Your credit report directly impacts your ability to rent in Los Angeles. Errors on that report-whether inaccurate payment histories or fraudulent accounts-can block you from getting approved for housing.

At Bontrager Law, we’ve seen renters credit reporting LA issues destroy otherwise qualified applications. The good news is you have legal tools to fight back and protect yourself.

How Credit Reporting Errors Damage Your LA Rental Prospects

Late payments that you actually made on time, accounts you never opened, or collection notices tied to someone else’s debt-these aren’t rare mistakes. They’re widespread problems that directly tank rental applications in Los Angeles. The three major credit bureaus-Equifax, Experian, and TransUnion-each maintain separate reports on you, and errors can appear on one, two, or all three. When a landlord pulls your credit during the rental application process, they see whatever inaccurate information sits in those files. A single wrong late payment can drop your credit score by 100 points or more, making landlords view you as high-risk even if you’ve never missed rent in your life. Qualified renters get rejected based on false information, then spend months trying to fix records that should never have been wrong in the first place. The damage compounds because that incorrect information stays on your report for up to seven years, poisoning every housing application you submit during that time.

When Your Payment History Gets Reported Incorrectly

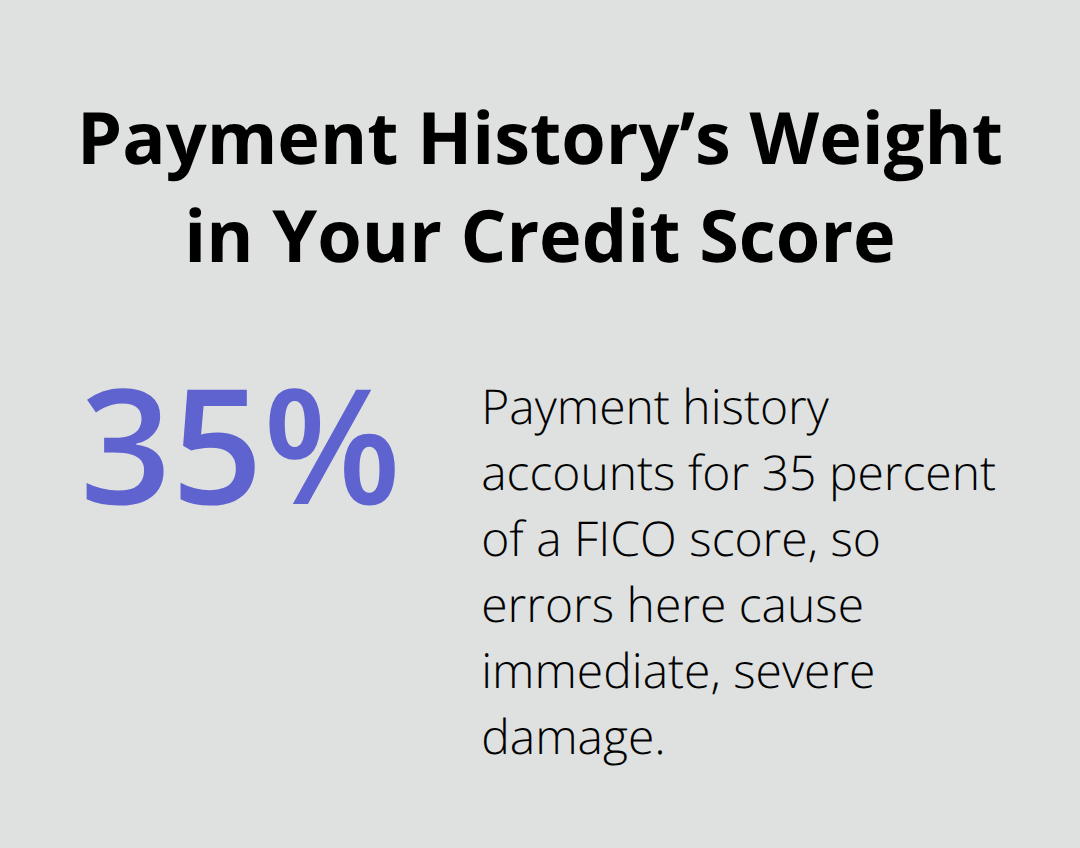

Payment history accounts for 35 percent of your credit score, so inaccurate records here cause immediate, severe damage. A landlord or utility company might report a payment as late when it arrived on time, or they might report a payment you made twice. These errors happen because of data entry mistakes, system glitches, or poor record-keeping at the creditor’s end.

