Your credit report affects everything from loan approvals to job opportunities. Inaccuracies on that report can derail your financial future, and credit bureaus don’t always get it right.

At Bontrager Law, we help California consumers understand and enforce their rights under the Fair Credit Reporting Act. This guide walks you through what protections you have, how violations happen, and what steps to take if your credit report contains errors.

What the FCRA Actually Protects

The Fair Credit Reporting Act is a federal law passed in 1970 that regulates how credit bureaus collect, store, and distribute your financial information. The FCRA applies to all three major credit bureaus-Equifax, Experian, and TransUnion-and it gives California consumers concrete rights that most people don’t know they have. Credit bureaus hold enormous power over your financial life. A single error on your credit report can cost you thousands in higher interest rates, trigger loan denials, or destroy job opportunities. The FCRA requires credit bureaus to maintain accurate information and investigate disputes within 30 days. If they fail, you have the right to pursue legal action. The Consumer Financial Protection Bureau processes over 100,000 consumer complaints each week, and many involve credit reporting errors that could have been prevented if consumers understood their rights.

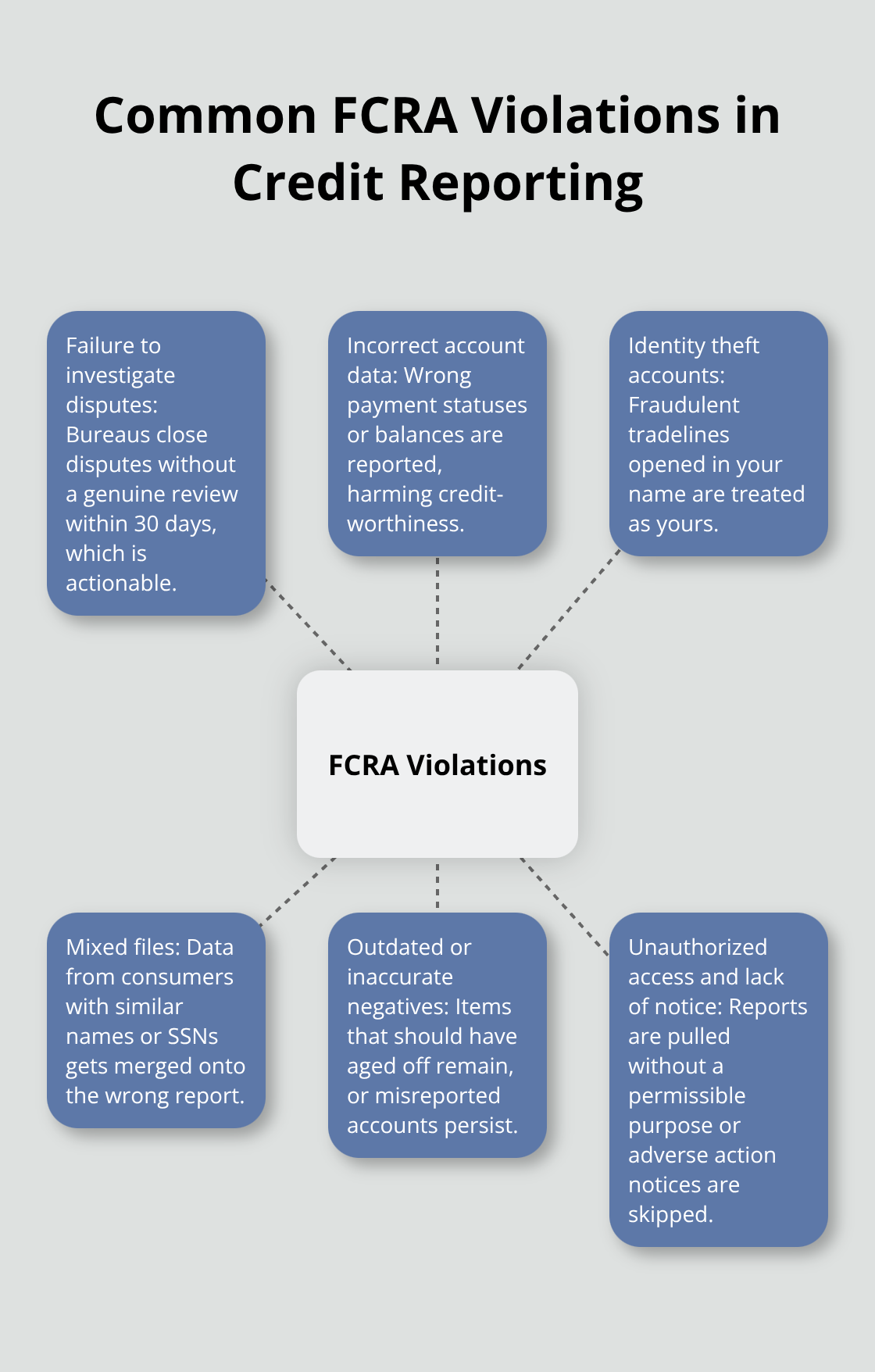

How Violations Actually Happen

