Credit report errors in California are more common than most people realize, and they can damage your finances without you even knowing it. A single mistake on your credit report can lower your score, increase your interest rates, and affect your ability to get loans or housing.

The good news is that California law gives you strong protections to fight back. We at Bontrager Law help Californians identify and correct these errors so they can reclaim their financial standing.

Where Credit Report Errors Come From

The Three Main Sources of Inaccuracy

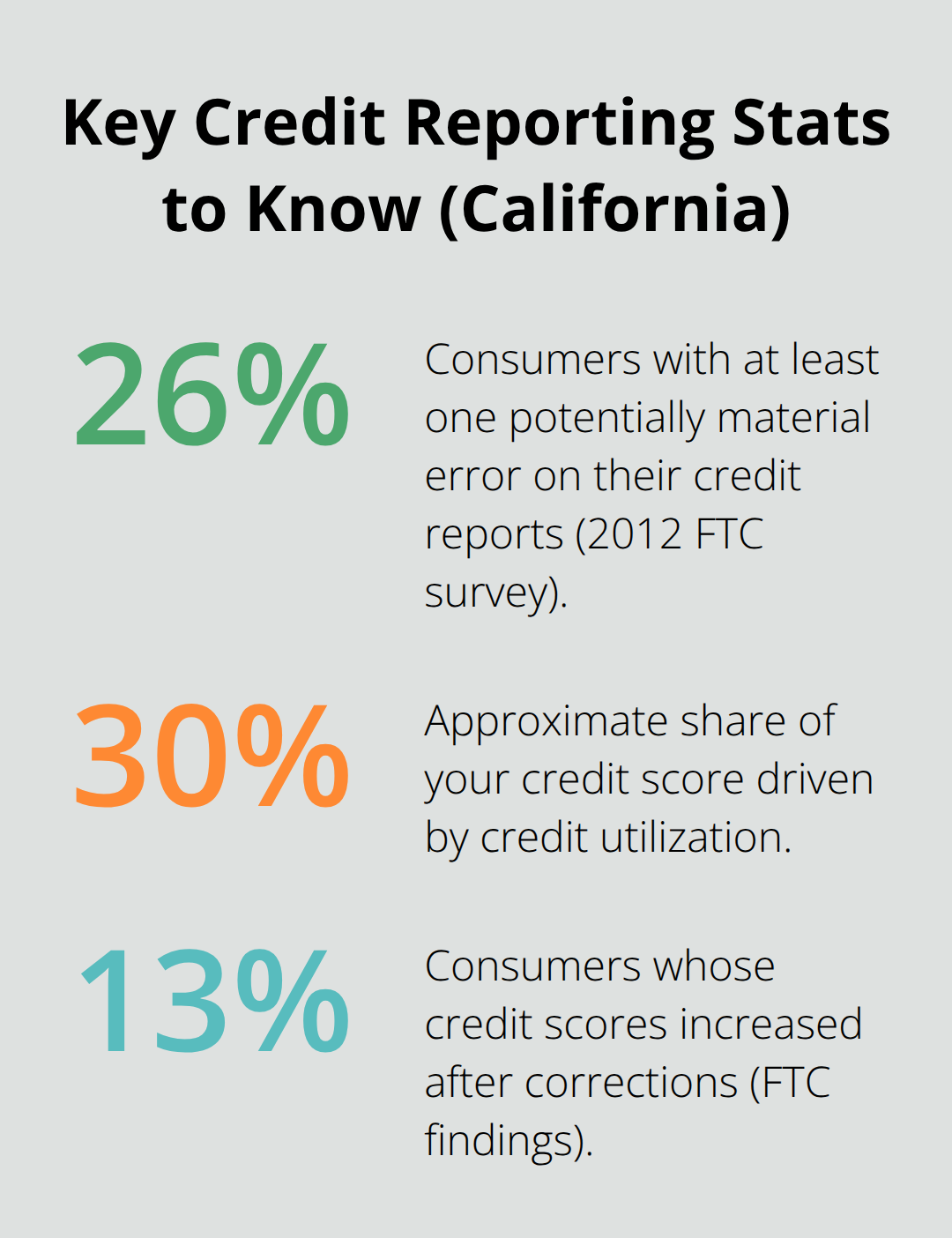

Credit report errors stem from three sources: data entry mistakes by creditors and debt collectors, merging of files when names or Social Security numbers are similar, and system failures at the bureaus themselves. A 2012 FTC survey found that 26 percent of consumers had at least one potentially material error on their credit reports, meaning millions of Californians face this problem. The most common mistakes include incorrect account status, wrong balances, late payments that should have been resolved, and accounts belonging to someone else entirely.