The problem worsens when you’re dealing with rent reporting services. As of April 1, 2025, California landlords subject to Assembly Bill 2747 must offer to report your on-time rent payments to credit bureaus. Services like Esusu, RentLinx, and CredHub now send rental payment data to Equifax, Experian, and TransUnion. While positive reporting helps many renters, it also means late or missed payments now appear on your credit reports-something that never happened before. If a reporting service records a payment as late when you paid on time, or fails to remove a payment after you’ve settled a dispute with your landlord, your score suffers immediately.

Identity Theft and Unauthorized Accounts

Fraudulent accounts opened in your name are far more destructive than late payment errors because they signal to landlords that you’re either irresponsible or a victim of crime-neither of which makes you look like a trustworthy tenant. An identity thief opens a credit card, takes out a loan, or signs up for utilities in your name, then stops paying. The collections account appears on your report, damaging your score and signaling default to any landlord reviewing your application. You won’t know this happened until you check your reports, which is why pulling your credit regularly matters. You can access one free copy of each bureau’s report every 12 months through AnnualCreditReport.com, or starting in 2026, you can check each report weekly at no cost. Equifax also offers six free reports per year through 2026. If you spot accounts you didn’t open, file a report immediately at IdentityTheft.gov to receive a personalized recovery plan. The sooner you act, the faster you can dispute these fraudulent accounts and prevent them from sabotaging your rental applications.

How Errors Block Your Housing Applications

Landlords in Los Angeles pull credit reports as a standard part of tenant screening, and they make decisions based on what those reports show. An inaccurate late payment or a fraudulent collection account can result in an outright rejection, even if your actual payment record is spotless. Some landlords set minimum credit score thresholds (often 620 or higher), and a single reporting error can push you below that cutoff. Others review your report manually and flag any negative items as red flags. Either way, the error controls the outcome of your application. You lose the apartment, and you move on to the next property-only to face the same rejection because the error still sits on all three of your credit reports. This cycle repeats until you fix the underlying problem. The longer you wait to dispute errors, the more rental opportunities you lose and the more damage compounds to your housing prospects.

Taking the First Step: Know What’s on Your Reports

You cannot fight errors you don’t know exist. Pull your credit reports from all three bureaus before you apply for housing in Los Angeles. Compare what each bureau reports about you, because they often contain different information. Look for accounts you didn’t open, payment dates that don’t match your records, and collection notices that don’t belong to you. Write down every discrepancy you find. This list becomes your roadmap for the disputes you’ll file next. The faster you identify errors, the faster you can move to correct them and improve your chances of rental approval.

