A mistake on your credit report can cost you thousands of dollars in higher interest rates or denied loans. Credit report errors in California are more common than you’d think, and they often go unnoticed until they damage your financial standing.

At Bontrager Law, we’ve helped countless California residents identify and fix inaccuracies that were holding them back. The good news is that you have legal rights to challenge these errors and get them corrected.

How Credit Report Errors Actually Happen

Where Errors Come From

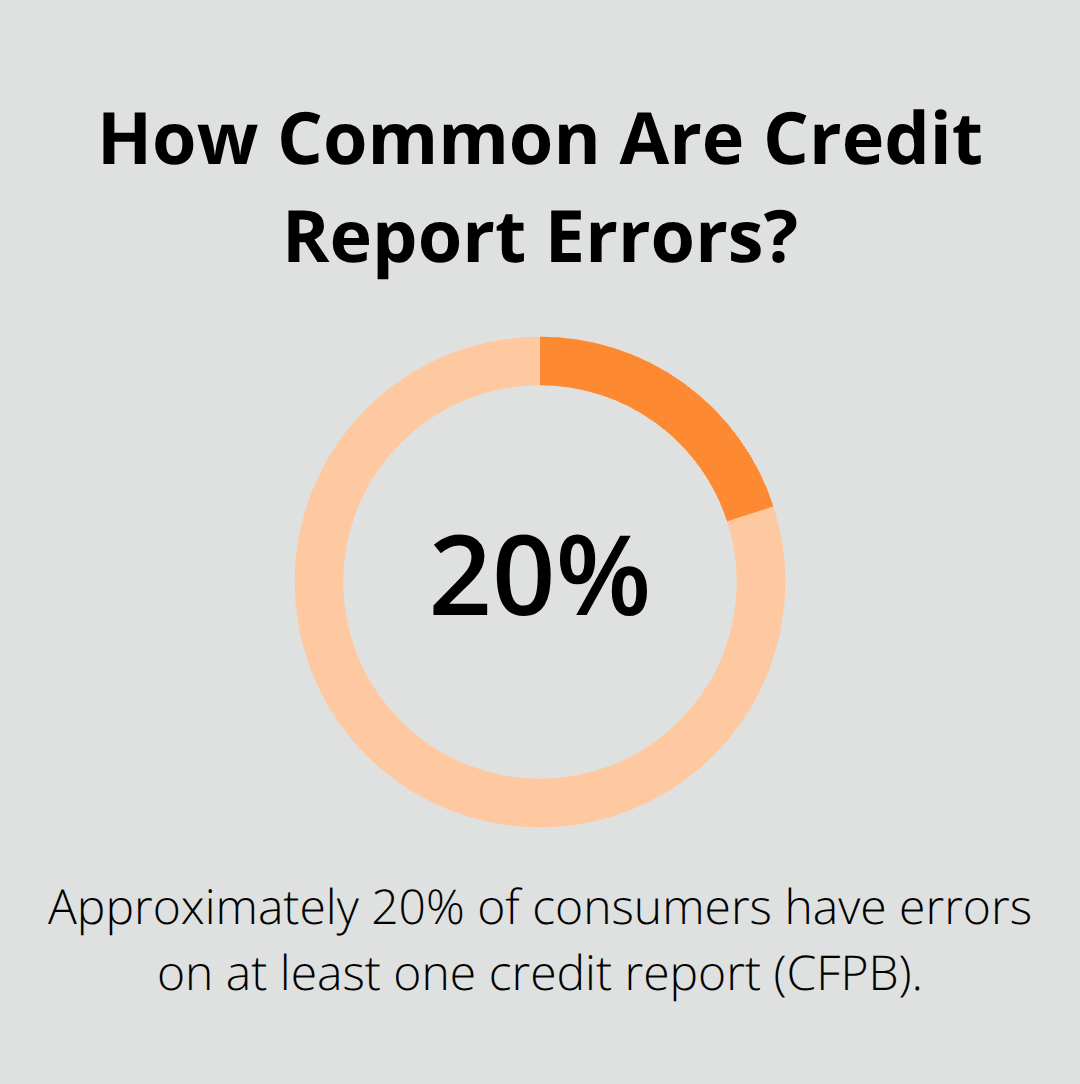

Wrong names, duplicate accounts, and incorrect payment histories plague California credit reports far more often than most people realize. According to the Consumer Financial Protection Bureau, approximately 20% of consumers have errors on at least one credit report. These aren’t rare edge cases-they’re widespread problems affecting millions of people’s financial opportunities.

Identity theft accounts for some errors, but many stem from simple data entry mistakes or mixed files where accounts belonging to someone with a similar name attach to your record. Furnishers report outdated information long after accounts close. Lenders, collection agencies, and credit bureaus themselves all play roles in how errors originate. When a creditor reports your account to Equifax, Experian, or TransUnion, they carry responsibility for accuracy, but bureaus also fail to properly verify information before adding it to your file.

