport.com, the official site recommended by the FTC, and review all three bureaus: Equifax, Experian, and TransUnion. Errors don’t disappear on their own, and the longer inaccurate information sits on your report, the more damage it does to your financial life. Once you’ve identified the problem, the next step is understanding exactly how to document it and file your complaint with the right agencies.

Filing Your FCRA Complaint in California

Gather and Document Your Evidence

Start by pulling your credit reports from AnnualCreditReport.com and printing them out. Highlight the errors you found, then write down the exact details: the account number, the creditor name, what’s reported versus what actually happened, and the date you first noticed the mistake. Organize your materials into a clear timeline and categories (reports, disputes, correspondence, evidence) to streamline filing and follow-up. This preparation makes your complaint stronger and gives agencies the information they need to act.

File Your Dispute with the Credit Bureau

Contact the credit bureau in writing and dispute the item. Under the FCRA, the bureau must investigate within 30 days and tell you the results. Keep copies of everything you send and every response you receive. The CFPB reports that credit reporting agencies investigate around 90 percent of disputes, but many consumers don’t follow up when corrections aren’t made. If the bureau doesn’t correct the error after your first dispute, file a second one with additional documentation like bank statements, payment histories, or correspondence proving the item is wrong.

If the debt was sold by a debt buyer or collector, demand the complete chain of assignment and the original contract to prove they own the debt. This step alone stops many violations cold because collectors can’t verify what they’re actually reporting.

Submit Your Complaint to the CFPB

File with the CFPB at consumerfinance.gov. The CFPB accepts credit report complaints and forwards them to the company within days. Your complaint typically takes less than 10 minutes to submit online. Include a clear description of what happened, the dates, the amounts, and attach your supporting documents like dispute letters and credit reports. The company has 15 days to respond and 60 days total to resolve the issue. You can check the status of your complaint online using your complaint number.

Report to California Agencies

California residents should file a complaint with the California Department of Financial Protection and Innovation at dfpi.ca.gov. The DFPI accepts complaints about credit reporting agencies and related products, offers translation services in over 240 languages, and processes online submissions in about five minutes. Mail submissions arrive within one to five days if you prefer that route. Include the same documentation you used for the CFPB complaint. If you’re dealing with a national bank, the DFPI will direct you to the Office of the Comptroller of the Currency at 1-800-613-6743. California’s Attorney General also investigates credit reporting violations through the state’s consumer protection division. File a complaint there as well.

Build Your Enforcement Trail

The more agencies you report to, the more pressure builds on the violator. These complaints inform enforcement actions and examinations, meaning your filing helps stop the same violation from happening to others. Once all three agencies have your complaint, you’ll have a documented trail showing the violation, the agency responses, and the company’s failure to correct the error-exactly what you need if litigation becomes necessary. This foundation positions you well for the next phase: understanding what happens after you file and what outcomes you can realistically expect.

