A single error on your credit report can cost you thousands in higher interest rates or rejected loan applications. California’s Fair Credit Reporting Act (FCRA) reporting requirements give you powerful tools to fight back against inaccurate information that damages your financial life.

At Bontrager Law, we’ve helped countless Californians dispute false entries and hold creditors accountable. This guide walks you through your rights and the practical steps to protect your credit file.

What the FCRA Is and Why It Matters in California

The Fair Credit Reporting Act became law in 1970 to establish baseline rules for how credit bureaus collect, use, and share your financial information. The federal statute applies nationwide, but California has layered additional protections on top through the Consumer Credit Reporting Agencies Act and the Investigative Consumer Reporting Agencies Act. This matters because when federal and California rules conflict, the stricter rule applies to you-giving Californians significantly stronger rights than residents in other states.

The FCRA itself grants you the right to access your credit report free once per year from Experian, Equifax, and TransUnion, dispute inaccuracies within 30 days of discovery, and receive notice when negative information is added to your file. California tightens these protections further by limiting how long negative items stay on your report and restricting what employers can see.

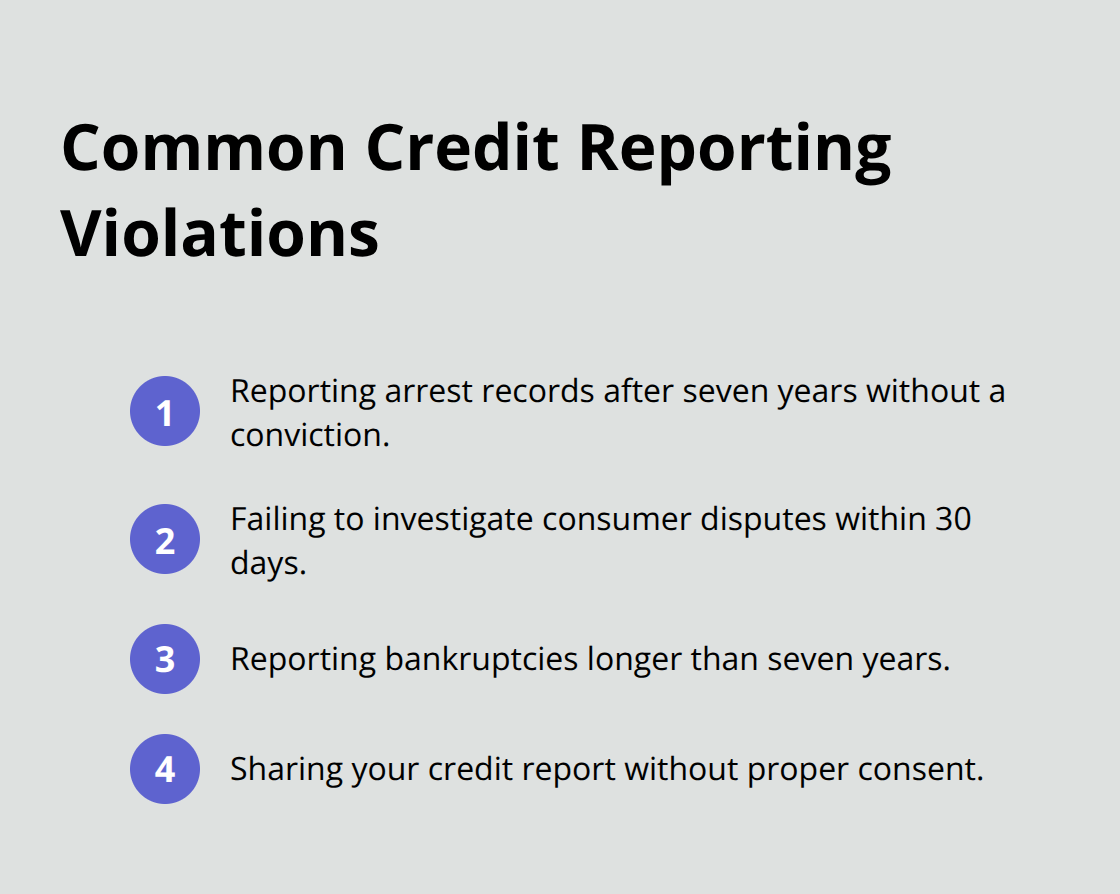

How Credit Reporting Violations Happen

Credit reporting violations occur constantly because the three major bureaus handle millions of files with minimal human review. Common violations include reporting arrest records after seven years without a conviction, failing to investigate disputes within 30 days, reporting bankruptcies longer than seven years, and sharing your report without proper consent. These aren’t technical mistakes-they directly cost you money.

