Wage garnishment can take a significant portion of your paycheck before it even reaches your bank account. California law does provide protections, but many workers don’t know how to use them.

At Bontrager Law, we help people stop wage garnishment and recover their financial stability. This guide walks you through your rights and the steps to fight back.

How Wage Garnishment Actually Works in California

The Court Order Requirement

Wage garnishment in California follows a specific legal process that starts with a court judgment. A creditor cannot simply take money from your paycheck without first winning a lawsuit against you and obtaining a Writ of Execution. Once they have that court order, they serve an Earnings Withholding Order on your employer, who then withholds the specified amount from your wages and sends it to the levying officer, usually the sheriff.

California’s Garnishment Limits

California caps wage garnishments at the lesser of 25% of your disposable earnings or the amount by which your weekly disposable income exceeds 48 times the state minimum wage, which is currently $16.50 per hour. If you earn $1,000 per week after taxes and required deductions, the maximum garnishment would be $250 per week. The federal Consumer Credit Protection Act works alongside California law to enforce these limits and prevents your employer from firing you for a single wage garnishment.

Tax Garnishments and Special Cases

Some debts bypass the normal court process entirely. Tax garnishments from the Franchise Tax Board follow different rules and can be issued without a traditional judgment, targeting past-due income tax obligations directly through an Earnings Withholding Order for Taxes.

The Critical 10-Day Window

The timeline matters significantly. Garnishment typically cannot begin until about 30 days after a judgment is entered, which gives you a critical window to act. Your employer must provide you a copy of the Earnings Withholding Order within 10 days of receiving it, and you have exactly 10 days from that notice to file a Claim of Exemption if you believe the garnishment would deprive you of basic necessities. This 10-day deadline is absolute and worth marking on your calendar immediately. If you miss it, stopping the garnishment becomes substantially harder.

Understanding Disposable Earnings

Disposable earnings are calculated as wages minus legally required deductions like income taxes, Social Security, and unemployment insurance, but not voluntary deductions like health insurance or retirement contributions you chose. The garnishment continues indefinitely until either the debt is paid in full or you successfully challenge it through an exemption claim or other legal action. Understanding this timeline and these calculations is fundamental, because waiting too long or miscalculating what counts as disposable income can cost you thousands of dollars. Now that you understand how the system works, your next step is to learn what protections California law actually gives you.

Your Legal Rights and Protections Against Wage Garnishment

Protected Income You Cannot Lose

California law shields certain income from creditors entirely. Social Security benefits, unemployment insurance, disability payments, and public assistance remain off-limits regardless of your debt amount. If you receive these payments, they should never appear in the garnishment calculation. Pension income also receives strong protection under California law, though the rules vary depending on the pension type. These categorical exemptions form the foundation of worker protection in the state.

Filing a Claim of Exemption

You can file a Claim of Exemption if the garnishment would prevent you from paying for basic necessities like food, shelter, utilities, and transportation. This protection is not theoretical-California courts grant these claims regularly when workers present solid evidence of hardship. The California Courts Self Help Guide provides the official forms: the Claim of Exemption (WG-006) and Financial Statement (WG-007/EJ-165). You must file these within 10 days of receiving the Earnings Withholding Order, and you need two copies. Keep one for yourself and file the original plus one copy with the levying officer, typically the sheriff, whose name appears on the garnishment order.

The creditor then has 10 days to respond. If they don’t respond, your claim is automatically granted and the sheriff stops or reduces the garnishment immediately. If the creditor opposes, you’ll receive a Notice of Opposition and a hearing date. Bring documentation to that hearing: recent pay stubs, bank statements showing your balance, and bills for rent, utilities, insurance, and other essentials. Courts require solid evidence that paying the garnishment would genuinely harm your ability to meet basic needs, not just that it’s inconvenient.