What Happens After You File

The CFPB Timeline and Company Response

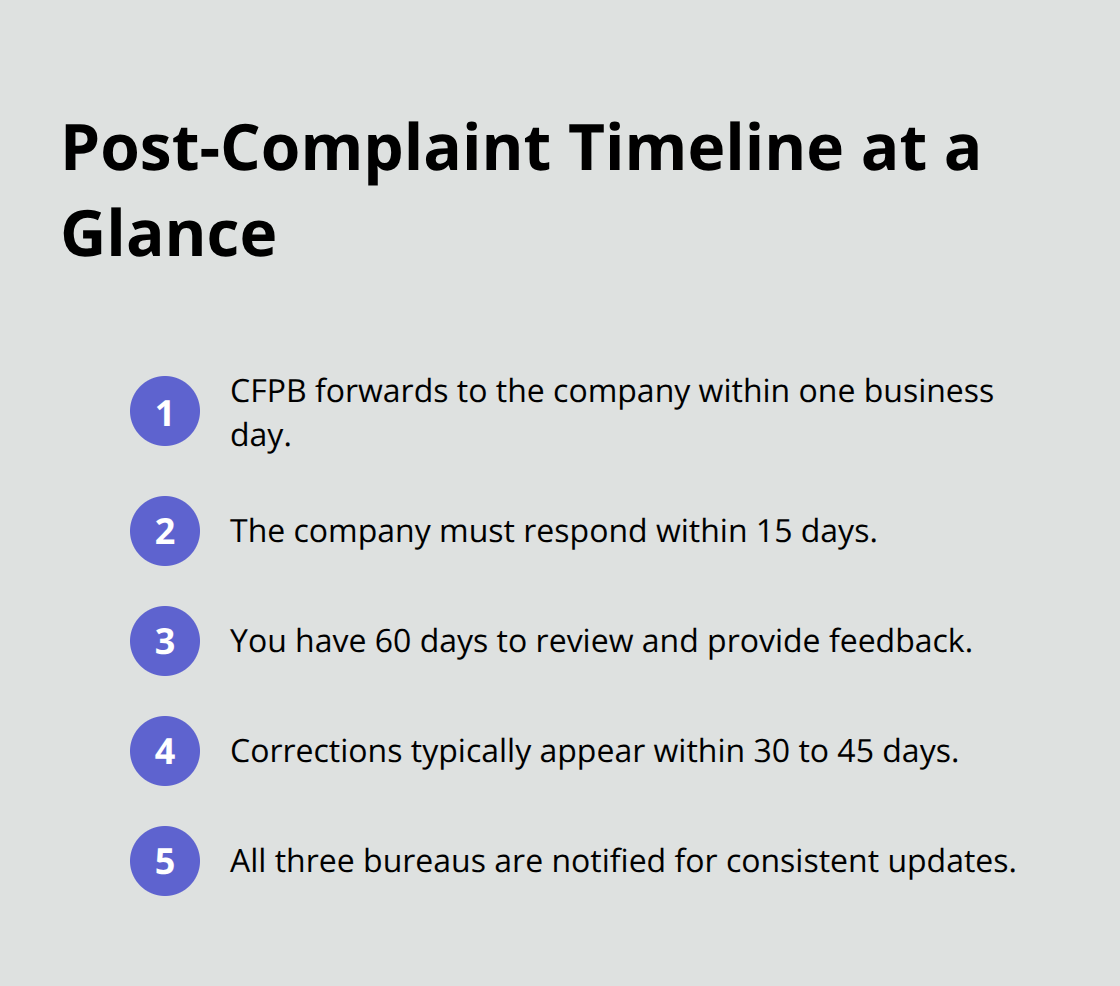

After you submit your complaint to the CFPB, the clock starts ticking on a predictable timeline that gives you concrete leverage. The CFPB forwards your complaint to the company within one business day, and the company then has 15 days to respond to you directly. In practice, many companies respond within a week because they know the CFPB is tracking their performance. The company’s response goes back to the CFPB, and you have 60 days total to review what they say and provide feedback.

How Corrections Appear Across Your Reports

During this 15 to 60 day window, the credit bureau or collector must either correct the error, remove the item from your report, or provide a written explanation of why they believe the information is accurate. If they correct the error, all three major bureaus-Equifax, Experian, and TransUnion-receive notification so the correction appears consistently across your reports. Corrections typically show up within 30 to 45 days, so check all three reports regularly after your complaint resolves. The DFPI follows a similar timeline, though their investigation can take longer if they decide to pursue enforcement action on your behalf.

Statutory Damages When Errors Persist

The outcomes available to you depend on whether the company corrects the error voluntarily or whether agencies need to force action. If the error gets corrected, you’ve won the primary battle, but you can still pursue statutory damages of $100 to $1,000 per willful violation under the FCRA, as established in Omar Santos v. Experian Information Solutions. This means you don’t need to prove you lost money to recover compensation. If the company refuses to correct a clear error or if they violated the FCRA in other ways (like sharing your report without permission or failing to investigate your dispute), you have grounds for litigation.

Building Your Case for Legal Action

The CFPB and DFPI complaints create an official record showing the violation, the company’s response, and their failure to correct the problem, which strengthens any legal claim significantly. Many companies settle disputes once they see multiple agency complaints and realize litigation costs more than paying damages. If you decide to pursue legal action, working with an attorney gives you immediate access to someone who understands exactly what California courts expect and how to value your claim. An experienced firm has handled thousands of credit reporting disputes and knows which violations carry the strongest cases. An attorney can also handle communications with the company and their lawyers, which often speeds resolution because companies take legal representation seriously. Contact a firm if the error significantly harmed your credit score, if the company refuses to correct obvious mistakes, or if you’ve already filed complaints with the CFPB and DFPI and received unsatisfactory responses.

Final Thoughts

Filing an FCRA complaint in California puts real power in your hands to correct errors and hold companies accountable. You’ve learned how to identify violations, document mistakes, and submit complaints to the CFPB and state agencies that create an official record. Companies respond within 15 days, corrections appear within 30 to 45 days, and you can pursue statutory damages of $100 to $1,000 per willful violation without proving financial loss.

The path forward depends on your situation and the company’s response to your complaint. If the credit bureau corrects the error after your complaint, monitor all three reports to confirm the fix appears everywhere. If the company refuses to correct a clear mistake or ignores your dispute, you’ve already gathered the documentation needed for legal action, and many companies settle once they see multiple agency complaints.

We at Bontrager Law represent California residents in credit reporting disputes and related claims against banks, collectors, and large corporations. Contact us if your credit reporting error significantly damaged your score, if you’ve filed complaints without results, or if you’re ready to pursue compensation for willful violations. Your credit rights matter, and you have legal remedies available.