Misspelled names, outdated addresses, and duplicate accounts also appear frequently on credit files. Medical billing errors compound the problem-research shows that half or more medical bills contain billing errors, and those errors flow directly into your credit file. The scale of the problem is staggering: each major credit bureau manages over 200 million credit files and processes more than 1 billion data updates monthly, creating countless opportunities for inaccuracies to slip through.

Why the Dispute Process Fails Consumers

The dispute process itself favors creditors and collectors over consumers. When you file a dispute with a bureau, the bureau contacts the creditor or debt collector to verify the information. If the creditor simply stands by the claim, the dispute is often resolved in their favor-regardless of whether the information is actually correct. This means inaccurate data can remain on your report for seven years or longer unless you fight back aggressively.

The economic incentives built into credit reporting work against accuracy: bureaus profit from volume, not quality, and creditors benefit from inflated balances and false delinquencies. Additionally, if a dispute is deemed frivolous due to incomplete information, the bureau may skip the investigation entirely, leaving you stuck with the error. Many Californians give up after a single failed dispute, not realizing they can resubmit with new evidence or file complaints with the Consumer Financial Protection Bureau to trigger formal oversight.

The Real Cost of Staying Silent

A single error can cost you thousands in higher interest rates. If an account shows an incorrect balance, your credit utilization ratio-which accounts for roughly 30 percent of your credit score-inflates artificially and tanks your score. Lenders use your credit score to set interest rates, and even a 50-point drop means hundreds of dollars more per year on a mortgage or auto loan.

An inaccurate late payment that remains on your report for seven years creates a permanent liability that affects every credit application. If an account is incorrectly listed as open when it should be closed (or vice versa), it distorts your available credit and payment history. The FTC found that after corrections, 13 percent of consumers saw a score increase, and about 5.2 percent moved to more favorable risk brackets-proving that fixing errors directly improves your financial position.

Worse, if the error involves mixed files (another person’s data merged with yours), you could face denied credit, housing rejections, or even false collection attempts, all traceable back to a bureau’s negligence. Understanding these costs makes the next step clear: you need to know exactly what your credit reports say and how to challenge what’s wrong.

