A single error on your credit report can tank your score and cost you thousands in higher interest rates. Yet millions of Americans discover inaccuracies every year that go unaddressed.

We at Bontrager Law help people fight back against credit reporting mistakes. This guide walks you through proven credit report error remedies, from disputing inaccuracies yourself to pursuing legal action when bureaus refuse to correct the record.

How Credit Report Errors Actually Happen

Errors Are Systemic, Not Accidental

Credit report errors aren’t rare accidents-they’re systemic problems baked into how the credit reporting industry operates. A non-representative sample of over 4,000 participants in Credit Checkup found that 44% discovered at least one mistake on their credit report. That’s nearly half of all people checking their files. The errors fall into distinct categories that repeat across millions of files.

The Main Types of Errors That Appear on Reports

Account information errors affect 27% of people who find mistakes, showing up as unrecognized accounts, incorrect late payments, or debts in collections that don’t belong to them at all. Personal information errors hit 34% of those with mistakes, including wrong names or addresses that create confusion between similar profiles. Mixed files occur when information from someone with a nearly identical name or Social Security number bleeds into your report. Fraudulent accounts and identity theft also appear regularly, turning your credit report into a dumping ground for someone else’s debt or criminal activity.

How Errors Damage Your Financial Life

A single inaccuracy can lower your credit score significantly, which directly translates to higher interest rates on mortgages, auto loans, and credit cards. An error might cost you thousands in additional interest over the life of a loan. Beyond borrowing costs, credit report errors affect job applications, housing opportunities, and insurance premiums.

The Scale of the Problem

The Consumer Financial Protection Bureau tracked consumer complaints about credit reporting errors for three years running, and the numbers exploded from 165,129 complaints in 2021 to 430,600 in 2023-a 161% increase that shows how frustrated people are becoming. A 2013 FTC study found that one in five consumers had an error on at least one of their three credit reports, and one in four identified errors that might damage their scores. The same study showed that four in five consumers who filed disputes experienced some modification to their credit report afterward, proving that action works.

Access Barriers Keep People in the Dark

Yet 25% of participants initially couldn’t access their credit reports at all, blocked by security questions or error messages that locked them out of the system. This access problem means millions of people don’t even know what errors exist in their files until they apply for credit and get rejected. These barriers prevent people from taking the first step toward fixing their credit-and that’s where the dispute process begins.

Steps to Dispute Credit Report Errors

Pull Your Reports and Spot the Problems

Start at AnnualCreditReport.com, the official government-backed site for free annual reports from all three bureaus. Equifax currently offers six additional free reports per year through December 31, 2026, so pull those too if you want to monitor changes more frequently. Print or save each report and read through line by line. Look for account information errors like unrecognized accounts, incorrect late payment dates, or debts showing in collections that aren’t yours. Check personal information errors including wrong names, addresses, or Social Security numbers that might indicate a mixed file from someone else’s data bleeding into yours. Circle or highlight every inaccuracy you find. A 2013 FTC study showed that one in four consumers identified errors that might affect their credit scores, so take your time here-this step determines everything that follows.

File Your Dispute with the Credit Bureau

File a dispute directly with the credit bureau through their official online portal, by mail, or by phone. Equifax, Experian, and TransUnion each maintain dispute channels on their websites. When you dispute, be specific about which accounts and items are wrong and explain exactly why. The credit bureau must investigate and forward your dispute to the furnisher-the original creditor or data provider-within a few days. Furnishers typically respond within about 30 days, and if the information is wrong or unverifiable, they must update or remove it across all three bureaus.

Document Everything and Track Progress

Mail your dispute letter by certified mail with return receipt requested so you have proof of delivery. Include your full name, address, phone number, credit report confirmation number if available, every item you want fixed, a clear explanation of why it’s incorrect, and a specific request to remove or correct the item. Keep copies of everything-your dispute letter, supporting documents, and proof of delivery. Track each dispute’s progress by noting the date you sent it and checking back after 30 days to verify changes appeared on your reports.

Know When to Escalate

A 2013 FTC study found that four in five consumers who filed disputes experienced some modification to their credit report, meaning persistence pays off. However, if the bureaus or furnishers don’t respond or refuse to correct legitimate errors after you’ve disputed multiple times, escalation becomes necessary. The Fair Credit Reporting Act provides legal remedies when credit bureaus violate their obligations to investigate disputes thoroughly and correct inaccurate information.

When Credit Bureaus Refuse to Correct Errors

The Fair Credit Reporting Act Protects You

The Fair Credit Reporting Act gives you a legal foundation to fight back when credit bureaus and furnishers ignore your disputes or fail to investigate properly. Under the FCRA, credit bureaus must investigate disputes within 30 days and report results back to you. If they don’t investigate thoroughly, ignore your claim entirely, or refuse to correct information you’ve proven wrong, you have grounds for legal action. The law also requires furnishers to investigate disputes from bureaus and correct or remove inaccurate data within roughly 30 days.

What Happens When Bureaus Violate the Law

When these obligations go unfulfilled, you can file a complaint with the Consumer Financial Protection Bureau, which tracked 430,600 credit reporting complaints in 2023 alone-a massive jump from 165,129 in 2021. The CFPB takes these complaints seriously and has enforcement power against bureaus that systematically fail consumers. Beyond CFPB complaints, the FCRA allows you to sue credit bureaus and furnishers directly for violations. You can recover actual damages (like costs from a denied loan or higher interest rates), statutory damages up to $1,000 per violation, and attorney fees if you win.

