A credit report error can tank your credit score and cost you thousands in higher interest rates. Yet most Californians don’t realize how common these mistakes are-or that they have the power to fix them.

We at Bontrager Law help people correct credit report errors every day. This guide walks you through your rights and the exact steps to dispute inaccuracies on your report.

Where Credit Report Errors Come From

Credit bureaus receive information from hundreds of thousands of data sources-banks, credit card companies, landlords, collection agencies, and courts. With that volume comes inevitable mistakes. The Consumer Financial Protection Bureau found that one in five Americans have errors on at least one of their three credit reports. Some errors are minor typos. Others are catastrophic, like accounts that don’t belong to you or payments marked as late when you paid on time.

Common Types of Errors

The most common mistakes we see fall into a few categories: accounts reported under the wrong name or Social Security number, duplicate accounts that show the same debt twice, incorrect payment history where on-time payments appear as late, wrong account balances that inflate your debt load, and closed accounts still showing as open. These aren’t rare edge cases-they happen constantly because the system relies on automated data transfers between lenders and bureaus with minimal human review. A single typo from a creditor’s computer system enters the bureau’s database and suddenly becomes part of your permanent financial record.

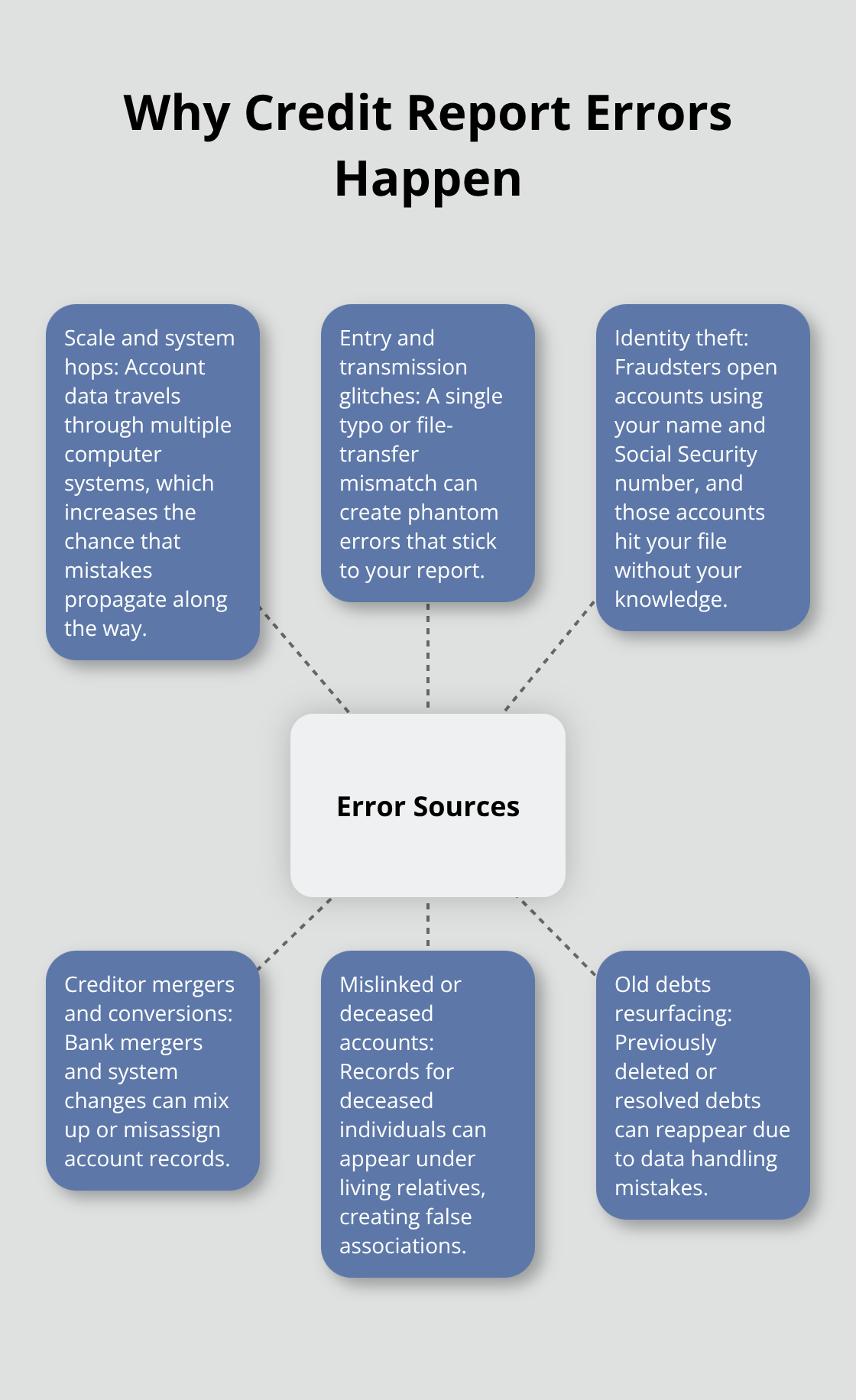

Why Errors Happen So Often

The sheer scale of credit reporting makes errors inevitable. Equifax, Experian, and TransUnion process millions of account updates daily through automated systems designed to be fast, not flawless. When a creditor updates your account information, it travels through multiple computer systems before landing on your report. A data entry error at the source, a transmission glitch, or a mismatch between your name spelling at one creditor versus another creates phantom errors.