Challenging Garnishments on Other Grounds

You can challenge a garnishment by identifying a procedural defect or proving the underlying debt is incorrect or fraudulent. Common procedural errors include the creditor serving the garnishment order improperly, failing to provide you with required notice, or using an expired judgment. If the debt amount is wrong, the creditor violated the judgment, or the creditor obtained the judgment through fraud, you can file a motion to set aside the garnishment or the underlying judgment itself. In limited civil cases where the judgment is under $35,000, you can also file a motion to pay the judgment in installments, which stops the garnishment in favor of a structured payment plan.

Acting Quickly Protects Your Paycheck

Every week of delay means more money taken from your paycheck. The moment you receive a garnishment notice, contact a consumer protection attorney for a free case review. An attorney helps you file exemption claims, challenge invalid garnishments, and negotiate settlements that protect your income while resolving the underlying debt. Understanding your rights is the first step, but taking action within those critical deadlines determines whether you actually stop the garnishment. The next section shows how an attorney actively fights back against creditors and collection agencies on your behalf.

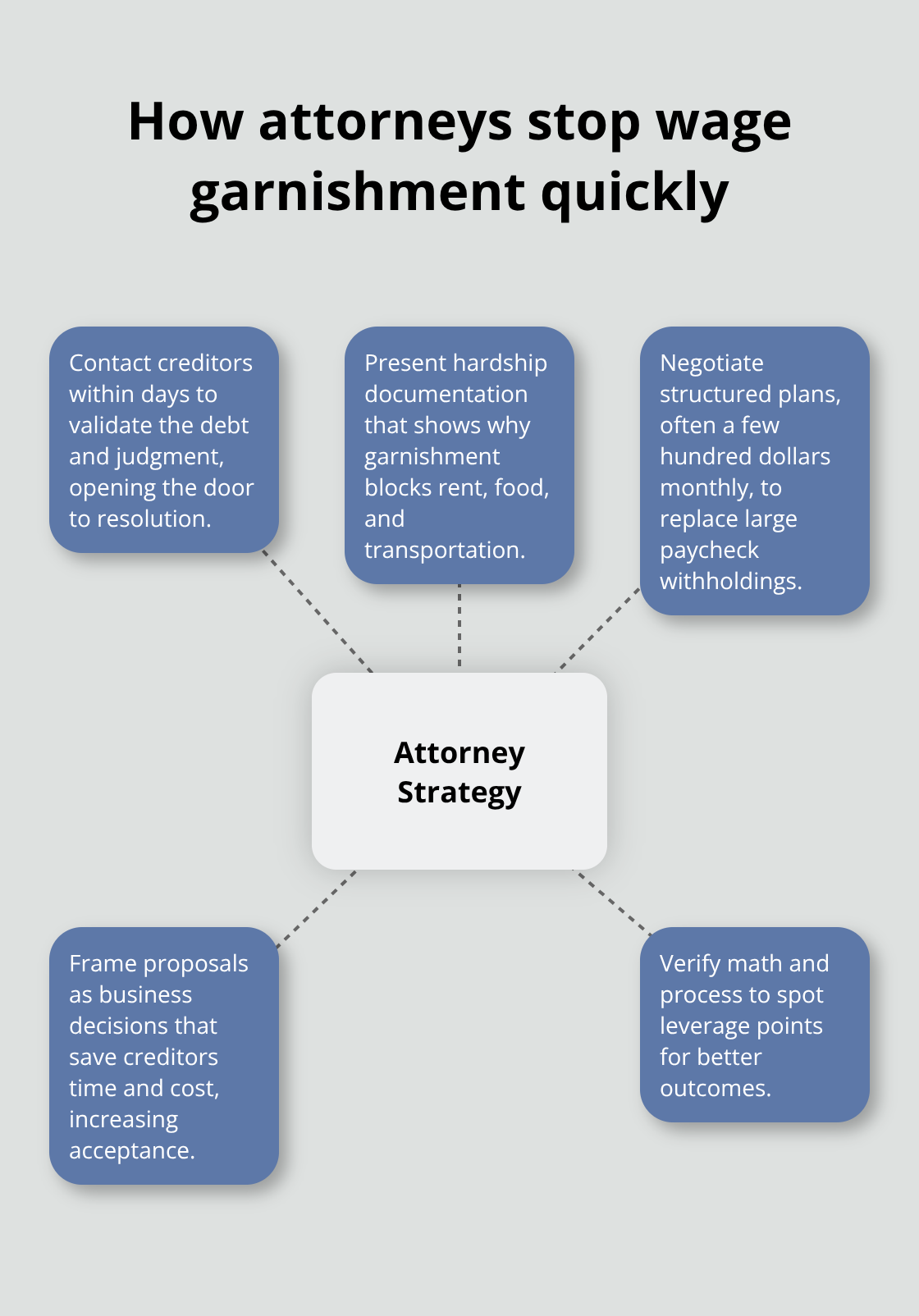

How a Consumer Protection Attorney Stops Wage Garnishment

Moving Fast Against the Clock

Time works against you when garnishment takes your paycheck. A consumer protection attorney contacts the creditor or collection agency within days to assess the debt’s validity, verify the judgment’s accuracy, and identify settlement or payment plan options. Many creditors prefer negotiation over continued garnishment because court involvement drains their resources and reduces recovery. An attorney presents your financial hardship documentation immediately, showing precisely how the garnishment prevents you from covering rent, food, and transportation. Creditors often accept structured payment arrangements of $200 to $500 monthly instead of continuing a garnishment that pulls $1,000 or more from your paycheck each month. The negotiation succeeds when presented as a business proposition rather than an emotional appeal.

Leveraging Weak Judgments and Procedural Errors

Cases with weak underlying judgments, calculation errors, or procedural violations provide leverage for settlement. An attorney identifies these defects and uses them to push creditors toward negotiated resolutions. Creditors frequently realize that accepting 60 or 70 cents on the dollar through settlement beats a prolonged garnishment that nets them less overall. If procedural defects exist-such as improper service of the garnishment order, missing notices, or an expired judgment-an attorney files motions challenging the garnishment’s validity. Some cases settle during these proceedings because creditors recognize their garnishment order contains errors or violates California’s strict procedural requirements.