A single inaccuracy can result in loan denials, higher interest rates that compound over years, rejected housing applications, or job offers withdrawn. The Consumer Financial Protection Bureau and Federal Trade Commission enforce FCRA compliance, but enforcement moves slowly.

What Violations Cost You

Willful violations carry statutory damages of $100 to $1,000 plus actual damages and attorney’s fees under 15 U.S.C. § 1681n, while negligent violations allow recovery of actual damages plus costs and attorney’s fees under 15 U.S.C. § 1681o. California’s stricter framework creates additional liability, meaning bureaus and employers face greater financial exposure for violations here than elsewhere.

Taking Action Against Reporting Errors

If you’ve been denied credit, employment, or housing due to reporting errors, the path forward involves disputing the inaccuracy directly with the bureau, documenting the impact, and pursuing damages if the bureau fails to correct it within 30 days. Understanding your specific rights under both federal and California law positions you to hold reporting agencies accountable and recover what you’ve lost-which brings us to the concrete rights you hold as a California resident.

What You Can Actually Do About Reporting Errors

Pull Your Reports and Spot the Mistakes

California law gives you three concrete powers that most residents never use. First, you can request your credit report free from each of the three major bureaus-Experian, Equifax, and TransUnion-once every 12 months through AnnualCreditReport.com, the only federally authorized source. Pull all three reports and compare them because errors often appear on one bureau but not the others. Look specifically for accounts you don’t recognize, wrong payment histories, incorrect balances, and closed accounts still listed as open.

File a Written Dispute Within 30 Days

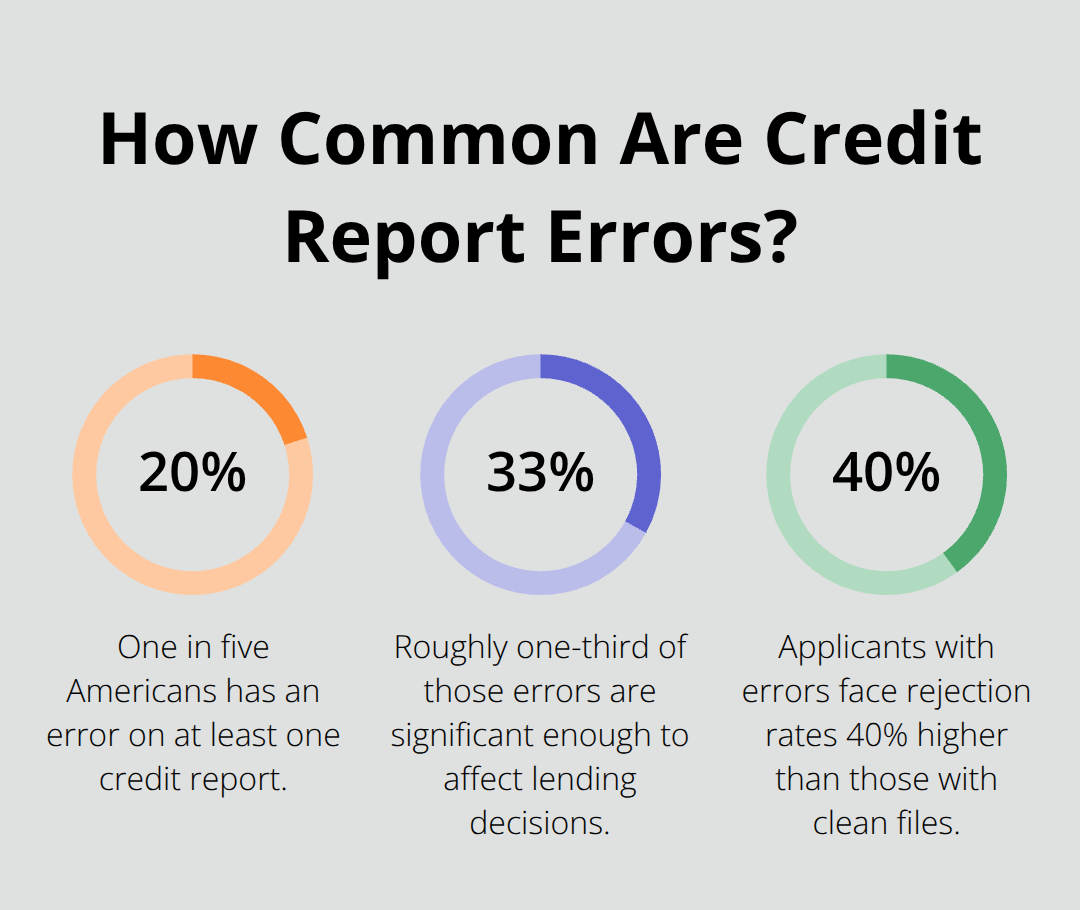

Under the FCRA, you have 30 days from discovery to dispute inaccuracies, and the bureaus must investigate within that window. Send your dispute in writing to the bureau’s disputes department-email or certified mail-because phone calls create no paper trail. Include copies of documentation supporting your claim: bank statements, payment receipts, or correspondence showing the account should be removed or corrected. The bureau then contacts the creditor who reported the information and asks them to verify it. If the creditor cannot verify the account within 30 days, the bureau must remove it. The Federal Trade Commission reports that one in five Americans has an error on at least one credit report, and roughly one-third of those errors are significant enough to affect lending decisions.