Identity theft compounds this problem significantly. Criminals open accounts using your name and Social Security number, and those fraudulent accounts appear on your report while you remain unaware. The DFPI notes a growing risk of tech-enabled scams that specifically target personal data to create false credit entries. Even legitimate creditors make mistakes-mergers between banks cause account records to mix up, deceased individuals’ accounts sometimes appear under living relatives’ names, and old debts occasionally resurface after deletion years earlier. The bureaus aren’t required to verify information independently; they simply record what creditors report.

The Real Cost of Errors on Your Finances

A single error costs you real money. If a fraudulent account inflates your credit utilization ratio (the percentage of available credit you actually use), your score drops immediately because lenders view high utilization as risky. An incorrectly reported late payment stays on your record for seven years and signals to every lender that you’re unreliable. Clients we work with have faced mortgage denials worth hundreds of thousands of dollars because of errors on their reports, or received approval only at interest rates two to three percentage points higher than they qualified for. That difference adds up to tens of thousands in extra payments over the life of a loan.

Errors affect far more than just credit approvals. Insurance companies check credit reports and charge higher premiums to people with errors on file. Landlords deny rental applications based on inaccurate payment history. Some employers review credit reports during hiring, and errors can cost you a job opportunity. The financial damage compounds because you pay more for everything while you work to fix a problem you didn’t create.

Understanding how these errors happen is the first step toward protecting yourself. The next section shows you exactly how to obtain your credit report, identify what’s wrong, and take action to correct it.

