Debt collectors calling at all hours, credit reports filled with errors you didn’t make, identity theft draining your accounts-these problems feel overwhelming and expensive to fix.

At Bontrager Law, we know that an affordable consumer protection attorney shouldn’t be a luxury. You deserve legal help that actually protects your rights without crushing your wallet.

What Happens When You Fight Back Against Debt Collectors and Credit Errors

Debt collectors operate on volume. They send thousands of calls and letters hoping most people won’t respond. The Fair Debt Collection Practices Act prohibits harassment, threats, calls before 8 a.m. or after 9 p.m., and contact at your workplace if your employer objects. Yet the Consumer Financial Protection Bureau received over 200,000 complaints about debt collection in 2024 alone. Many violations go unchallenged simply because people don’t know they can fight back.

When Legal Representation Changes the Game

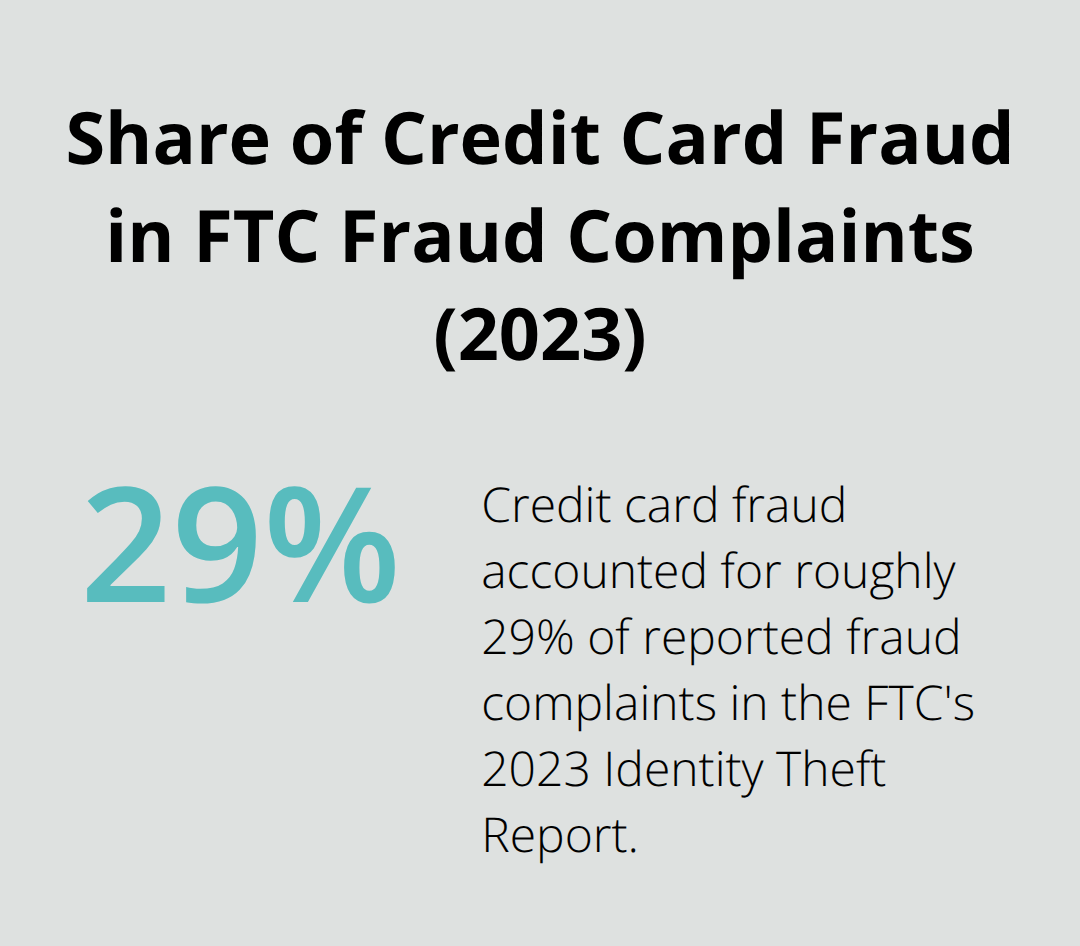

When you push back with legal representation, collectors often back down. Some cases result in payment to you for violations, not just dismissal of the debt. Identity theft and credit reporting errors follow similar patterns. Equifax, Experian, and TransUnion process billions of records annually, and errors are common. The Federal Trade Commission’s 2023 Identity Theft Report documented nearly 2.6 million fraud complaints, with credit card fraud accounting for roughly 29 percent. Each error on your credit report can cost you thousands in higher interest rates or loan denials.

Disputing errors directly with credit bureaus works sometimes, but when they ignore your dispute or reinserve inaccurate information, a lawyer’s demand carries weight they cannot ignore. The key difference between handling these issues alone and with representation comes down to leverage and knowledge of applicable law.