Leverage California’s Stronger Removal Rights

California’s Consumer Credit Reporting Agencies Act gives you stronger removal rights than federal law alone provides. Negative items typically fall off after seven years, but California shortens this for certain records: arrest information without conviction must be removed immediately, and bankruptcies disappear after seven years instead of the federal 10-year limit. If a bureau violates these timelines, you can sue under California law for damages.

Recover Damages When Violations Occur

When violations occur-whether the bureau ignored your dispute, failed to investigate within 30 days, reported information it couldn’t verify, or shared your report without consent-you can recover statutory damages of $100 to $1,000 per violation plus actual damages showing what the error cost you (denied credit, higher interest rates, lost job opportunity), punitive damages if the violation was willful, and attorney’s fees. This last point changes everything: because the law covers attorney’s fees, many firms handle FCRA cases without requiring upfront payment from you. Document the impact of each error carefully-pull loan denial letters, screenshots showing interest rate quotes before and after the error, and any communications showing harm.

These three powers-accessing your reports, disputing inaccuracies, and recovering damages-form the foundation of your FCRA rights. But knowing your rights means nothing without understanding how reporting errors actually damage your financial life and what that damage looks like in concrete terms.

How Credit Reporting Errors Tank Your Financial Opportunities

Immediate Impact on Loan Approvals and Interest Rates

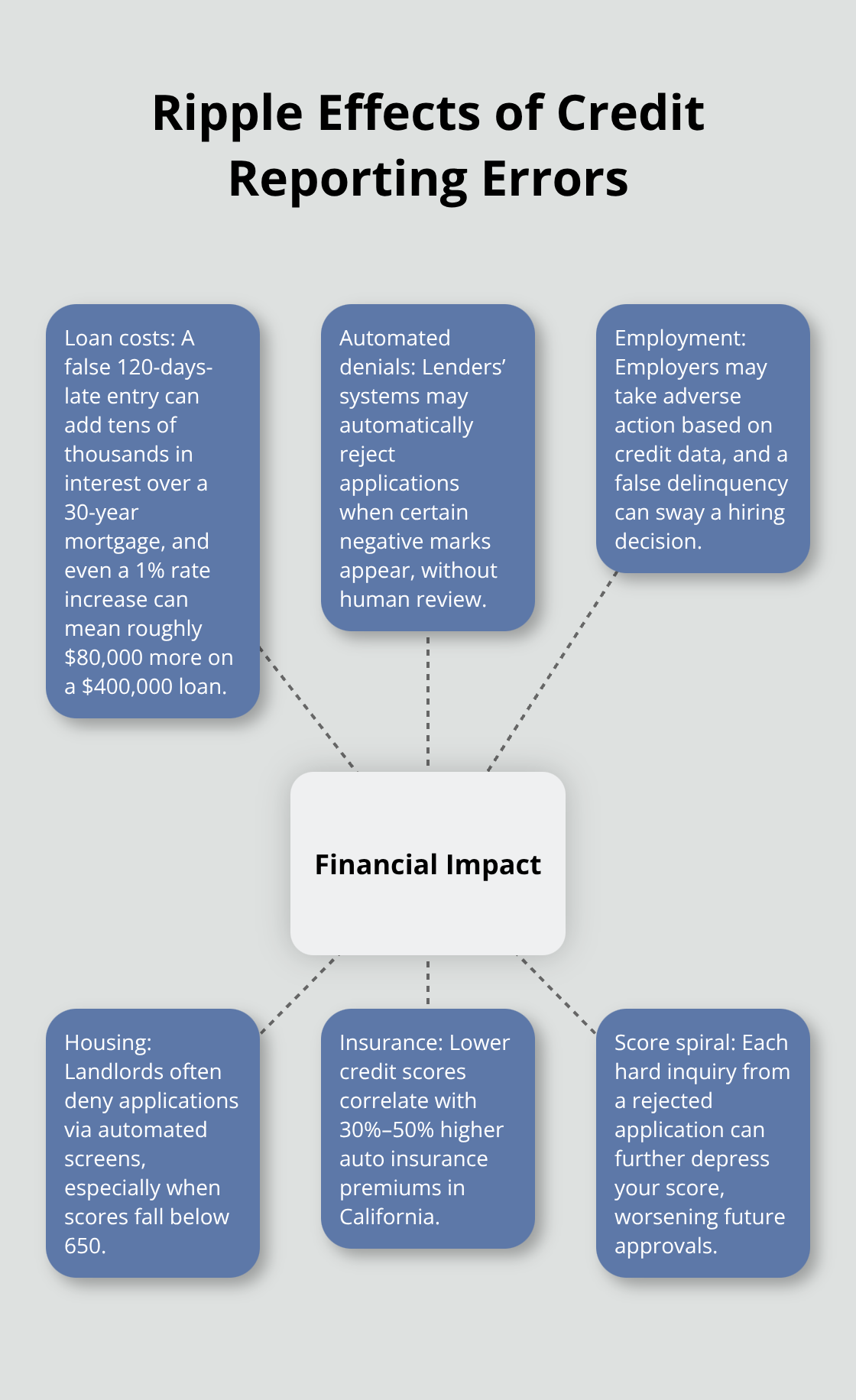

A single inaccuracy on your credit report doesn’t sit there harmlessly-it actively destroys your financial options. When lenders pull your report during a mortgage application, they see inflated debt totals, missed payments you never made, or accounts belonging to someone else entirely. That $5,000 error reporting a payment 120 days late costs you $40,000 in additional interest over a 30-year mortgage, according to analysis by the National Association of Consumer Advocates. Many lenders use automated systems that instantly reject applications when certain negative marks appear, meaning a human never reviews your file to catch the mistake. The difference between a 3.5% and 4.5% interest rate on a $400,000 home means you pay roughly $80,000 more over the life of the loan-all because a bureau failed to remove a paid-off account or investigate a fraudulent entry you disputed 90 days ago.

Employment and Housing Rejections

Employment and housing decisions hinge on credit reports more than most Californians realize. California law requires employers to provide written notice before pulling your report and to notify you if they take adverse action based on it, but many skip this step or bury the notification in hiring paperwork. When a reporting error tanks your credit score, landlords increasingly deny applications based on automated screening systems that flag anything below 650. The National Credit Reporting Association data shows that applicants with errors on their reports face