How to Get Your Credit Reports and Start Disputing

Pull Your Reports from All Three Bureaus

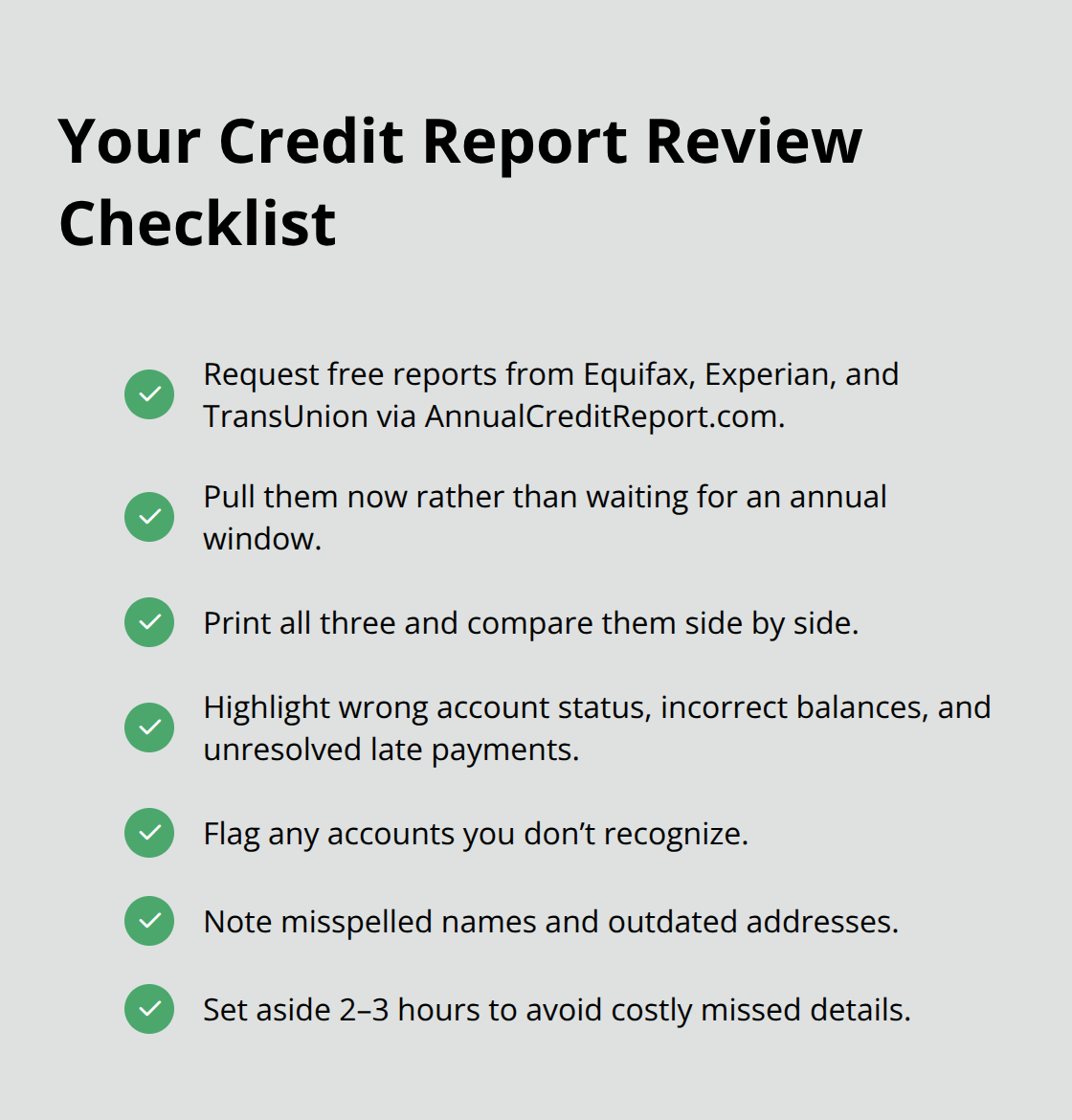

Visit AnnualCreditReport.com, the federally authorized source, and request your free credit reports from Equifax, Experian, and TransUnion. You receive one free report per bureau per year, though as of August 2023, all three bureaus offer free online reports more frequently-pull them now rather than waiting. Print all three reports and review them side by side, because errors in one bureau may not appear in the others. Mark every discrepancy with a highlighter: wrong account status, incorrect balances, late payments that should be resolved, accounts you don’t recognize, misspelled names, or outdated addresses. This task takes two to three hours but prevents you from missing details that could cost thousands in higher interest rates.

Build Your Dispute File

Once you identify an error, create a dispute file with printed reports, clear highlights, and separate folders for each bureau. Document everything you find, including the account number, the error description, and why it’s wrong. This organized approach keeps your evidence accessible and strengthens your case when you contact the bureaus or file complaints later.

File Disputes with Each Bureau

Write a precise dispute letter that identifies the exact account, describes the error, explains why it’s wrong, and requests correction or deletion under the Fair Credit Reporting Act. Include your identifying information, supporting documents, and a note that you are sending via certified mail with return receipt. Mail your dispute to Equifax, TransUnion, or Experian using certified mail so you trigger the bureau’s 30-day investigation clock. The bureau will contact the creditor or data furnisher to verify the information, and this is where most disputes fail: if the creditor simply stands by the claim, the bureau closes the dispute in their favor regardless of whether the information is actually correct.