Credit bureaus routinely fail to investigate disputes properly, which is itself a violation you can challenge. Inaccurate information appears on reports through multiple channels: creditors report wrong payment statuses, identity theft creates fraudulent accounts in your name, or the bureaus simply mix up files between consumers with similar names. The FTC’s Legal Library documents that common violations include incorrect personal information, outdated negative marks that should have been removed, misreported accounts, and unauthorized access to your report by third parties without a permissible purpose. If a lender, employer, or landlord takes adverse action based on your credit report, they must notify you-and many don’t, which is itself a violation.

Finding Errors Before They Cost You

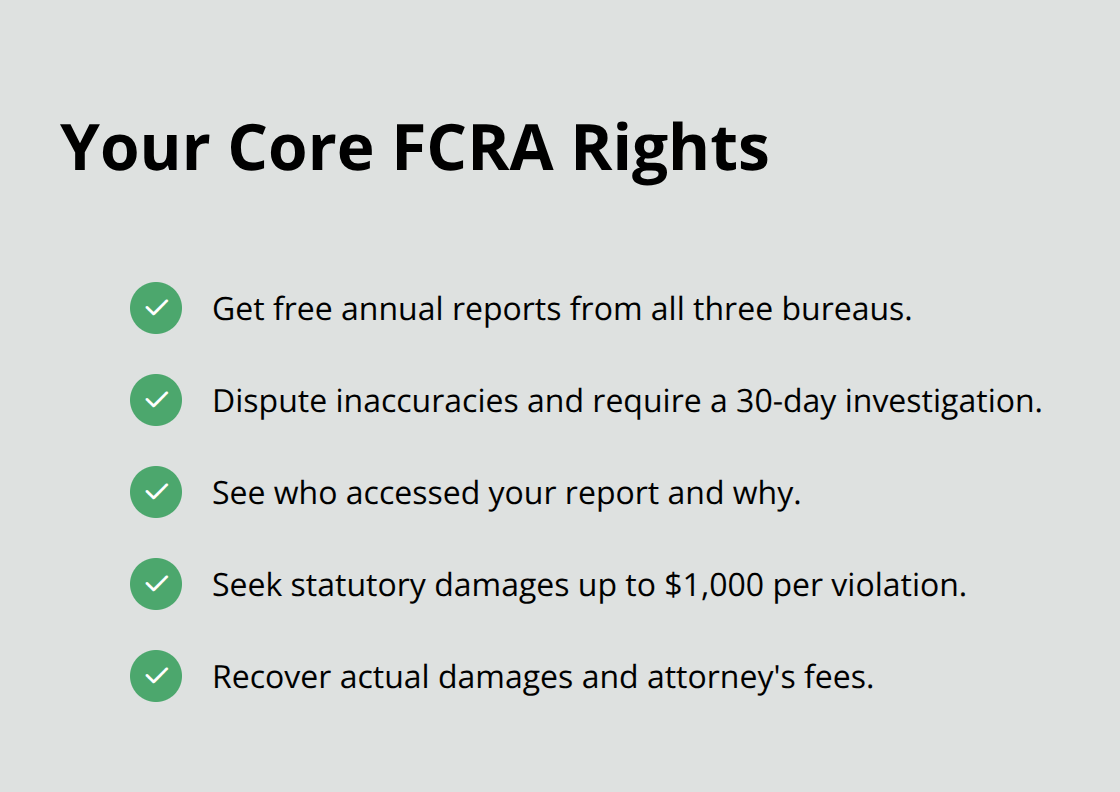

You can access free annual copies of your credit reports from all three bureaus through AnnualCreditReport.com, and pulling these reports is your first step to identifying errors. When you file a dispute, the bureau must investigate, but if they don’t conduct a genuine investigation or ignore supporting documents you provide, that failure creates liability. California consumers can recover actual damages, statutory damages up to $1,000 per violation, and attorney’s fees if they pursue legal action-making it worth fighting back when bureaus ignore your rights. Understanding these violations positions you to take the next critical step: knowing exactly what rights you hold under the FCRA and how to exercise them.

