A credit report error can tank your score and cost you thousands in higher interest rates. At Bontrager Law, we’ve seen how inaccurate information, fraudulent accounts, and outdated negative entries wreak havoc on California residents’ finances.

The Fair Credit Reporting Act gives you real power to fight back. This guide walks you through FCRA reporting corrections in California-from spotting errors to taking legal action if needed.

How Credit Reporting Errors Start

Credit reporting errors in California stem from three primary sources, and understanding where mistakes originate helps you catch them faster. Data entry mistakes happen constantly at the furnishing stage-banks, credit card companies, and lenders input thousands of transactions daily, and typos slip through. A wrong account number, transposed Social Security digits, or a name variation gets recorded and transmitted to Equifax, Experian, and TransUnion. California’s massive credit market makes this problem acute: roughly 25 million residents carry credit cards, about seven million mortgages exist in the state, and nearly four million Californians repay student debt. With that volume, even a 0.1% error rate means tens of thousands of Californians see inaccurate information on their reports. A single misreported account can drop your score 50 to 100 points, directly raising your mortgage rate or killing a loan application entirely.

When Identity Theft Corrupts Your Report

Fraudulent accounts represent a different threat-someone uses your identity to open accounts in your name, and those accounts appear on your credit report with negative payment histories or high balances. Identity theft victims often discover the problem when they check their credit report, sometimes months after the fraud began. Criminals target California residents deliberately because the state’s high-value mortgages and credit card market make fraud profitable. Once a fraudulent account lands on your report, it damages your credit immediately and requires you to prove it isn’t yours-a burden that shouldn’t fall on you. The process to remove fraudulent accounts takes time because furnishers and bureaus must investigate, and during that investigation window, the false information remains visible to lenders.

Outdated Information That Should Disappear

Negative information that should have aged off your report still appears because the credit bureaus fail to remove entries when the legal reporting window closes. Most negative items fall off after seven years; bankruptcies after ten years. California law under the Fair Credit Reporting Act requires bureaus to stop reporting information outside these windows, but documented cases show bureaus continue reporting outdated entries. An old collection account, a paid-off charged-off card, or a settled judgment that’s past its reporting deadline should vanish from your report, yet many California residents see these entries linger for years past the deadline. This happens because the removal process isn’t automatic-the bureaus don’t proactively delete; they wait for disputes or legal action to force removal. That’s why you should review your report annually for outdated negative entries, and why you should contact the bureaus directly about items past their reporting date. Direct contact often succeeds faster than waiting for the entries to disappear on their own.

Why You Need to Act Now

The longer inaccurate information remains on your report, the more damage it inflicts on your financial life. Lenders see the errors and make decisions based on false data. Your credit score reflects mistakes that aren’t yours, and you lose opportunities for better rates and terms. The good news is that you have legal rights under the FCRA, and the process to correct errors is straightforward once you understand the steps. The next section walks you through your rights and shows you exactly what power the law gives you to fight back against reporting errors.