Escalate When Disputes Fail

If the bureau responds with “verified” or fails to fix the issue after 30 days, escalate immediately by filing a complaint with the Consumer Financial Protection Bureau. The CFPB complaint process forwards your issue to the bureau and tries for a substantive response within roughly 15 days, adding formal federal oversight that forces real investigation rather than rubber-stamp verification. If a previously deleted item is re-inserted, the bureau must notify you in writing within five business days identifying who provided the data; failure to notify is a violation. Many Californians give up after one failed dispute, but you can resubmit with new evidence or file multiple CFPB complaints if the bureau continues to ignore clear errors.

Know Your Rights When Disputes Stall

The dispute process itself favors creditors and collectors over consumers. When you file a dispute, the bureau contacts the creditor to verify the information. If the creditor stands by the claim, the dispute is often resolved in their favor-regardless of whether the information is actually correct. Additionally, if a dispute is deemed frivolous due to incomplete information, the bureau may skip the investigation entirely, leaving you stuck with the error. Understanding this dynamic means you cannot rely on a single dispute attempt; you must follow up, escalate, and push back when the system fails you. The next section covers your legal rights and what creditors and bureaus must actually do when you challenge their claims.

What the Law Actually Requires From Bureaus and Creditors

The FCRA Gives You Concrete Rights

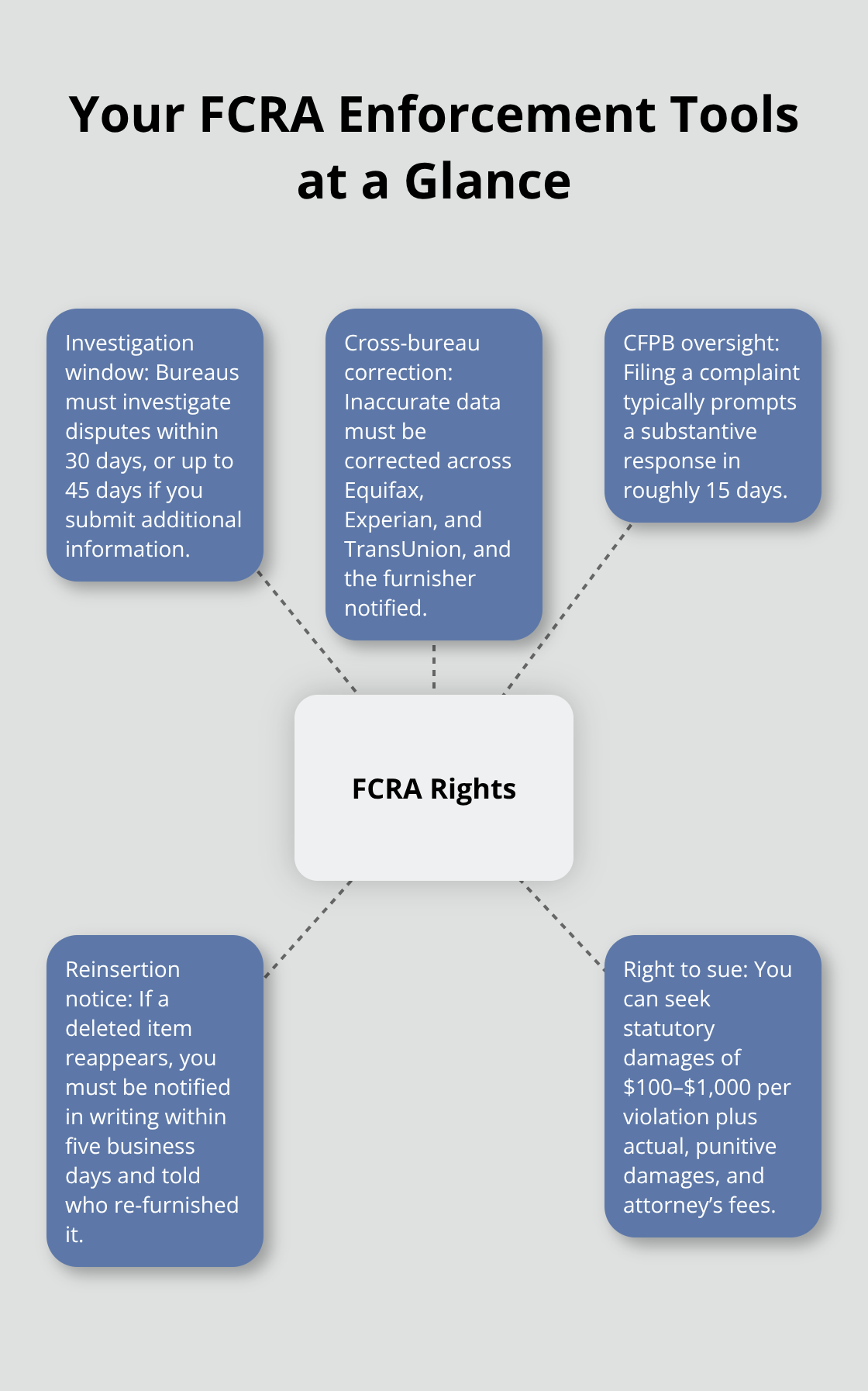

The Fair Credit Reporting Act gives you concrete rights that most Californians never use. The FCRA requires credit bureaus to report information with maximum possible accuracy, and when you dispute an error, the bureau must investigate within 30 days-or 45 days if you submit additional information during that window. The bureau must then respond to you in writing with the investigation results. If the information is found to be inaccurate, the bureau must correct it across all three reports and notify the furnisher (the creditor or debt collector who provided the data) to do the same.

A single corrected error should disappear from Equifax, Experian, and TransUnion simultaneously. If it does not, that is a violation.

Your Right to Sue for Damages

The FCRA allows you to sue a bureau or creditor for negligent or willful violations, with statutory damages ranging from $100 to $1,000 per violation, plus actual damages, punitive damages, and attorney’s fees. This means if a bureau ignores your dispute or a creditor repeatedly furnishes inaccurate data, you have leverage beyond complaint letters. When a bureau verifies an error as accurate without proper investigation, or when a creditor stands by false information, you can file a complaint with the Consumer Financial Protection Bureau, which has direct supervisory authority over these companies.

