Identity theft can destroy your credit score in weeks. Fraudsters open accounts, max out cards, and leave you with the damage.

When this happens, you need a credit identity theft lawyer who understands both the legal and financial sides of recovery. At Bontrager Law, we help victims reclaim their credit and hold thieves accountable.

How Identity Theft Damages Your Credit Immediately

Identity theft hits your credit score faster than most victims realize. According to the Bureau of Justice Statistics, about 23.9 million U.S. residents experienced identity theft in 2021 alone, with credit card misuse affecting roughly 4% of the population. When a thief opens accounts in your name, those fraudulent accounts appear on your credit report within days. Each new account inquiry tanks your score, and maxed-out balances destroy your credit utilization ratio. You might not notice the damage until you apply for a mortgage, car loan, or even a job that requires a credit check. The Federal Trade Commission reported over 1.1 million identity theft cases in 2023, showing this problem only accelerates. In Q1 2025, credit card identity theft alone surged 49% from the prior year, with new account fraud climbing from 91,421 cases to 139,569 cases.

How Thieves Access Your Information

Fraudsters target you through phishing emails, data breaches at retailers, skimming devices at ATMs and gas pumps, insecure public Wi-Fi networks, and mail theft. They don’t need much-just your name, Social Security number, and date of birth to wreak havoc. Once they have this information, they act quickly to open accounts and extract value before you catch on.

Red Flags That Signal Fraud

Red flags appear immediately: unexpected charges on accounts you never opened, bills for services you never requested, sudden credit score drops of 50+ points, credit applications denied with no clear reason, IRS notices about unfiled tax returns, and collection calls on accounts you don’t recognize. Most victims spend at least one day resolving the financial damage, though serious cases consume weeks or months.

The average direct financial loss per victim totals $880 according to the Bureau of Justice Statistics, but victims of new account fraud face far steeper bills-averaging $3,430 per incident compared to $620 for credit card misuse.

Pull Your Credit Reports Today

Your first move is pulling your credit reports from all three bureaus-Equifax, Experian, and TransUnion. You’re entitled to one free report annually from each bureau through AnnualCreditReport.com. Don’t waste time; pull them today. Scrutinize every account listed, every inquiry, every balance. If you spot unauthorized accounts you never opened or inquiries you never authorized, that’s concrete evidence of theft. Write down dates, account numbers, and the names of fraudulent creditors. This documentation becomes critical if you pursue legal action later.

Dispute Errors on Your Credit Report

About 59% of identity theft victims experienced financial losses of $1 or more, with total losses across all incidents reaching $16.4 billion in 2021 alone. When you find errors on your credit report, dispute them promptly with both the credit bureau and the reporting company directly. Include as much detail and supporting documentation as possible. Send disputes via certified mail so you have proof of delivery. The Fair Credit Reporting Act gives you the right to challenge inaccurate information, and bureaus must investigate within 30 days. Don’t wait for the investigation to complete before taking further action-your next step involves contacting your financial institutions and filing reports with federal agencies to stop the bleeding and establish a legal record of the fraud.

What to Do Immediately After Discovering Identity Theft

Speed determines whether you stop the thief or let them drain your accounts. The moment you spot unauthorized accounts or fraudulent charges, contact the Federal Trade Commission at identitytheft.gov and file an Identity Theft Report. This single step creates an official record that speeds up fraud blocking with lenders and creditors. The FTC report also gives you ammunition when disputing fraudulent accounts because it documents the theft happened and when. While filing, gather specific details: the fraudulent account numbers, the dates you discovered the fraud, and the names of creditors who opened fake accounts. This information matters because creditors are more likely to remove fraudulent accounts when you present concrete evidence of identity theft rather than vague complaints.

Contact Your Banks and Credit Card Companies Within Hours

Next, call your banks and credit card companies directly using the phone numbers on your statements or cards. Don’t use numbers from a Google search because scammers sometimes hijack search results. Tell each institution about the fraudulent accounts and ask them to freeze your existing accounts pending investigation. Many banks issue new cards within 24 to 48 hours and reverse unauthorized charges. According to the Bureau of Justice Statistics, about 67% of identity theft victims contacted their credit card company or bank about the incident, and most recovered at least some losses this way.

Request written confirmation of every conversation and the names of representatives you spoke with.