Steps to Dispute Credit Reporting Errors

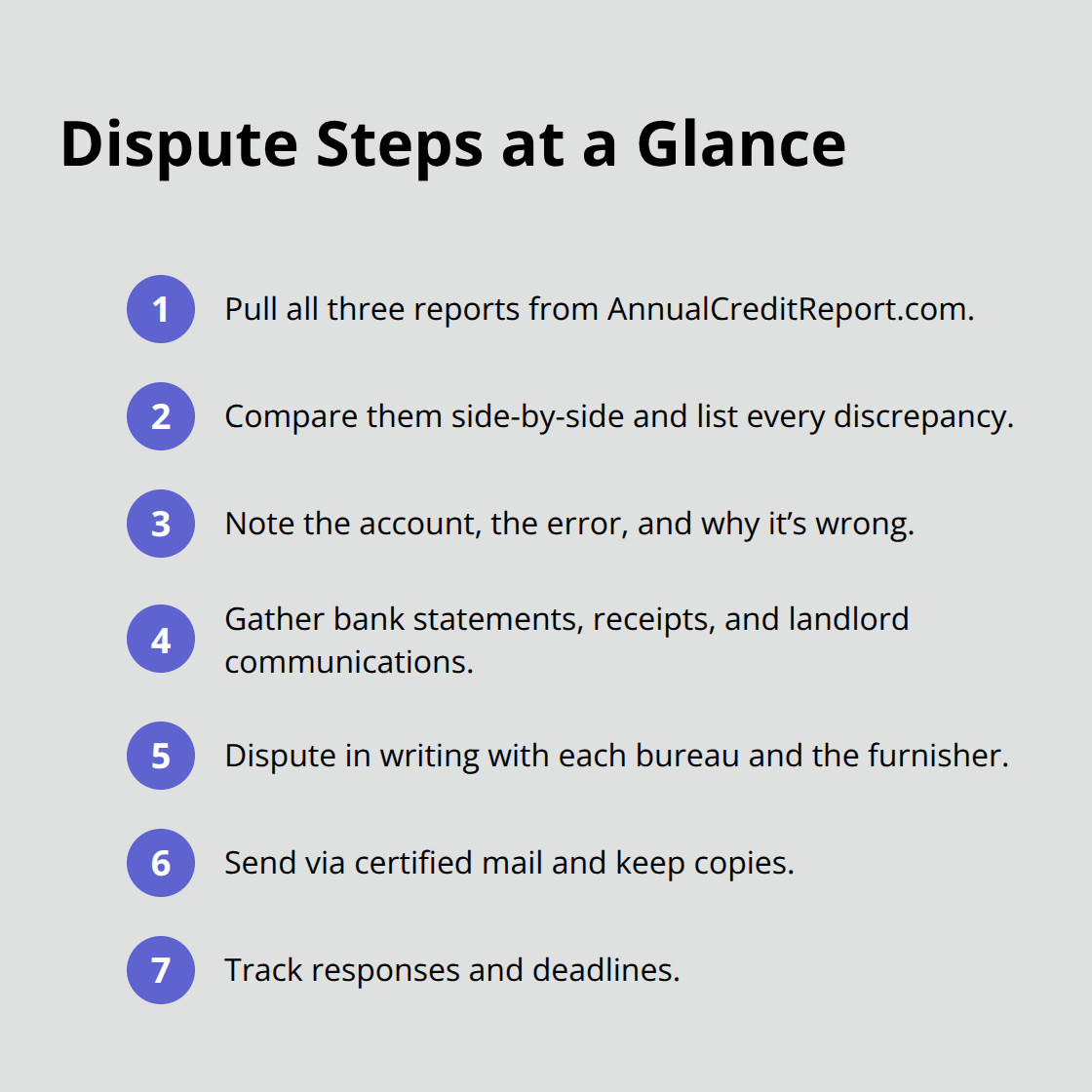

Obtain your credit reports from all three bureaus through AnnualCreditReport.com, the only authorized free source. Once you have them, compare the three reports side-by-side because Equifax, Experian, and TransUnion often contain different information about you. Circle every discrepancy: accounts you didn’t open, payment dates that don’t match your records, collection notices that aren’t yours, or late payments you know you made on time. Write down the specific account name, the reporting error, and why it’s wrong. This documentation becomes your dispute evidence. Investigate each item independently and verify against your own payment records, bank statements, or landlord communications. The faster you identify errors, the faster you can move to correction-which matters because every month that inaccurate information sits on your report damages your rental prospects in Los Angeles.

Contact Each Bureau Separately

Each bureau maintains its own investigation process, so you must contact all three. Experian handles disputes at 888-397-3742, TransUnion at 800-916-8800, and Equifax at 866-349-5191. You can dispute by phone, but written disputes create a paper trail that protects you if a bureau claims you never reported the error. Write a letter to each bureau that includes your full name and address, the specific account or item you’re disputing, and a clear explanation of why it’s wrong. Attach copies (never originals) of supporting documents like bank statements, payment confirmations, or landlord correspondence. Send each letter via certified mail with return receipt so you have proof of delivery. The bureau must investigate within 30 days and notify you in writing of the results.