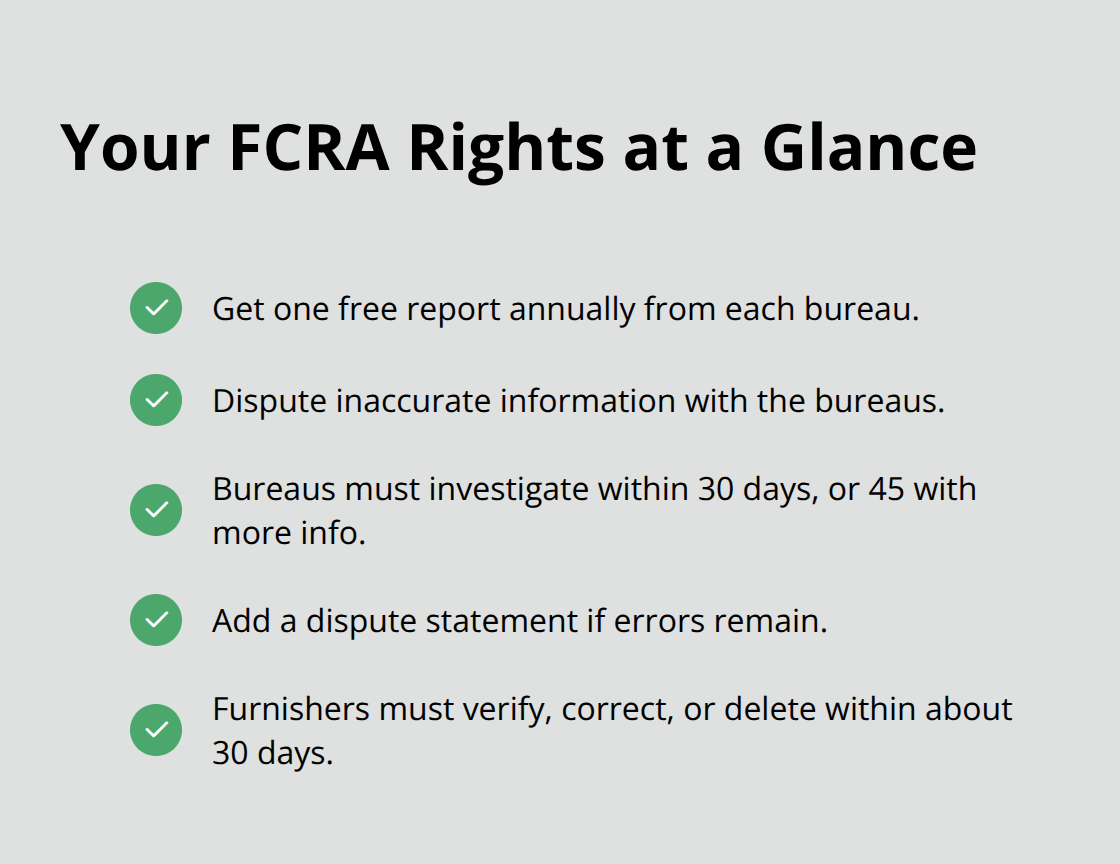

Your FCRA Rights in California

The Fair Credit Reporting Act grants California residents four concrete rights that furnishers and credit bureaus must respect. First, you access your credit report for free once per year from each of the three major bureaus through AnnualCreditReport.com. Many Californians pull all three reports at once rather than spacing them out, which gives you a complete snapshot of what lenders see about you. Second, you dispute any information you believe is inaccurate, and the bureau must investigate your dispute within 30 days, or 45 days if you submit additional information during that window. Third, you add a dispute statement to your file if the bureau investigates but doesn’t remove the error, which means lenders will see your side of the story when they pull your report. Fourth, when a furnisher receives your dispute, they must investigate and respond within approximately 30 days; if they cannot verify the information, they must tell the bureaus to delete or correct it. These aren’t suggestions or best practices-they’re legal obligations backed by federal law.