Place Fraud Alerts With All Three Credit Bureaus

Place fraud alerts with Equifax at 800-525-6285, Experian at 888-397-3742, and TransUnion at 800-680-7289. A fraud alert instructs lenders to contact you by phone before approving new credit in your name, which blocks most new account fraud cold. This step is not optional. Fraud alerts last one year and cost nothing. When you call, explain that you are an identity theft victim and request an alert on your file. The bureaus will also send you free credit reports so you can verify the damage. After placing alerts, contact the Social Security Administration fraud line at 800-269-0271 to report the theft and prevent criminals from opening new accounts using your Social Security number (this prevents fraudsters from exploiting your SSN for employment or government benefits). Document every call with dates, times, and the names of representatives. These records become critical evidence if you later pursue legal action against negligent data holders or creditors who failed to catch the fraud.

File a Police Report in Your Jurisdiction

File a police report immediately in the jurisdiction where the theft occurred. This step proves diligence to creditors and law enforcement and creates an official record that strengthens your position when disputing accounts. Only 7% of identity theft victims reported incidents to law enforcement, yet doing so significantly improves your chances of holding responsible parties accountable. Provide the police with copies of your FTC Identity Theft Report and documentation of fraudulent accounts. Request a copy of the police report for your records-you’ll need it when working with creditors and potentially with legal counsel to recover losses and restore your credit standing.