What Happens After You File

If the bureau finds the information inaccurate, it must inform all three credit reporting agencies to correct it, and you’ll receive a free updated report. If the investigation doesn’t resolve your dispute, you can add a statement disputing the item to your file, which appears on future reports. This notation signals to landlords that you’ve challenged the accuracy of the information, which can help your rental application even while the dispute remains pending.

Dispute the Original Reporter Directly

You don’t have to wait for the bureau to investigate-dispute the error directly with the business that reported it. If a landlord reported a late payment you made on time, or if a rent-reporting service like Esusu or RentLinx recorded incorrect payment data, send a written dispute to that company as well. Use the same format: your name and address, the specific error, why it’s wrong, and supporting documentation. Send via certified mail and keep copies of everything. Many businesses ignore these disputes, which is why documentation matters. If a business keeps reporting information you’ve disputed, the bureau must note that you are disputing it on your report.

Monitor Your Reports for Corrections

After corrections are made, monitor your credit reports to confirm the error was removed and that dispute notices appear in future reports. Verify that all three bureaus reflect the corrected information. If errors persist after your dispute, you may have grounds to take further action-which brings us to the legal protections that California law provides to renters facing credit reporting violations.

What California and Federal Law Actually Protect You

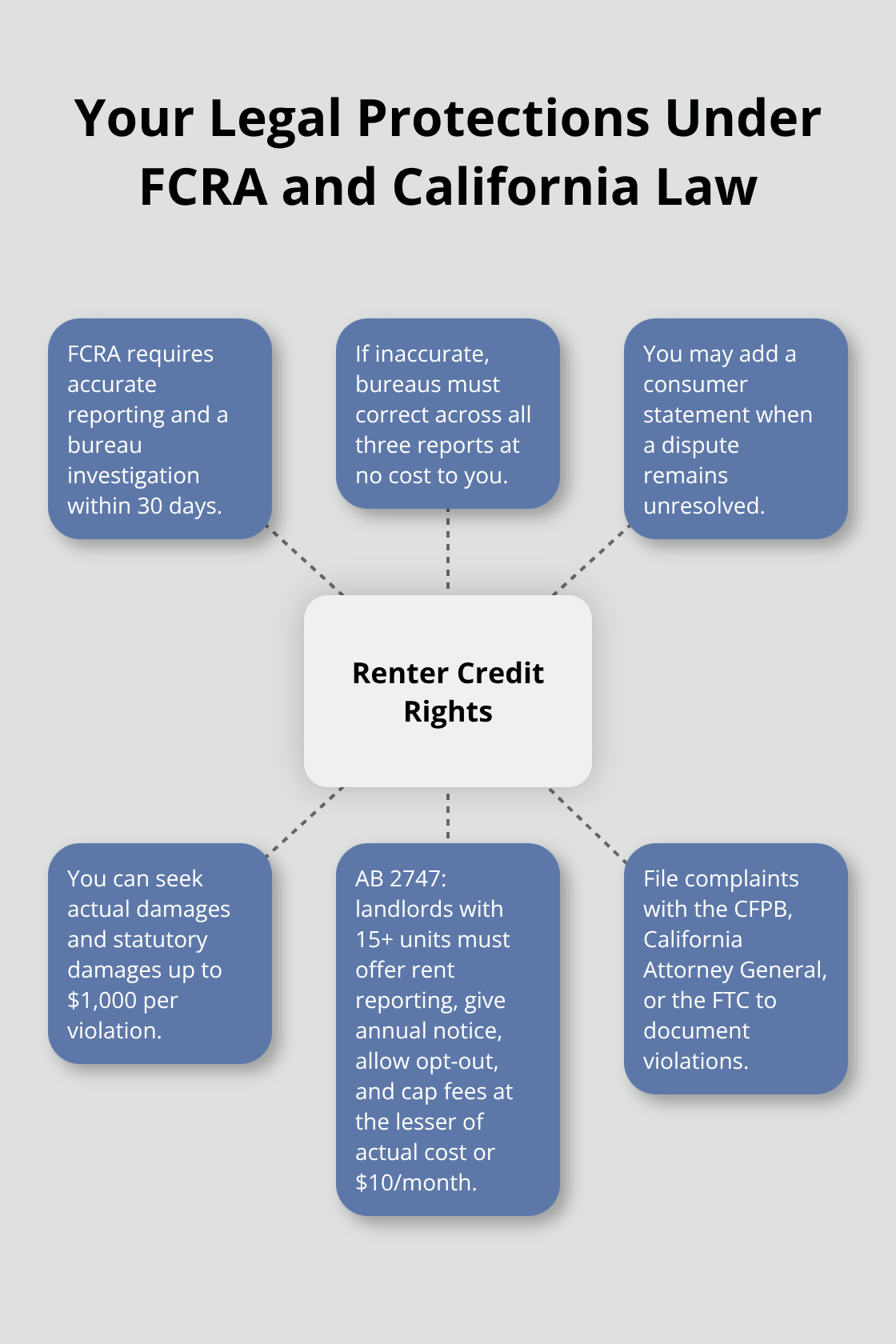

Federal law grants you specific rights when credit bureaus and creditors report information about you. The Fair Credit Reporting Act (FCRA) requires that any information on your credit report remain accurate, and it mandates that credit bureaus investigate disputes within 30 days. If a bureau finds information inaccurate after investigating your dispute, it must correct the error across all three bureaus at no cost to you. The FCRA also allows you to add a statement to your file if a dispute remains unresolved, and that statement appears on all future reports you request. Most importantly, if a credit bureau or creditor violates FCRA requirements, you can sue for actual damages (like lost housing opportunities or emotional distress) plus statutory damages up to $1,000 per violation, even if you cannot prove specific financial harm.

California’s Consumer Protection Laws

California goes further than federal law. The state’s Consumer Legal Remedies Act prohibits unfair and deceptive practices in consumer transactions, which includes credit reporting. Assembly Bill 2747, effective April 1, 2025, requires landlords with more than 15 rental units to offer tenants the option to have on-time rent payments reported to credit bureaus. This law recognizes that rent reporting helps renters build credit, but it also protects you by requiring landlords to notify you annually of the reporting option and your right to opt out. If a rent-reporting service or landlord violates these requirements, you have grounds to file a complaint with the California Attorney General. The law also caps fees for rent reporting at the lesser of actual cost or $10 per month, preventing landlords from charging excessive amounts for the service.