How to Dispute Your Credit Report Errors

Getting Your Credit Report and Spotting Errors

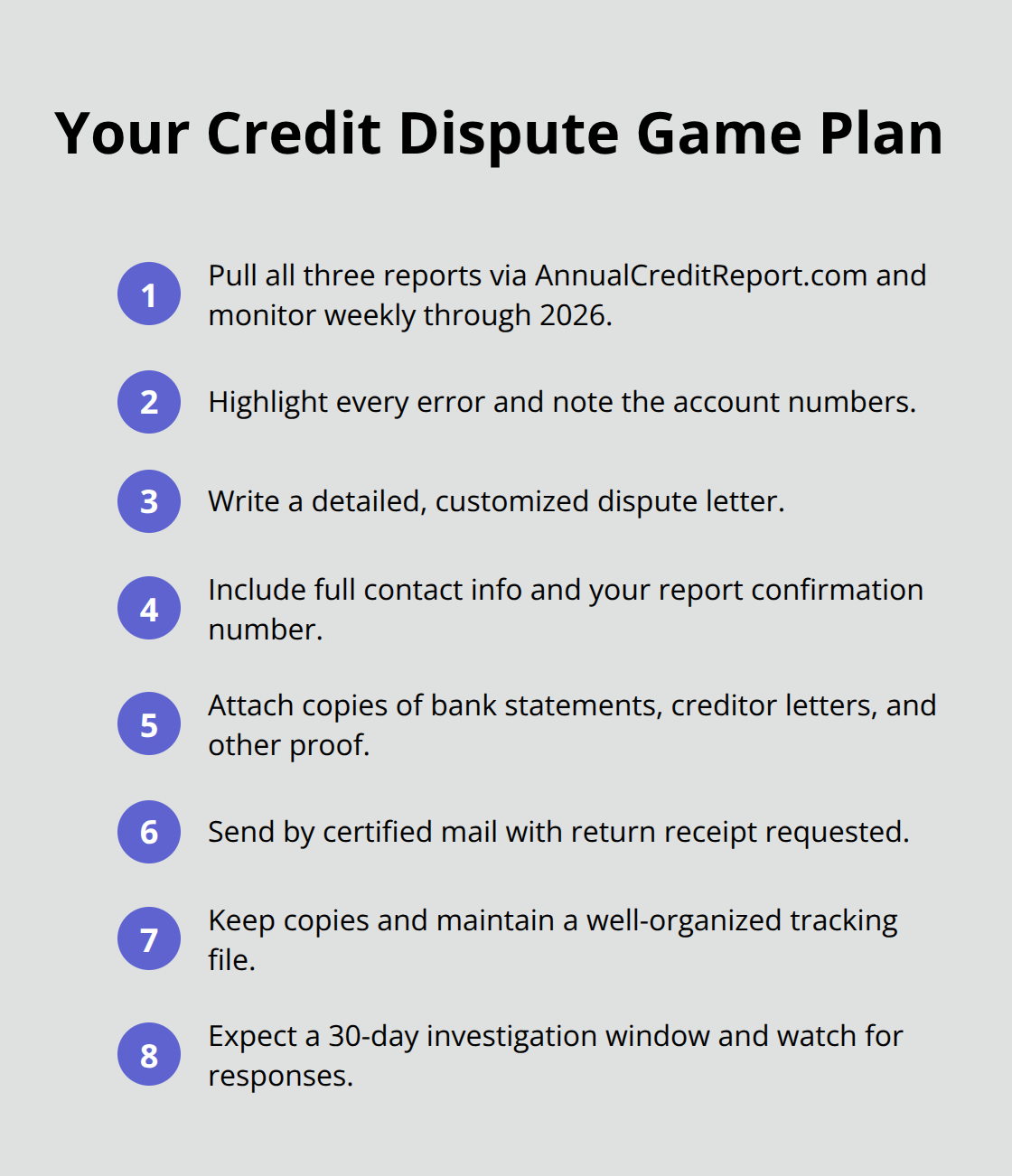

Visit AnnualCreditReport.com and request reports from all three bureaus-Equifax, Experian, and TransUnion. Through 2026, you can pull one report from each bureau every week at no cost, which means you can monitor changes as you dispute. Print or download each report and read through them carefully. Look for accounts you don’t recognize, payments marked late when you paid on time, duplicate accounts showing the same debt twice, incorrect balances, and closed accounts still listed as open. Circle or highlight every error you find. This step takes time but it’s worth it-you’re about to fix problems that cost you thousands in higher interest rates and denied credit.

Writing Your Dispute Letter

Don’t use the bureaus’ online dispute forms. They limit your explanation to a few lines and provide no space for supporting evidence. Instead, write a detailed dispute letter by hand or type it, explaining exactly what’s wrong and why.

Include your full name, address, phone number, and the confirmation number from your credit report. For each error, write the account number and a clear explanation of what’s inaccurate.

Gathering and Submitting Your Evidence

Attach copies (not originals) of documents that prove your position-bank statements showing on-time payments, creditor letters confirming account closure, or proof you never opened the account. Mail your letter and all documents by certified mail with return receipt requested to the bureau’s dispute address found on their website. Keep copies of everything you send and the certified mail receipt. The bureau must investigate within 30 days and forward your dispute to the creditor who reported the information.