Building Your Hardship Case

An attorney gathers your pay stubs from the last two months, bank statements showing your account balances, and documentation of all monthly expenses including rent, utilities, childcare, insurance, and medical costs. This evidence forms a detailed Financial Statement that demonstrates to the court exactly why the garnishment creates genuine hardship. Courts in California take hardship seriously when presented with solid documentation and regularly reduce or eliminate wage garnishment when evidence clearly shows the worker cannot afford basic necessities.

Representing You at Hearings and Beyond

When the creditor opposes your exemption claim, an attorney represents you at the hearing, presenting evidence and cross-examining the creditor’s representative about the debt’s legitimacy and your financial situation. An attorney also explores whether you qualify to pay the judgment in installments under California’s limited civil case rules, which halts the garnishment immediately in favor of a payment plan you can actually afford. If we discover procedural defects or other grounds for challenge, we file the appropriate motions and advocate for your rights throughout the process.

Final Thoughts

Wage garnishment in California removes money from your paycheck before you can pay rent, buy groceries, or cover medical bills. The system favors creditors, but California law provides real protections that work when you act within the legal deadlines. The 10-day window to file a Claim of Exemption, the ability to challenge procedural errors, and hardship exemptions exist to stop wage garnishment California situations from destroying your financial stability. Most workers don’t realize they can negotiate with creditors, file exemption claims that courts grant regularly, or challenge the underlying judgment if it contains errors.

A consumer protection attorney accelerates this process dramatically by contacting creditors immediately, identifying settlement opportunities, and building your hardship case with the documentation courts require. Rather than spending weeks gathering documents and filing forms yourself, an attorney catches procedural defects that give you leverage to challenge the garnishment entirely. Many creditors settle quickly when presented with solid evidence of financial hardship and the prospect of a court hearing, accepting structured payment arrangements instead of continued wage withholding.

We at Bontrager Law represent individuals across California in wage garnishment disputes and related debt collection matters. We start with a free case review to assess your situation, explain your rights, and outline the fastest path to protect your income. Contact us today to regain control of your paycheck.