Common Problems That Appear on Reports

Closed accounts remain listed as open. Balances get recorded incorrectly. Payment dates shift by months or years. The system relies on data providers reporting correctly and bureaus catching problems-both frequently fail. California residents face the same vulnerabilities as everyone else, though you have stronger legal protections to fight back.

The Real Cost of Errors on Your Wallet

A single error triggers a cascade of financial damage. Higher interest rates on mortgages, auto loans, and credit cards cost you tens of thousands of dollars over time. Loan denials happen outright when your report shows delinquencies that never occurred.

Auto insurance companies use credit data to set premiums, meaning an error can inflate your rates significantly. Employers, landlords, and utility companies pull credit reports too, so inaccurate information can cost you jobs and housing. The damage compounds because most people don’t catch errors until they apply for credit and receive rejection or terrible terms. You might carry an error for years without knowing it exists.

This is why California law gives you powerful rights to dispute and correct information-the financial stakes are genuinely high. Catching errors early matters enormously. Understanding your rights under both federal and California law puts you in position to act quickly when problems appear on your record.

Your Rights Under California and Federal Law

The Dual Legal Framework Protecting You

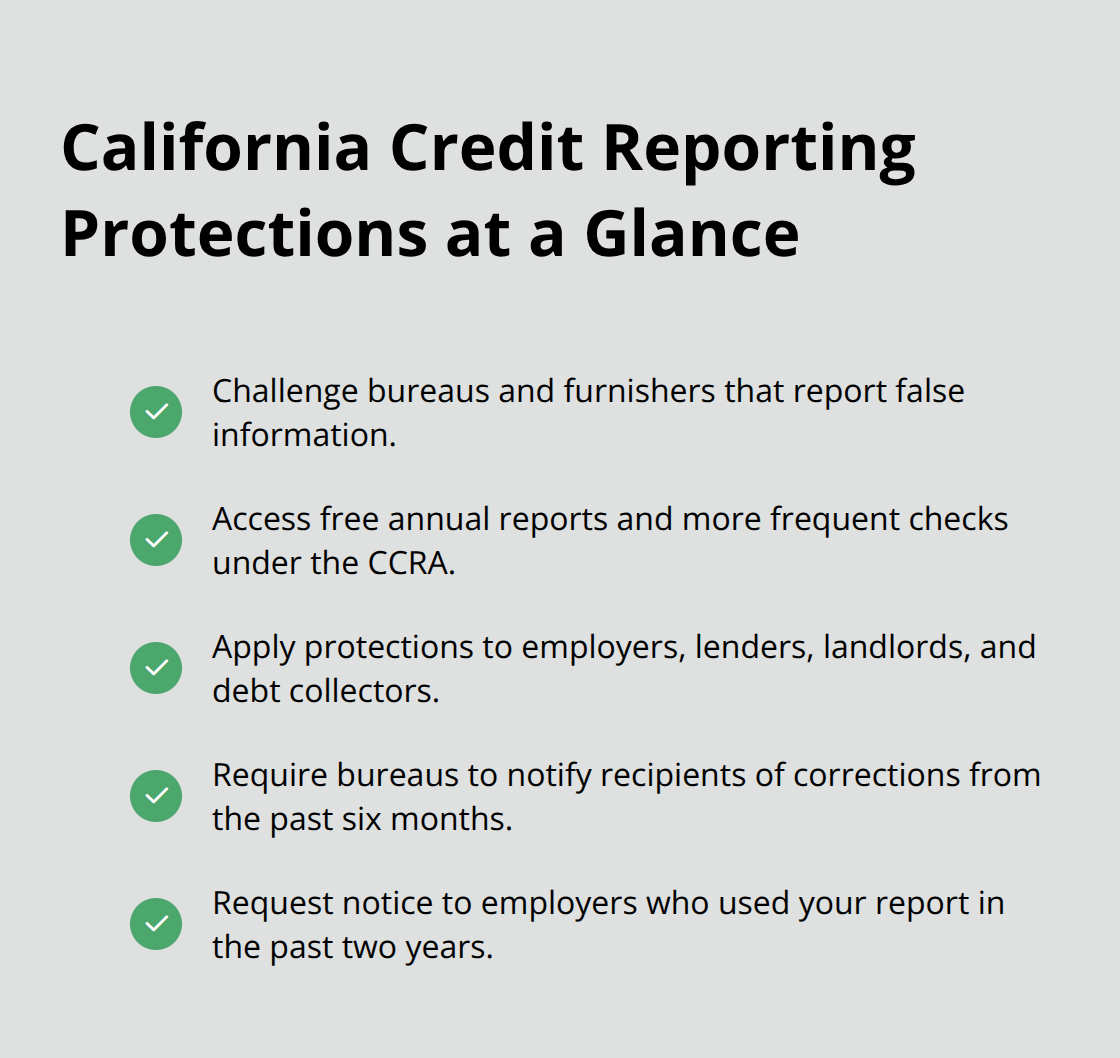

California residents operate under a dual legal framework that gives you stronger protections than most Americans realize. The Fair Credit Reporting Act sets federal baseline requirements that apply everywhere, but California’s Consumer Credit Reporting Agencies Act layers additional safeguards on top. The FCRA mandates that credit bureaus maintain only accurate, complete, and verifiable information about you. Furnishers-the creditors and collection agencies reporting data-must investigate disputes within 30 days and correct inaccurate information across all three bureaus if they find an error.

California’s Additional Protections