Filing Complaints and Building Your Case

If you discover that a creditor, collector, or credit reporting company has violated your rights, file a complaint immediately with the Consumer Financial Protection Bureau at its website, which maintains a public database of complaints and tracks how companies respond. You can also file complaints with the California Attorney General or the Federal Trade Commission at ReportFraud.ftc.gov. Document everything: keep copies of your dispute letters, proof of delivery via certified mail, written responses from bureaus and creditors, and records of how the error affected your housing applications. If a business ignores your dispute or continues reporting inaccurate information after you have challenged it, that violation strengthens any legal claim you might pursue.

When to Seek Legal Help

Credit reporting violations can result in significant damages, and you should not navigate this process alone if a business refuses to correct errors or continues violating your rights. Bontrager Law represents renters across California who face credit reporting violations, and the firm handles these cases on a contingency basis, meaning you pay nothing unless damages are recovered. A free case review with the team can clarify whether you have a viable claim and what compensation you might be entitled to pursue.

Final Thoughts

Credit reporting errors destroy rental applications in Los Angeles. A single inaccurate late payment, a fraudulent account, or a data entry mistake can block your housing approval and keep you locked out of apartments for years. The false information stays on your report for up to seven years, poisoning every rental application you submit during that time.

You have concrete tools to fight back. Pull your credit reports from all three bureaus through AnnualCreditReport.com and compare them side-by-side. Write down every discrepancy you find, then dispute each error in writing with the bureau that reported it and with the original business that supplied the information. Send everything via certified mail and keep copies-the bureau must investigate within 30 days, and if the error is confirmed inaccurate, it gets removed from all three reports at no cost to you.

This process works, but it takes time and persistence. Many renters succeed in correcting errors on their own and improve their credit scores before their next rental application. If a credit bureau or creditor refuses to correct errors or violates your rights under federal or California law, Bontrager Law represents renters across California who face renters credit reporting LA violations, handling cases on a contingency basis so you pay nothing unless damages are recovered.