The Right to Sue for Violations

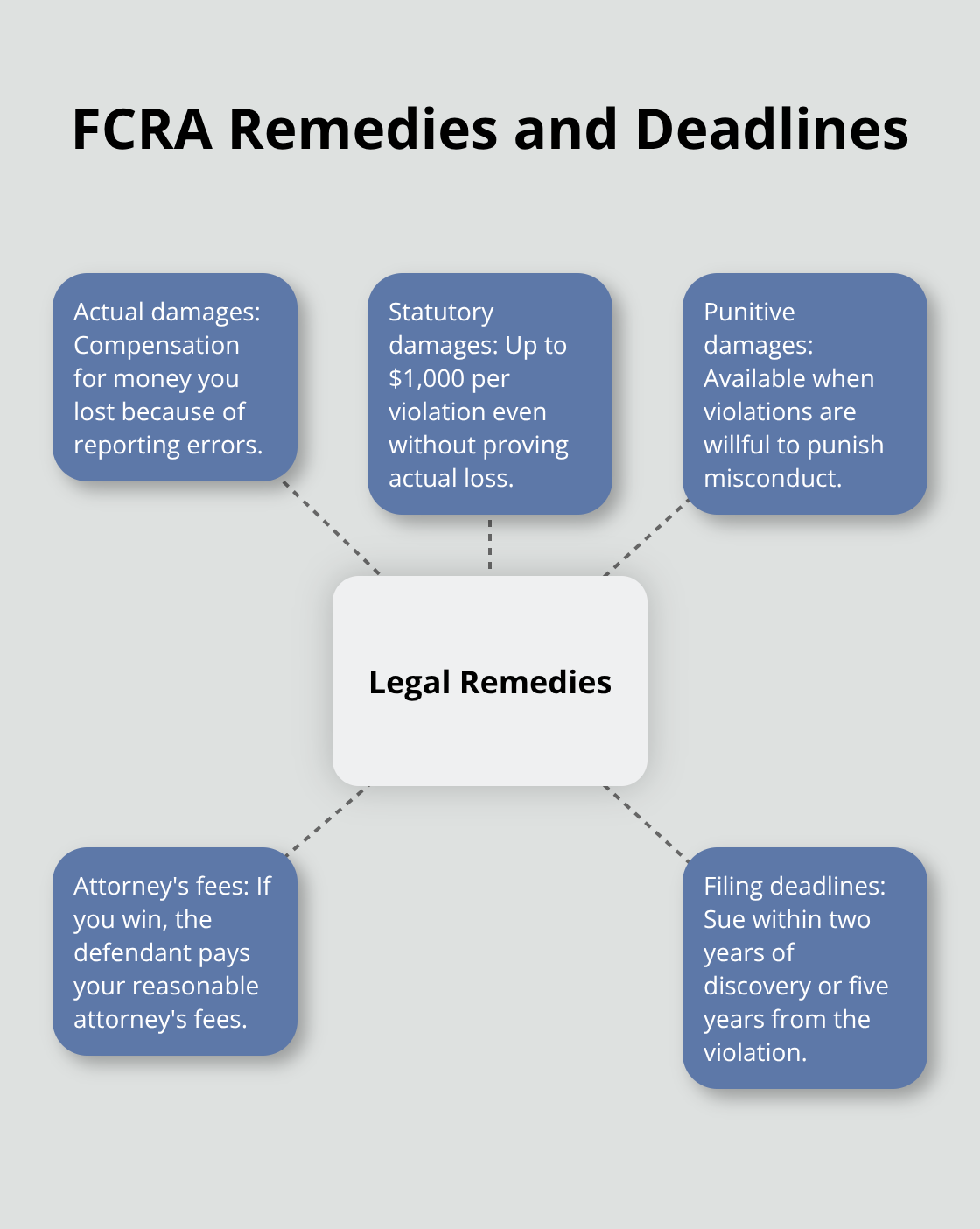

The FCRA gives you the right to sue for violations. If a bureau or furnisher fails to investigate your dispute properly, continues reporting information they know is wrong, or reports information outside the legal seven-year window, you file a lawsuit and recover actual damages (money you lost), statutory damages up to 1,000 dollars per violation, punitive damages if the violation was willful, and attorney’s fees. California courts have jurisdiction over FCRA cases, and you have two years from discovery of the violation or five years from the violation itself to file. This means if a bureau continues reporting a fraudulent account years after you filed a dispute, or if they ignore your dispute letter entirely, you have legal recourse.