Why Most People Don’t Know About Legal Remedies

Most people don’t realize they have legal remedies because the dispute process works silently in the background. However, if you’ve disputed errors multiple times through official channels and nothing changes, working with a consumer protection attorney becomes your strongest option. An attorney can send formal demand letters that carry weight furnishers and bureaus ignore from consumers alone.

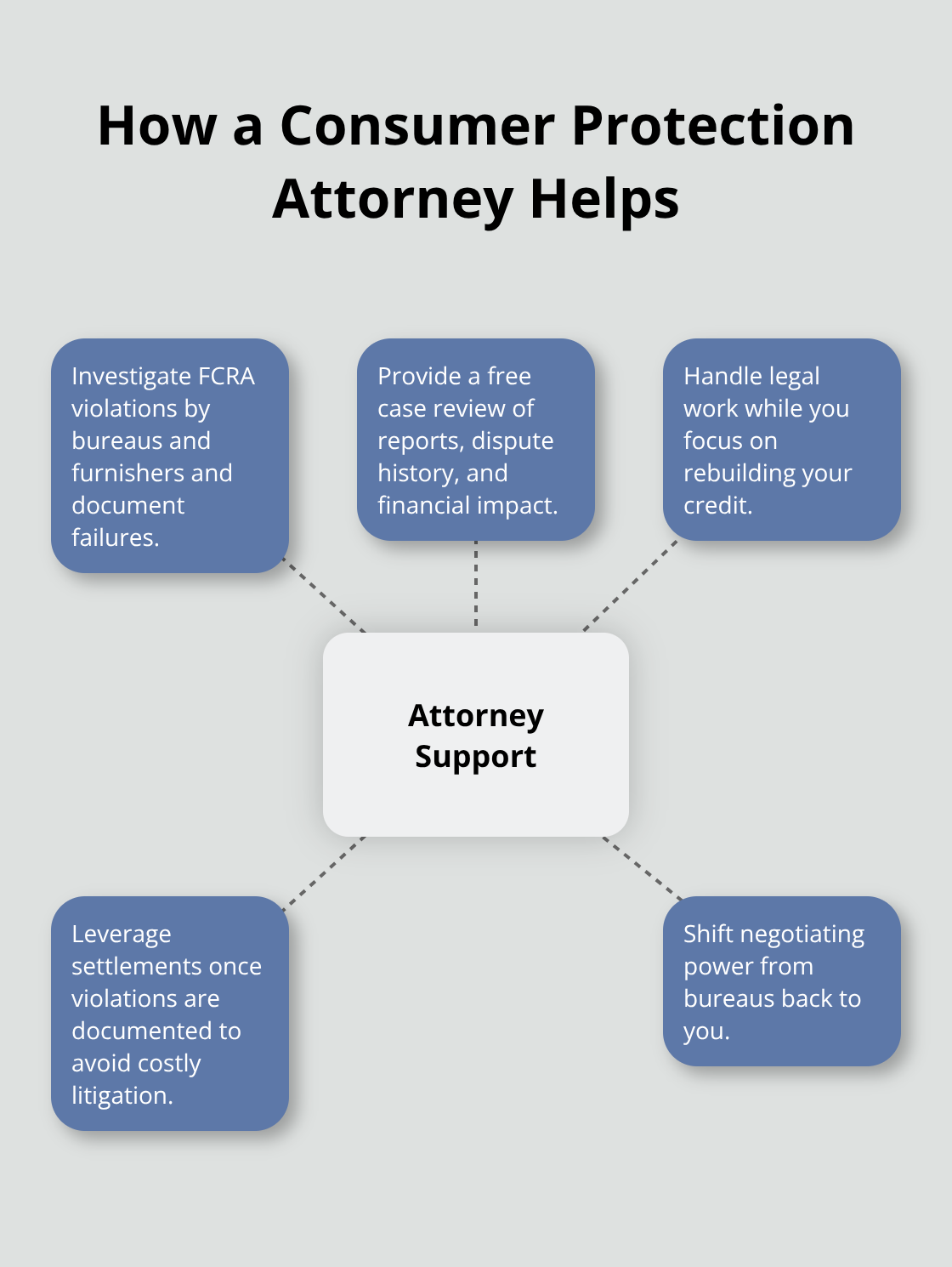

How a Consumer Protection Attorney Can Help

A consumer protection attorney investigates whether the bureaus and furnishers violated FCRA requirements, documents their failures, and pursues claims that recover damages for the harm errors caused you. The process starts with a free case review where an attorney examines your credit reports, dispute history, and financial impact. If violations exist, the attorney handles the legal work while you focus on rebuilding your credit.

Many cases settle when bureaus realize an attorney is involved and violations are documented, avoiding costly litigation. This approach works because it shifts leverage from the bureaus back to you.

Final Thoughts

Credit report errors fade over time, but they damage your finances while they remain. Negative items stay on your report for seven to ten years depending on the type, though recent errors carry more weight than older ones. A 2013 FTC study found that slightly more than one in ten consumers saw a change in their credit score after errors were corrected, with some experiencing improvements of 25 points or more.

Pull your free credit reports from AnnualCreditReport.com at least once yearly, or use Equifax’s six additional free reports available through December 31, 2026 for more frequent checks. Review each report line by line and dispute anything suspicious immediately. Pay bills on time consistently, keep credit utilization below 30%, and avoid applying for multiple accounts in short periods-these habits build positive history while preventing the mistakes that plague millions of Americans.

If you’ve already disputed errors multiple times without results, credit report error remedies through legal action may be your next step. We at Bontrager Law represent individuals across California in credit reporting disputes and related claims against bureaus and furnishers. Start with a free case review to understand your options and whether violations occurred.