Your credit report shapes your financial future, yet many Californians don’t fully understand their FCRA rights. Errors on your report can cost you thousands in higher interest rates or denied applications.

At Bontrager Law, we’ve seen how quickly inaccurate information damages credit scores. This guide walks you through your protections under the Fair Credit Reporting Act and shows you exactly how to fight back against reporting violations.

What the FCRA Actually Does for You

The Fair Credit Reporting Act is a federal law passed in 1970 that regulates how credit reporting agencies collect, maintain, and share your financial information. It applies to every state, including California, and it gives you concrete rights that most people never use. The FCRA doesn’t prevent negative information from appearing on your report-it prevents inaccurate information from staying there.

Credit Reporting Agencies Must Follow Strict Rules

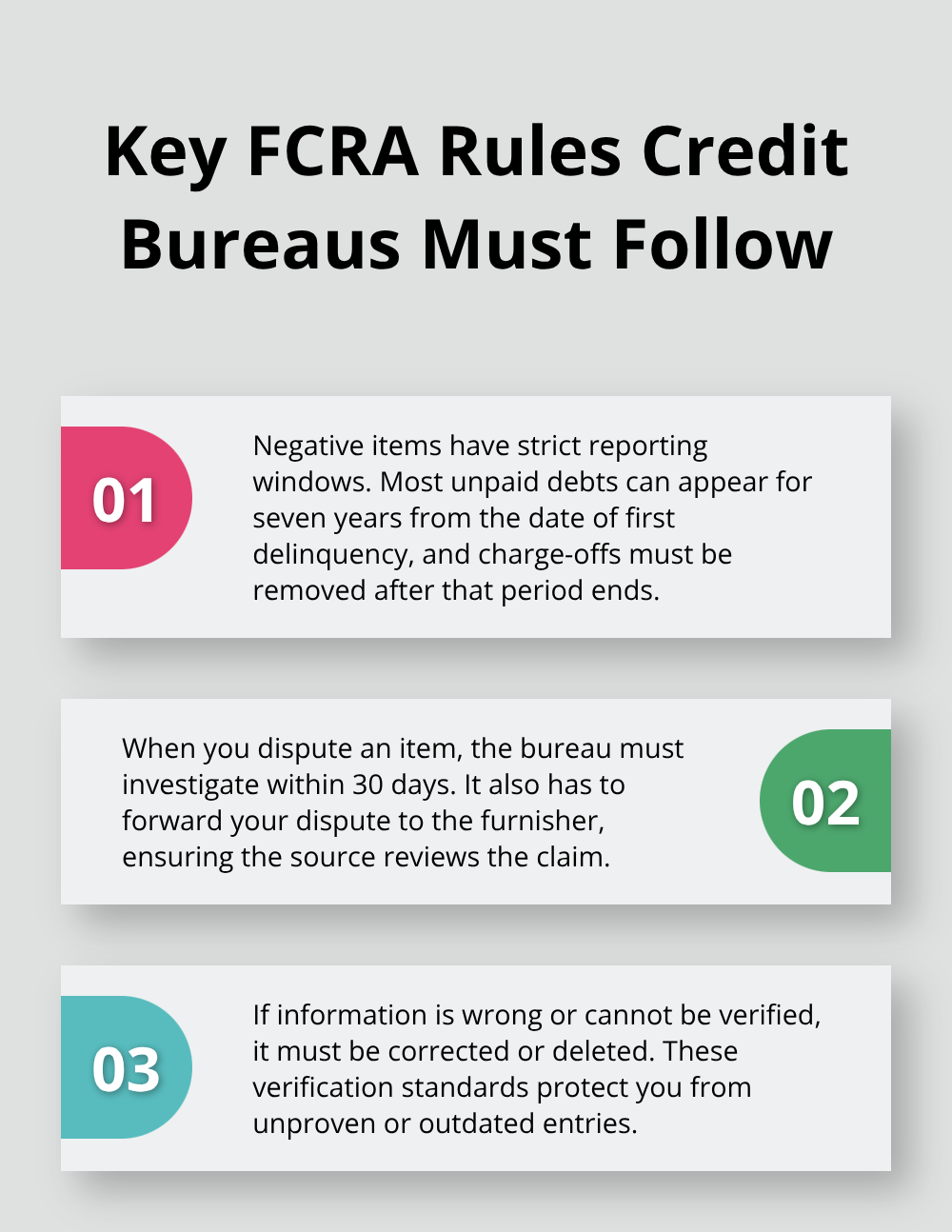

Credit reporting agencies like Equifax, Experian, and TransUnion must follow strict rules about what they can report and how long they can report it. Under the FCRA, unpaid debts typically stay on your credit report for seven years from the date of first delinquency. Medical debt now has different rules following SB 1061 in 2024, and charge-offs must be removed after the seven-year period ends. The law also requires these agencies to investigate disputes within 30 days and to forward your dispute to the company that originally reported the information, called the furnisher.

If they find the information was wrong or cannot verify it, they must delete or correct it.

Why Inaccurate Reports Cost You Real Money