The CCRA extends these protections further by applying to any entity that uses or provides credit data in California, including employers, lenders, landlords, and debt collectors. This means you can challenge not just the bureaus themselves but also the companies reporting false information. Both laws grant you the right to access your credit reports free annually from AnnualCreditReport.com, and under the CCRA you can access them more frequently. The bureaus must notify anyone who received your report in the past six months of any corrections you obtain, and anyone who received it for employment purposes in the past two years if you request it.

Filing Disputes with Credit Bureaus

When you dispute an error, you have two critical paths. First, contact the credit reporting company-Equifax, Experian, or TransUnion-that has the inaccuracy on file. File your dispute online, by phone, or by mail with written documentation of why the information is wrong. Include copies of supporting documents like statements or payment confirmations, and send disputes by certified mail with tracking so you have proof of delivery.

Disputing Directly with Furnishers

Second, dispute directly with the furnisher, the company that originally reported the false information to the bureaus. This dual approach matters because furnishers often correct errors at the source faster than bureaus investigate them. The furnisher must then notify all three bureaus to update their records. If the investigation finds the information inaccurate, you receive a free updated credit report and the bureaus must send correction notices to creditors who accessed your report.

When Disputes Stall and What Comes Next

If disputes stall or the bureaus refuse to correct verified errors, file complaints with the Consumer Financial Protection Bureau and Federal Trade Commission, and in California you can escalate to the California Department of Financial Protection and Innovation or the state Attorney General’s office. Documentation matters enormously-keep detailed records of all communications, dispute numbers, response dates, and any corrections made. If unresolved disputes cause tangible financial damage like denied loans or higher interest rates, consulting a consumer protection attorney becomes the logical next step to explore whether violations occurred and what remedies apply. Understanding these pathways positions you to take action when problems surface on your record.