rejection rates 40% higher than those with clean files. You lose the apartment, the job offer, or the loan-then spend months trying to reverse the decision even after the error is corrected. Employers conducting background checks through agencies like Equifax Workforce Solutions often rely on credit data alongside criminal history, and a false delinquency swings a hiring decision without you ever knowing the real reason you faced rejection. Housing discrimination compounds this harm: if you face denial of a rental because of a reporting error, you’re forced into less desirable housing, longer commutes, or neighborhoods with fewer services-costs that compound for years.

Long-Term Damage to Your Credit Score and Financial Future

The long-term financial impact of reporting errors extends far beyond the immediate denial. Your credit score influences insurance premiums in California, with drivers carrying lower scores paying 30% to 50% more for auto insurance according to the National Association of Insurance Commissioners. Utility companies, cell phone providers, and even some employers check credit scores as a proxy for financial responsibility, meaning a single error affects your ability to secure basic services. Once negative information lands on your report, it stays there for years unless you actively dispute it-and most people never do. The Federal Trade Commission reports that fewer than 5% of Americans ever dispute errors on their credit reports, which means inaccurate information compounds in silence, damaging your score repeatedly across multiple lender inquiries and applications.

If incorrect information remains on your credit report after you have disputed it, legal action may be an option. Each hard inquiry from a rejected application further depresses your score, creating a downward spiral where one error triggers cascading financial damage.

Final Thoughts

The FCRA reporting requirements in California hand you concrete power to fight inaccurate information that costs you money. You can pull your credit reports free from all three bureaus annually, dispute errors within 30 days and force investigation, leverage California’s stricter removal timelines, and recover damages when violations occur. Most Californians never use these rights, which means inaccurate information sits on their reports for years, silently destroying their financial opportunities.

Start by pulling your reports from AnnualCreditReport.com and comparing all three. Look for accounts you don’t recognize, wrong payment histories, and closed accounts still listed as open. If you find errors, send written disputes to each bureau’s disputes department with supporting documentation. Document everything the error costs you: loan denials, higher interest rates, rejected housing applications, or lost job opportunities.

If reporting errors have damaged your financial life, contact Bontrager Law for a free case review. We represent Californians across the state in credit reporting disputes, identity theft claims, and related consumer protection matters. With nearly 20 years of experience and millions recovered for clients, we know how to hold reporting agencies accountable and recover what inaccurate information has cost you.