Your Rights Under the FCRA

Access Your Credit Reports for Free

The FCRA grants you the unconditional right to access your credit reports from all three bureaus at no cost once per year through AnnualCreditReport.com. This isn’t a suggestion-it’s a federal right. The CFPB receives over 100,000 consumer complaints weekly, and many stem from errors that consumers could have caught by simply reviewing their reports.

When you pull your report, look for red flags: accounts you didn’t open, payment statuses that don’t match your records, personal information that’s wrong, or negative items that should have aged off. Negative marks typically fall off after seven years, so if you see a charge-off from 2015 still reporting in 2026, that’s a violation you can challenge.

Dispute Inaccurate Information Effectively

You have the right to dispute any inaccurate credit information you believe is inaccurate, and the bureau must investigate your claim within 30 days. Most consumers file weak disputes that say nothing more than “this is wrong.” The FTC’s Legal Library confirms that strong disputes include specific facts, dates, and supporting documents like payment records or statements proving the account doesn’t belong to you. If the bureau fails to investigate, ignores your supporting documents, or simply re-verifies the information without actually contacting the creditor, that failure is itself a violation you can pursue legally. Sloppy investigations-where bureaus don’t even attempt to contact the furnisher or rely on outdated verification methods-expose them to damages up to $1,000 per violation under the FCRA.

Know Who Accesses Your Report

You have the right to know who accessed your credit report and for what purpose. Unauthorized access by someone without a permissible purpose is illegal and actionable. If a potential employer pulled your report without your consent, or a creditor accessed it without a legitimate reason, that violation can result in actual damages plus statutory damages and attorney’s fees. These three rights form the foundation of your FCRA protections, but knowing them means nothing without taking action when violations occur. The next step involves understanding how to file a dispute and when legal representation becomes necessary to hold credit bureaus accountable.