What Happens During Investigation

If the creditor can’t verify the information is accurate, they must tell the bureau to fix or remove it. If the investigation finds nothing wrong, you can request a dispute statement be added to your file that explains your position-this statement appears on all future reports. Create a folder with copies of your dispute letters, all supporting documents, certified mail receipts, and responses from the bureaus. This documentation protects you if the dispute doesn’t resolve and you need to pursue further action.

Moving Forward With Your Rights

The dispute process works, but only when you follow it correctly and maintain detailed records. Understanding what the law requires from creditors and bureaus strengthens your position significantly. The next section explains your legal protections under California and federal law-rights that give you real leverage if errors persist.

What the Law Actually Requires From Credit Bureaus and Creditors

The Federal Law That Protects You

The Fair Credit Reporting Act gives you concrete legal leverage that most Californians never use. When you file a dispute, the law doesn’t ask the bureau to investigate politely-it demands action. Under federal law, the credit bureau must forward your dispute and all evidence to the creditor within five business days. That creditor then has 30 days to investigate and report back to the bureau whether the information is accurate. If the creditor cannot verify the account is yours or cannot confirm the reported information is correct, they must tell the bureau to delete or correct it. This isn’t a suggestion. It’s a requirement. The bureau must then update your report and notify you in writing of the results.

Your Right to Add a Dispute Statement

If the creditor confirms the information is accurate after investigation, you have the right to add a dispute statement to your file that explains your position. That statement must appear on every future credit report sent to lenders, landlords, or employers who request it. This creates a permanent record of your objection, which can influence how creditors view the disputed information.