When a Credit Identity Theft Lawyer Becomes Your Best Defense

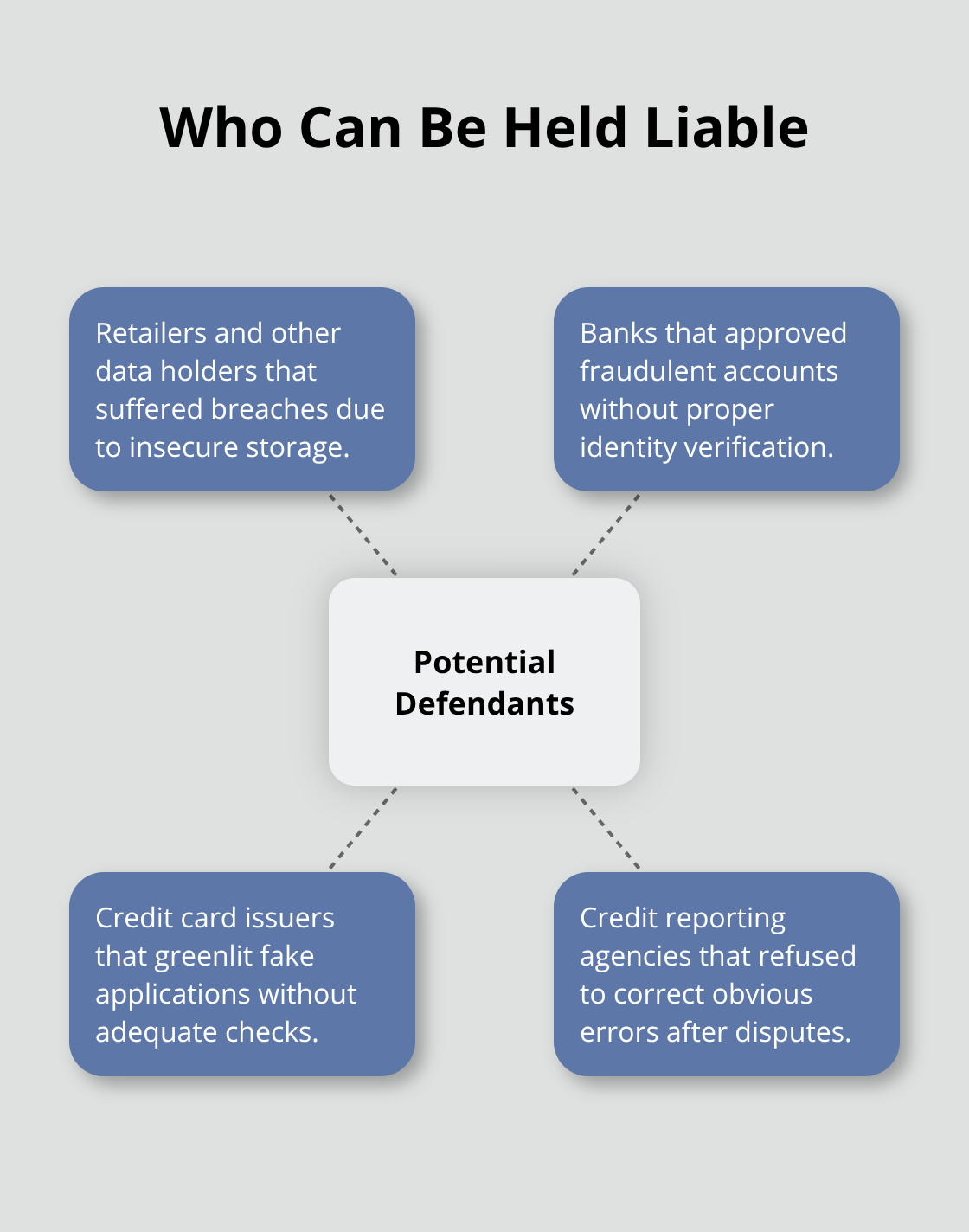

At this point, you’ve filed reports, contacted your banks, and placed fraud alerts. But stopping the thief is only half the battle. The real fight is recovering your money and restoring your credit while holding the companies responsible for the breach accountable. This is where a credit identity theft lawyer enters the picture-not to handle paperwork you could do yourself, but to pursue financial recovery from the actual wrongdoers. Many victims assume they’re stuck eating the losses themselves, but that’s simply false. Under federal laws like the Fair Credit Reporting Act and the Identity Theft and Assumption Deterrence Act, you have the right to hold negligent parties liable, including data breaches at retailers, banks that failed to catch fraudulent accounts, credit card issuers that approved fake applications without verification, and credit reporting agencies that refused to correct obvious errors on your report.

Why Financial Recovery Requires Legal Action

The financial stakes justify legal action immediately. Victims of new account fraud face average losses of $3,430 per incident according to the Bureau of Justice Statistics, and in Q1 2025, new account credit card fraud alone climbed 49% year-over-year with 139,569 reported cases. A lawyer investigates who actually failed in their duty to protect your data or catch the fraud. Did a retailer store your information insecurely? Did a bank approve a credit card application without proper identity verification? Did a credit bureau refuse to remove fraudulent accounts after you disputed them? These failures create legal liability.

How Your Attorney Builds Your Case

Your attorney gathers evidence, files claims against the responsible parties, and pursues damages for out-of-pocket losses, emotional distress, and time spent resolving the theft. The legal process typically involves sending demand letters to negligent parties, negotiating settlements, and if necessary, filing suit in court. Most cases settle without trial because companies would rather pay damages than face public litigation. Throughout the process, your lawyer handles all communication with creditors, credit bureaus, and defendants so you can focus on rebuilding your life instead of fighting bureaucracy.

What Damages You Can Recover

Federal consumer protection laws allow you to recover multiple categories of damages. Out-of-pocket costs include fraudulent charges, overdraft fees, and money spent resolving the theft. Emotional distress damages compensate you for the stress and anxiety identity theft causes (about 10% of victims experience severe distress according to the Bureau of Justice Statistics). You can also recover for time lost-hours spent on phone calls, document gathering, and credit repair work. Some cases include lost wages if the theft forced you to take time off work. State and federal law determine which damages apply to your specific situation, which is why legal counsel matters.

Acting Quickly Protects Your Rights

The key is acting quickly because evidence degrades over time and statutes of limitations apply to these claims. The sooner you contact a lawyer, the sooner they can preserve evidence, send preservation letters to companies, and begin negotiations with responsible parties. Delays allow companies to destroy records and make your case harder to prove.

Final Thoughts

Rebuilding your credit after identity theft takes time, but you can restore your financial standing with the right approach. Monitor your credit reports monthly through AnnualCreditReport.com to catch new fraudulent activity before it spreads, pay all bills on time, keep credit card balances low, and avoid opening new accounts unless absolutely necessary. Your credit score will gradually recover as fraudulent accounts age and fall off your report, typically within seven years.

Long-term prevention means treating your personal information like cash. Shred sensitive documents before throwing them away, lock important papers in a safe place, and never carry your Social Security number in your wallet (use your work phone number on checks instead, and print only the last four digits of your account number on the memo line). Use secure websites marked with https when shopping online, monitor your bank and credit card statements weekly, and consider placing a credit freeze on your file if you’re not actively seeking new credit.

A credit identity theft lawyer can accelerate your recovery by pursuing financial damages from the companies that failed to protect your data or catch the fraud. Contact Bontrager Law to discuss your case and learn how we can help restore your financial standing with a free case review and no upfront fees.