Your Rights Under Federal and State Law

The Fair Credit Reporting Act gives you the right to dispute inaccurate information and receive corrections within 30 days. The Fair Debt Collection Practices Act prohibits specific abusive tactics. California’s Rosenthal Fair Debt Collection Practices Act adds state-level protections beyond federal law. Many people don’t realize that violations of these laws often entitle you to damages and attorney’s fees paid by the collector or creditor, not by you.

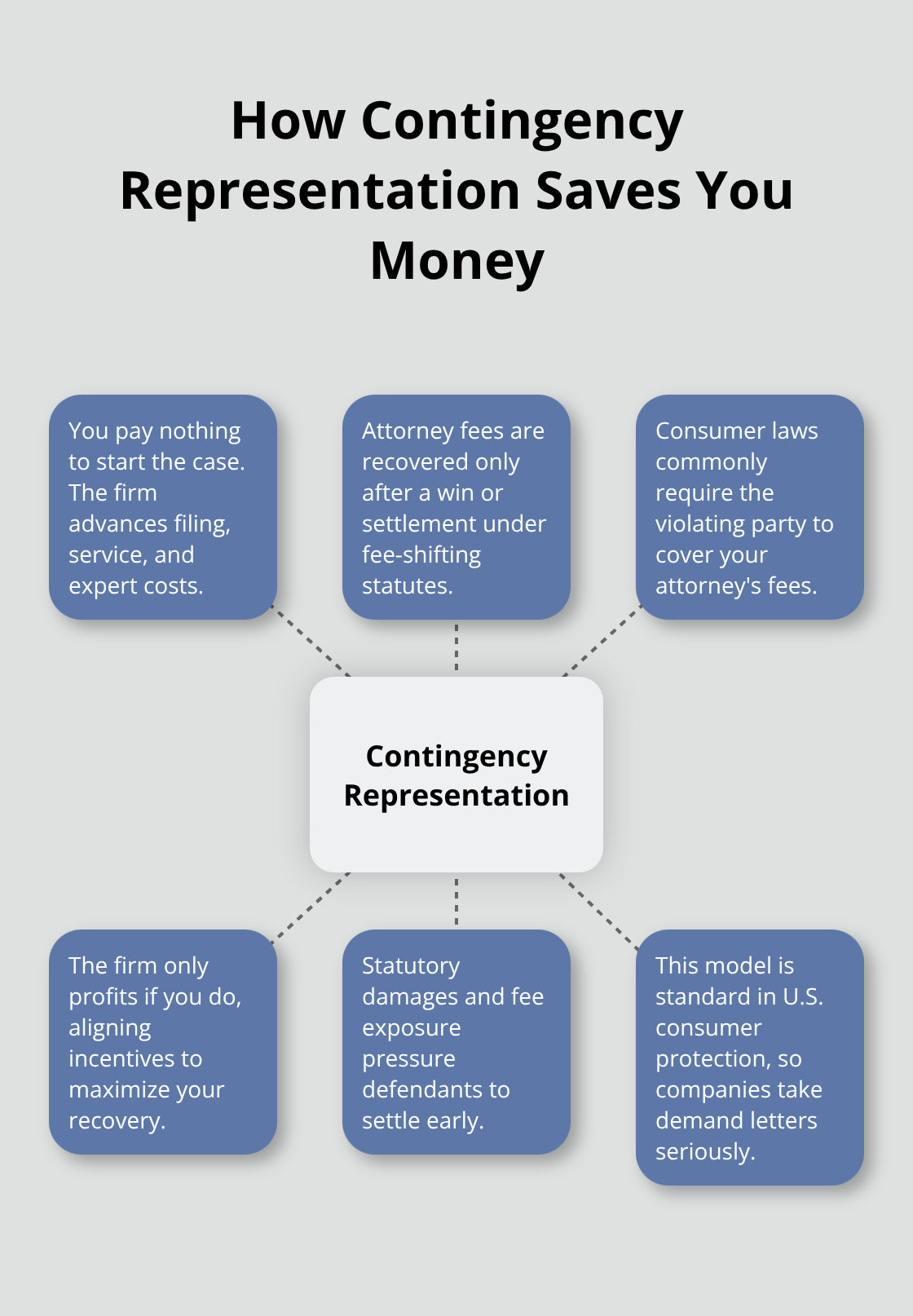

When a law firm takes your case on contingency, they advance all costs and get paid only if you win. You pay nothing upfront. Debt collectors and credit bureaus know this structure because it’s standard in consumer protection law. They also know that most consumers won’t hire lawyers, which is why violations persist. When a firm sends a demand letter backed by knowledge of case law and statutory damages, the dynamic shifts immediately.