Why Attorney’s Fees Matter

Many California residents don’t pursue legal action because they think the process is expensive, but the FCRA’s attorney’s fee provision changes that calculation. The defendant pays your legal costs if you win, which makes pursuing violations financially feasible. If a bureau or furnisher ignores your rights under the FCRA, contacting a consumer protection attorney who handles credit reporting cases makes sense before your filing deadline passes. Bontrager Law represents California residents in FCRA disputes and has recovered millions for clients over nearly 20 years of handling thousands of claims. A free case review helps you understand whether your situation qualifies for legal action and what damages you might recover.

How to Fix Credit Report Errors

Pull Your Reports and Review Them Thoroughly

Start at AnnualCreditReport.com and request your credit reports from all three bureaus-Equifax, Experian, and TransUnion. You receive one free copy annually from each bureau. Many California residents pull all three reports at once rather than spreading them out over the year, which gives you a complete picture of what lenders see. Print them or save them as PDFs and read through every section carefully. Look for personal information errors first: wrong name, phone number, address, or Social Security number. Then examine each account listed to confirm it belongs to you. Identity theft sometimes creates mixed files where information from another person gets combined with yours, so verify that every account is actually yours.

Spot the Most Common Errors

Check the account status, payment history, current balance, and credit limit for accuracy on each account. Watch for accounts you closed that still show as open, authorized user accounts listed as accounts you own, duplicate debts reported under different names, and payment histories with incorrect delinquency dates. The CFPB notes that common errors include accounts that don’t belong to you, inaccurate personal information, and wrong payment histories. Document every error you find by circling or highlighting it on your printed report and creating a separate list with the account name, account number, and specific description of what’s wrong.

File Disputes with Both the Bureau and the Furnisher

Contact both the credit bureau that issued the report and the furnisher that provided the incorrect information. File your dispute with the credit bureau online, by phone, or by mail, but send disputes by certified mail with return receipt requested to create proof the bureau received it. Include your contact information, the account number of each disputed item, a clear explanation of why each item is wrong, and copies of supporting documents like statements, payment receipts, or court documents. Never send original documents. The bureau must investigate within 30 days (or 45 days if you provide additional information) and must share your dispute with the furnisher. Simultaneously, mail a dispute letter directly to the furnisher using their dispute address from your credit report.

Track Your Progress and Follow Up

Keep copies of everything you send and maintain a log of all communications with dates and responses. After 30 days, follow up with the bureau to confirm your dispute was investigated and check whether corrections have been made. If the bureau investigated but didn’t remove the error, you can request that a concise dispute statement be added to your file so future lenders see your side of the story. If the furnisher corrected the information, the bureaus must update your reports within 30 days. If nothing changes and the error persists, contact a consumer protection attorney to discuss whether the bureau or furnisher violated your FCRA rights. We at Bontrager Law review cases where disputes were ignored or mishandled, and many violations qualify for legal action with attorney’s fees paid by the defendant.

Final Thoughts on FCRA Reporting Corrections California

If your dispute stalls or the furnisher ignores your request, file a complaint with the Consumer Financial Protection Bureau to escalate the issue. The CFPB accepts complaints online, by phone at 855-411-2372, or by mail, and they forward your complaint to the company with a tracking number so you can monitor progress. Companies take federal agency involvement seriously, and many California residents see results after filing a CFPB complaint because the agency has authority over credit reporting violations.

When disputes fail or violations persist, contact a consumer protection attorney to review your dispute letters, the bureau’s response, and your supporting documents. If the bureau failed to investigate, continued reporting information they couldn’t verify, or ignored your dispute entirely, you likely have a case under the FCRA. The law allows you to recover actual damages, statutory damages up to 1,000 dollars per violation, punitive damages for willful violations, and attorney’s fees paid by the defendant.

The correction process typically takes 30 to 90 days from start to resolution if the bureau and furnisher cooperate, though legal action can take longer but often produces faster results than waiting for voluntary compliance. We at Bontrager Law represent California residents in FCRA reporting corrections and have recovered millions for clients over nearly 20 years. A free case review shows you whether your situation qualifies for legal action and what you might recover.