How to Take Action Against FCRA Violations

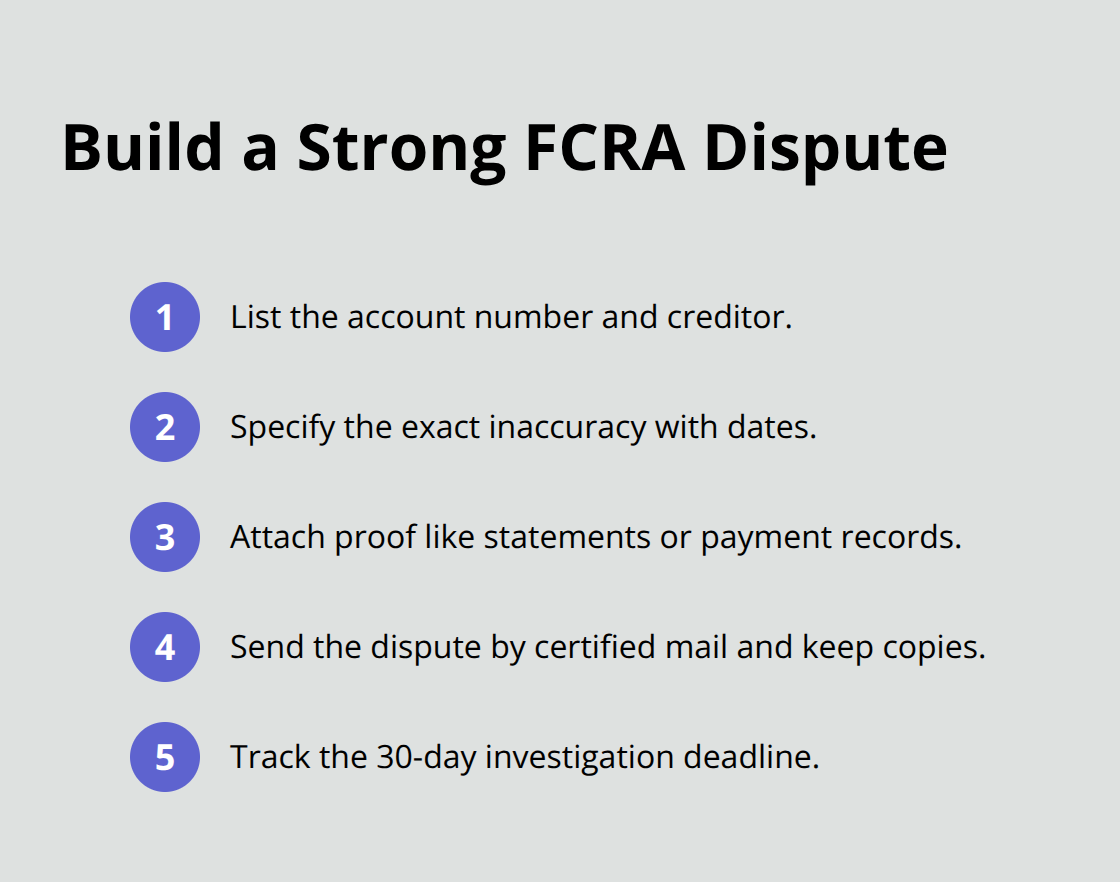

File a Detailed Dispute with Supporting Documents

A vague dispute stating “this is wrong” gives credit bureaus an easy escape route. The CFPB’s Legal Library confirms that strong disputes include the specific account number, the exact inaccuracy you’re challenging, relevant dates, and supporting documents like payment records or statements proving the account isn’t yours.

When you send written disputes using certified mail with return receipt requested and keep copies of everything, you create a documented trail. The bureau has 30 days to investigate, contact the creditor furnishing the information, and respond to you. If they ignore your supporting documents, fail to contact the furnisher, or simply re-verify without actual investigation, that negligence creates legal liability. The FTC enforces FCRA compliance, and bureaus know this-so a detailed, documented dispute with clear evidence forces them to take action or face violations.

Document Every Communication

Save emails, letters, dispute responses, and any denial notices. This documentation becomes critical if you later need legal representation to prove the bureau’s failure to investigate properly. Most consumers overlook this step and later struggle to demonstrate what happened during the dispute process. Your records show whether the bureau actually investigated or merely went through the motions. Courts and attorneys rely on this paper trail to establish violations and calculate damages.

Recognize When You Need Legal Representation

Many consumers wait too long before contacting an attorney, thinking they can resolve violations alone. If a bureau ignores your dispute after 30 days, fails to investigate, or continues reporting inaccurate information after your challenge, contacting a California FCRA attorney becomes necessary. The FCRA allows statutory damages up to $1,000 per violation, meaning multiple inaccuracies or repeated failures to investigate can result in substantial recovery. You can also recover actual damages-the real financial harm the errors caused you, such as higher interest rates on loans or denied credit. If the bureau’s violations were willful rather than negligent, punitive damages may apply. Attorney’s fees are recoverable as well, so hiring representation doesn’t require upfront costs when violations are clear. Most California FCRA attorneys work on contingency, meaning you pay nothing unless you win.

Act Within the Statute of Limitations

Violations have statutes of limitations, so waiting years to act weakens your case. If a bureau fails to correct inaccuracies within 30 days of your dispute or continues unauthorized access to your report, that window for legal action remains open now. We offer free case reviews to evaluate whether violations occurred and what damages you may recover. The key is timing-contact an attorney as soon as a bureau demonstrates it won’t correct errors or investigate your dispute properly.

Final Thoughts

Your credit report shapes your financial reality, and the FCRA gives you concrete tools to protect it. You have the right to access your reports for free, dispute inaccuracies with supporting documents, and know who accesses your information. Credit bureaus must investigate disputes within 30 days, and when they fail-by ignoring your evidence, skipping genuine investigation, or continuing to report errors-that failure creates legal liability.

Taking action yourself starts with pulling your free reports and filing detailed disputes with documentation. Many consumers hit a wall when bureaus ignore their challenges or continue reporting inaccurate information, and that’s when an FCRA lawyer California can navigate the dispute process more effectively and hold bureaus accountable. Statutory damages reach $1,000 per violation, actual damages cover real financial harm, and attorney’s fees are recoverable-meaning you don’t pay upfront costs when violations are clear.

Don’t wait years to act, as statutes of limitations apply and delay weakens your position. If a bureau has ignored your dispute or continues reporting errors after your challenge, contact us for a free case evaluation today.