Inaccurate credit reports directly affect your ability to get loans, secure housing, and sometimes even land employment. A single error can cost you thousands in higher interest rates or result in denied applications. This matters because lenders, landlords, and employers rely on these reports to make decisions about you.

California Adds Its Own Layer of Protection

California adds its own layer of protection through the California Consumer Credit Reporting Agencies Act, which works alongside the federal FCRA. The state law requires that credit reporting companies use fair, impartial procedures and prohibits contract terms that try to override these protections. California also has strict privacy laws through the Gramm-Leach-Bliley Act and California Financial Information Privacy Act that limit how financial institutions share your personal information.

Your Right to Opt Out and Sue for Violations

These state laws mean you have the right to opt out of sharing your financial data with outside companies and, in some cases, with affiliates of the institution itself. The California Department of Financial Protection and Innovation and the California Attorney General enforce these protections, and violations can result in complaints being filed against financial institutions. If a credit reporting agency or furnisher violates your rights under these laws, you can sue for actual damages or statutory damages between $100 and $1,000 per violation (or $1,000 per violation if the violator is an individual). You can also recover attorney’s fees and costs if you win, which makes pursuing violations financially realistic even for smaller disputes.

Understanding these protections sets the foundation for taking action. The next section shows you exactly what rights you have when you spot errors on your own credit report and how to exercise them.