California’s Additional Protections

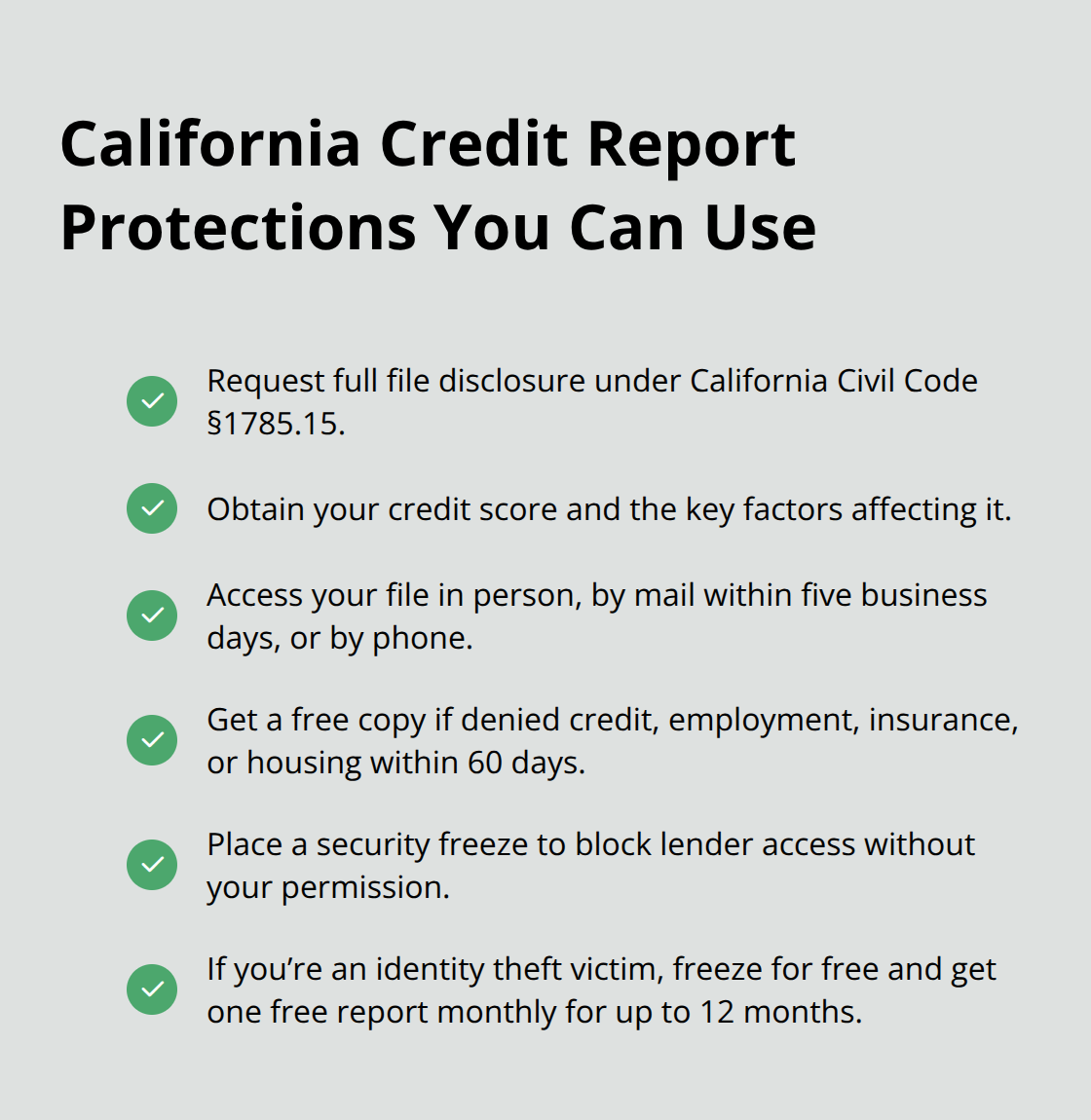

California law goes further than federal requirements. Under California Civil Code Section 1785.15, the bureaus must disclose your complete file to you, including all codes used, your credit score, and the key factors affecting it. You can access your file in person, by mail within five business days, or by phone. If you’ve been denied credit, employment, insurance, or housing within the past 60 days due to information in your report, the bureau cannot charge you the standard eight-dollar fee for a copy.

The law also gives you the right to place a security freeze on your report, which blocks lenders from accessing it without your explicit permission-a powerful tool if you suspect identity theft. Identity theft victims can place a freeze at no cost and receive one free credit report monthly for up to 12 consecutive months.

How Creditor Investigations Actually Work

The creditor’s investigation obligation is where most disputes succeed or fail. When you send detailed evidence with your dispute letter, the creditor faces a choice: investigate properly and likely find the information is wrong, or ignore your evidence and risk legal consequences. Many creditors process disputes carelessly because they assume most consumers won’t pursue further action. This is where documentation matters enormously. If you send certified mail with return receipt, keep copies of everything, and maintain a detailed file, you create an undeniable record that the creditor received your dispute and had time to investigate.

Legal Remedies When Disputes Fail

If the investigation fails to correct legitimate errors, California law and federal law both provide legal remedies. The FCRA allows you to sue a credit reporting agency for failing to investigate disputes properly or for continuing to report information they know is inaccurate. You can recover actual damages (money you lost due to the error), statutory damages up to one thousand dollars per violation, and attorney fees. This means you can pursue a lawsuit without paying out of pocket-most firms handling credit reporting cases work on contingency, collecting fees only if they win. The stronger your documentation and the clearer your evidence that the bureau failed to investigate, the stronger your case. Acting quickly matters because delays extend the harm and make it harder to prove damages later.

Final Thoughts

Correcting credit report errors takes time and persistence, but the payoff justifies the effort. You now understand how errors happen, the exact steps to dispute them, and the legal protections California and federal law provide. The difference between ignoring an error and fixing it amounts to tens of thousands of dollars over your lifetime in interest rates alone, plus better access to housing, employment, and insurance.

Many Californians successfully correct credit report errors on their own by following this process carefully. But some disputes hit roadblocks when creditors ignore evidence or bureaus fail to investigate properly. When errors persist despite your best efforts, you don’t have to accept it. The law gives you the right to pursue compensation, and you shouldn’t have to pay attorney fees out of pocket to enforce your rights.

We at Bontrager Law have spent nearly 20 years helping Californians fight credit reporting errors and identity theft. If your dispute stalls or the error continues damaging your finances, contact us for a free case review to learn whether legal action makes sense. We work on contingency, meaning you pay nothing unless we win.