Documentation Builds Your Foundation

Keep copies of every communication from debt collectors, every credit report you’ve pulled, every letter disputing errors, and any proof of identity theft like police reports or fraudulent account statements. The Federal Trade Commission provides identity theft resources that help you file an Identity Theft Report, which carries legal weight when disputing fraudulent accounts.

Many people wait months or years before taking action, but the longer you wait, the more damage compounds. Credit score impacts can last up to seven years. Wage garnishments happen quietly until money stops hitting your account. Acting within the first 30 to 60 days of discovering an error or unauthorized account gives you momentum and preserves your options under statute of limitations periods. Your documentation and quick action set the stage for what comes next-understanding how affordable legal representation actually works.

How Affordable Legal Help Actually Works

Why Contingency Fees Change Everything

Most people assume consumer protection attorneys cost too much. The reality flips this assumption on its head. When a law firm takes a consumer protection case, they operate on contingency-they advance every penny of litigation costs and collect payment only if you win. You pay nothing upfront, nothing during the case, and nothing at settlement unless the defendant covers your attorney’s fees (which consumer protection laws often require them to do). This structure exists because consumer protection law was built on a principle: violations should carry financial consequences for the wrongdoer. The Fair Debt Collection Practices Act, the Fair Credit Reporting Act, and similar statutes allow prevailing plaintiffs to recover attorney’s fees from the defendant.

A law firm representing you on contingency understands the math precisely-they invest their time and resources because the law itself creates a mechanism for them to recover those costs from the party that violated your rights.

The Free Case Review: What Actually Happens

Your first conversation with a consumer protection attorney costs nothing. You call or schedule online, describe your situation, and the attorney or paralegal evaluates whether your case has merit. They ask about the timeline of events, what documentation you have, which laws were violated, and what damages you’ve suffered. If they take your case, you sign a contingency agreement that spells out exactly how fees work, what costs they’ll advance, and what happens if you settle or win. No hidden charges appear later. No surprise billing arrives after settlement. No pressure to pay before results arrive. This transparency matters because you can compare different firms and understand precisely what you’re getting. Some attorneys charge higher contingency percentages but handle cases faster; others take lower percentages but move more slowly. The free initial consultation gives you the information to make that choice with full clarity about pricing and timelines.

What Separates Affordable Representation From Cheap Representation

Cost-effective legal help doesn’t mean low-quality legal help. A firm that takes your case on contingency has already decided your claim has real value-they wouldn’t invest their resources otherwise. They’ve evaluated the applicable law, assessed the defendant’s likely response, and calculated whether they can recover their costs and fees. This vetting process protects you. A firm that demands upfront fees has no skin in the game; they collect payment regardless of outcome. A firm on contingency only profits if you profit. That alignment of interests matters when your financial future hangs in the balance. The firm that takes your case must believe in it strongly enough to bet their own money on the outcome. Understanding this distinction helps you evaluate any attorney you contact and recognize which ones actually stand behind their work.