How the CFPB Forces Real Investigation

The CFPB forwards complaints to the bureau and requires substantive responses within roughly 15 days, forcing investigation rather than rubber-stamp closures. If a previously deleted item reappears on your report, the bureau must notify you in writing within five business days and identify who re-furnished the data. Failure to notify you constitutes a separate violation. This requirement prevents bureaus from quietly re-inserting errors without your knowledge.

What Creditors Must Do When You Challenge Them

Creditors must investigate disputes from you directly as well-not just from the bureau. Furnishers who repeatedly provide inaccurate data face CFPB enforcement actions and civil liability. When you send a dispute letter to a creditor, they cannot simply ignore it or stand by false information without conducting a real investigation. The law holds them accountable for the accuracy of what they report, and violations carry real consequences.

Your Leverage When the System Fails

Bureaus and creditors are not permitted to ignore clear errors, and when they do, you have the right to pursue damages. Understanding these legal requirements transforms your position from a powerless consumer to someone with enforceable rights backed by federal law.

Final Thoughts

Credit report errors CA are fixable, and federal law protects your right to challenge them. Pull your reports from all three bureaus, identify the errors, file disputes with documentation, and escalate to the Consumer Financial Protection Bureau if the bureaus fail to correct them within 30 days. You can resubmit disputes with new evidence, request statements explaining your disagreement, and pursue damages if bureaus or creditors violate the Fair Credit Reporting Act.

A single error can lower your score by 50 points or more, costing you hundreds of dollars annually in higher interest rates on mortgages, auto loans, and credit cards. The cost of action is minimal-your time and certified mail postage-while the cost of inaction is substantial. After you fix errors, monitor your reports regularly using AnnualCreditReport.com to catch new mistakes early.

If disputes are ignored, bureaus refuse to investigate properly, or creditors stand by false information despite your evidence, you have the right to pursue legal action and recover damages. We at Bontrager Law represent Californians in credit reporting disputes and have recovered millions for clients facing inaccurate data and unlawful practices. Contact us for a free case review if you have hit a wall with the bureaus or believe a creditor has violated your rights.