How to Actually Fix Your Credit Report

Get Your Reports and Spot the Problems

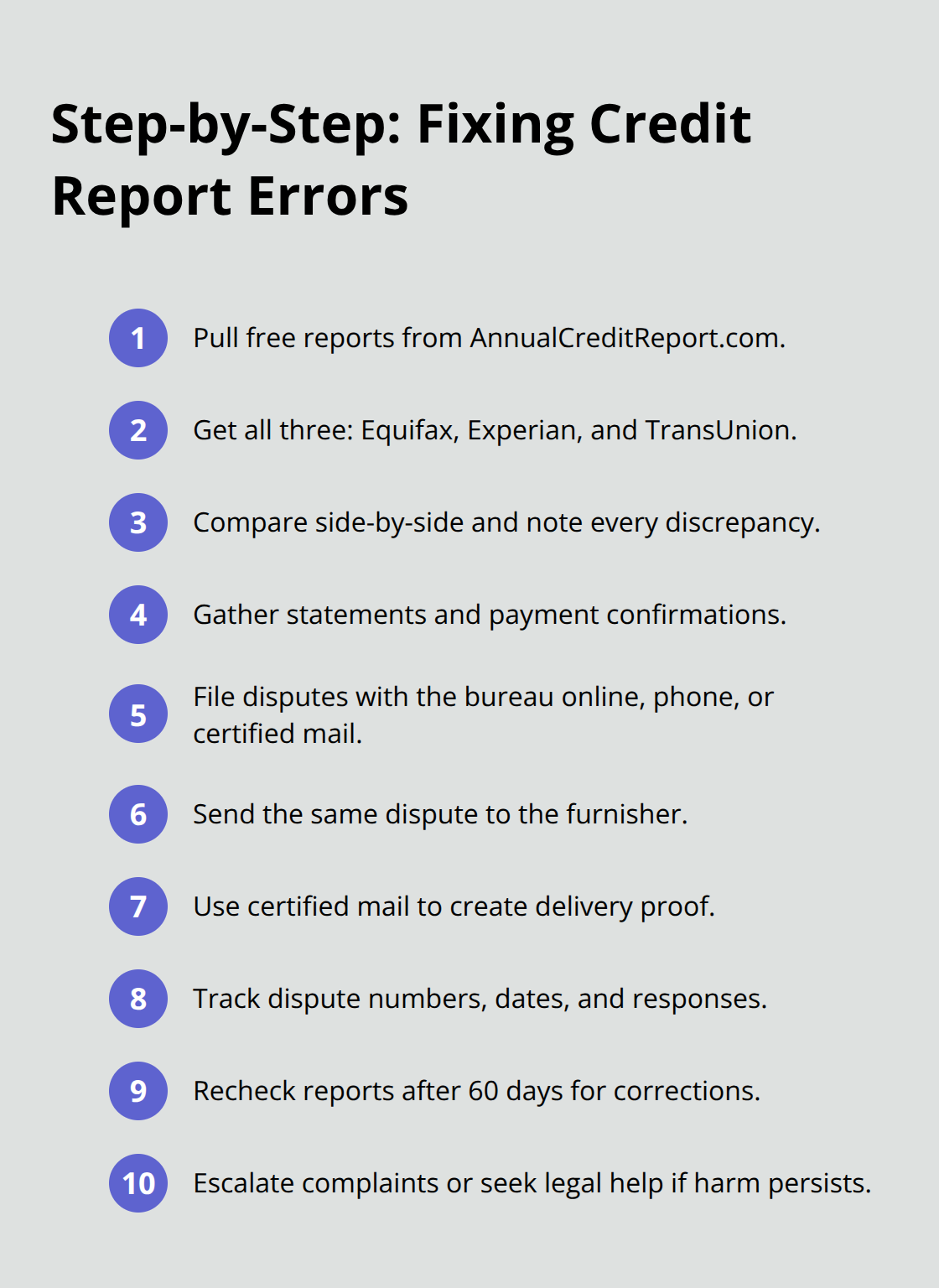

Pull your actual credit reports from AnnualCreditReport.com, the official source endorsed by the Federal Trade Commission. Request all three reports from Equifax, Experian, and TransUnion at once so you can compare them side-by-side. Many people find different errors on different bureaus, and you need to see all three to catch everything. The reports arrive free within 15 days, and this costs nothing. Once you have them in hand, scan each report line-by-line for accounts you don’t recognize, wrong names or addresses, closed accounts still showing as open, incorrect balances, or payment dates that don’t match your records. Write down every error you find with the exact account name, account number, and the specific inaccuracy. This documentation becomes your roadmap for disputes.

File Disputes with Both the Bureau and the Furnisher

Contact both the credit bureau and the furnisher simultaneously when you identify errors. File disputes with the bureau online, by phone, or by certified mail with return receipt-certified mail creates proof of delivery that matters if disputes go unresolved. Include a clear written explanation of why the information is wrong, attach copies of supporting documents like billing statements or payment confirmations, and reference the specific account and error. Send the same dispute to the furnisher, the company that originally reported the false information.

The furnisher must investigate within 30 days and notify all three bureaus if they find the information inaccurate.

Track Your Progress and Verify Corrections

After filing, track everything: keep dispute numbers, dates sent, copies of what you submitted, and all responses received. Check your credit reports again after 60 days to confirm corrections appeared. If errors persist after 30 days, file complaints with the Consumer Financial Protection Bureau and Federal Trade Commission. California residents can also file with the California Department of Financial Protection and Innovation. If corrections never arrive and the errors caused tangible harm (like loan denials or higher interest rates), legal action may be an option to evaluate whether the bureaus or furnishers violated the Fair Credit Reporting Act or California’s Consumer Credit Reporting Agencies Act.

Conclusion

Credit report errors in California can derail your financial future, but you hold the power to fix them. You have concrete legal rights under both the Fair Credit Reporting Act and California’s Consumer Credit Reporting Agencies Act that allow you to obtain free copies of your reports, identify inaccuracies, and file disputes with bureaus and furnishers within 30 days. Documentation matters enormously-keep records of every dispute, response date, and correction to build a solid paper trail.

Many people resolve credit report errors on their own by pulling reports from AnnualCreditReport.com, spotting problems, and filing written disputes with supporting documents. However, some situations demand professional help: when bureaus or furnishers ignore your disputes, when errors cost you a job or housing opportunity, or when you suspect violations of consumer protection law. An attorney can draft demand letters that prompt faster responses, file formal complaints, and evaluate whether you have grounds for damages.

If the process stalls or errors caused tangible financial harm, contact us for a free case review to understand your options without obligation. We represent California residents in credit reporting disputes and related consumer protection claims, and we can help you navigate these disputes and hold companies accountable.