What Real Cases Look Like in Consumer Protection

Credit Bureau Errors and How Attorneys Force Corrections

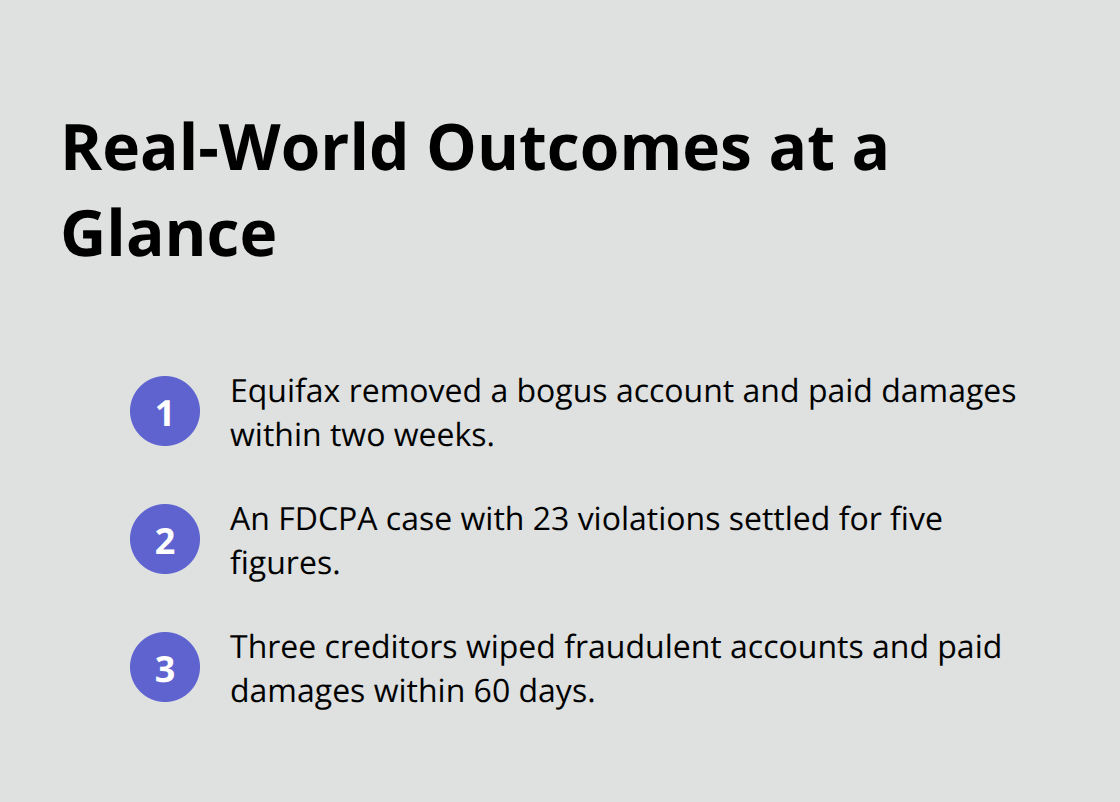

Credit bureaus make mistakes constantly, and when they do, the damage spreads fast. A consumer in California discovered Equifax listed a fraudulent account opened in her name, tanking her credit score by 87 points within weeks. She disputed the error directly with Equifax three times over four months. Each time, Equifax reinserted the inaccurate information back into her report, claiming they verified it with the creditor. The creditor, naturally, had no record of her because they never opened the account. This cycle repeats thousands of times yearly because credit bureaus face minimal consequences for sloppy verification. Once a consumer protection attorney sent a demand letter citing the Fair Credit Reporting Act and documenting the reinsertion violations, Equifax settled within two weeks, removed the account, and paid damages for the FCRA violations. The consumer recovered thousands without spending a dime upfront.

Debt Collectors and Statutory Damages

Debt collectors operate with similar brazenness. A collector called a consumer at 6:45 a.m., before the legal 8 a.m. window, demanding payment for a debt the consumer had already settled. The collector called again at 10 p.m. The consumer documented each violation. When an attorney reviewed the case, they identified 23 separate Fair Debt Collection Practices Act violations across three weeks of calls. The collector’s own records proved every violation. That case settled for five figures because the FDCPA allows statutory damages of up to $1,000 per violation, plus actual damages, plus attorney’s fees. The consumer paid nothing.

Identity Theft Across Multiple Accounts

Identity theft cases operate differently because the damage multiplies across multiple accounts and months. A consumer discovered fraudulent charges spanning three credit cards, a personal loan, and utility accounts opened in their name. They filed an Identity Theft Report with the FTC, which provided them with a recovery plan template. However, the creditors ignored their disputes, claiming the accounts were legitimate. One creditor even pursued collections against them for the fraudulent debt. At this point, an attorney’s involvement became essential. The attorney sent demand letters to each creditor citing violations of the Fair Credit Reporting Act and the Identity Theft Enforcement and Restitution Act, attaching the FTC Identity Theft Report and police report. Within 60 days, three creditors settled, removed the fraudulent accounts, and paid damages. The consumer recovered enough to cover identity theft monitoring services for years and repair costs.

How Documentation Creates Leverage

These outcomes share a pattern: documentation plus legal knowledge equals leverage. Collectors and credit bureaus count on consumers not understanding their rights or lacking the resources to fight back. A single demand letter from an attorney shifts that equation instantly because these companies employ compliance teams that understand statutory damages and litigation costs far better than most consumers do. They settle cases they know they’ll lose rather than face discovery, depositions, and trial. Your documentation of violations (combined with an attorney who understands applicable federal law) creates the conditions where defendants choose settlement over defense.

Final Thoughts

Debt collectors won’t stop calling, and credit bureaus won’t fix errors on their own. These problems persist because most people believe fighting back requires money they don’t have. That belief is wrong, and an affordable consumer protection attorney proves it every day through contingency representation that costs you nothing upfront.

When a firm takes your case on contingency, they advance every cost and collect payment only if you win. Often the defendant pays your attorney’s fees under federal law, which means you start with nothing owed and end the same way unless you recover damages. Your documentation-call logs, credit reports, dispute letters, police reports for identity theft-builds the foundation that forces defendants to take you seriously.

The free case review removes the final barrier to action. Call or schedule online, describe what happened, and listen to whether your situation qualifies for legal action. At Bontrager Law, we represent California consumers in credit reporting disputes, identity theft cases, and unlawful debt collection claims. Start with a free case review and take the first step toward protecting your financial future.