What to Do When You Find Credit Report Errors

Start by Pulling All Three Credit Reports

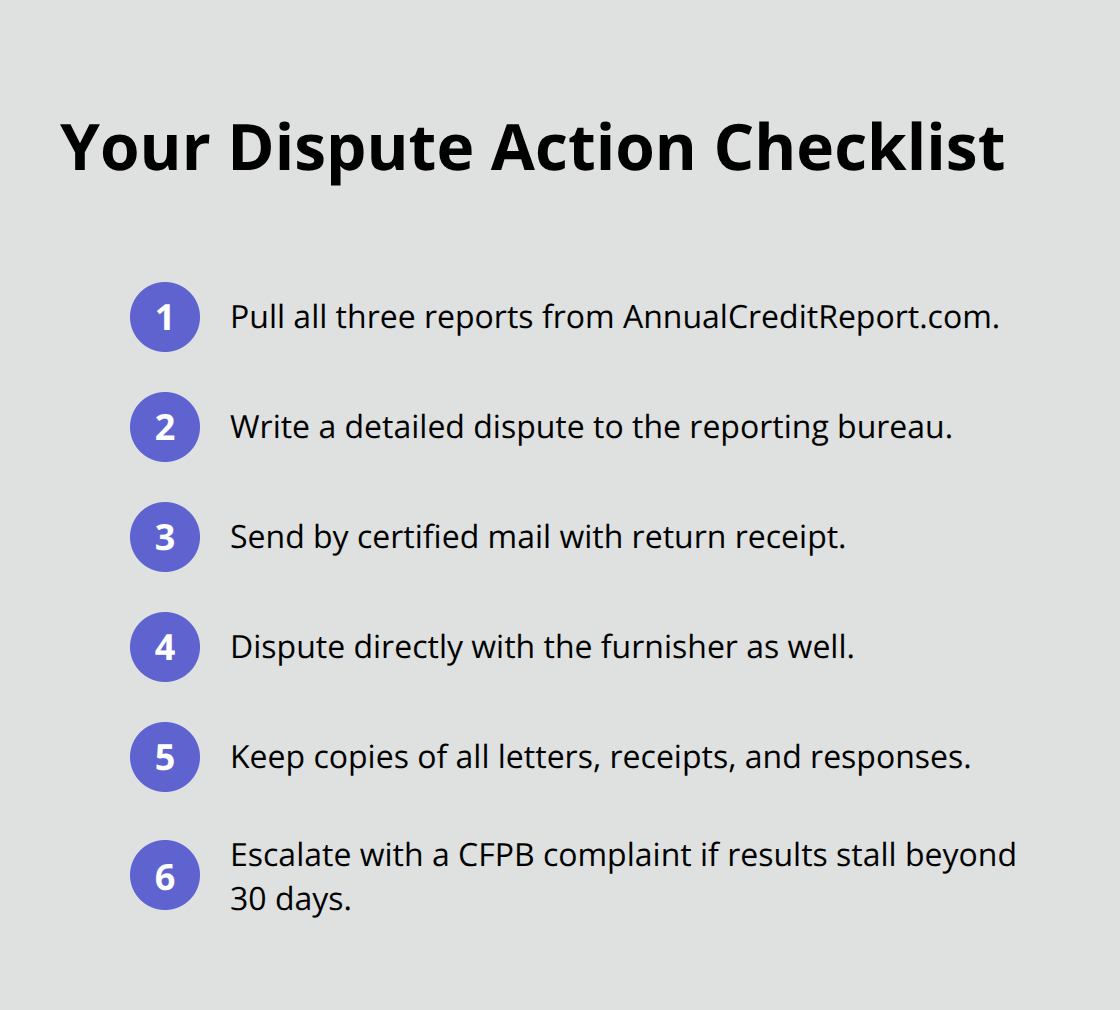

The moment you spot an error on your credit report, you have a legal right to challenge it, and the process is more straightforward than most people think. Obtain your free annual credit report from each of the three major bureaus-Equifax, Experian, and TransUnion-through AnnualCreditReport.com, the only federally authorized source for free reports. Many people check only one bureau and miss errors that appear on others; pull all three reports since different lenders report to different agencies.

File a Written Dispute with the Credit Bureau

When you find an error, write a detailed dispute letter to the bureau that reported it. Include your full name, current address, phone number, the account number in question, and a clear explanation of what’s wrong with supporting documents. Send this letter using certified mail with return receipt requested-this creates proof of delivery that protects you if the bureau claims they never received it. Under the FCRA, the bureau must investigate your claim within 30 days and forward your dispute to the furnisher, the original company that reported the information. The furnisher typically has 30 days to investigate, and if they find the information was wrong or cannot verify it, they must update or remove it from all three bureaus.

Dispute Directly with the Furnisher Too

Don’t stop at disputing with the bureau; also send a written dispute directly to the furnisher-the bank, landlord, creditor, or collection agency that supplied the inaccurate data. This dual approach applies pressure and creates a paper trail. If the furnisher cannot verify the information, they must notify the bureaus for correction or removal. You also have the right to know who has accessed your credit report, and you can request this information from each bureau. If someone pulled your report without authorization, that’s a violation you can challenge.

Document Everything and Escalate if Needed

After disputing, keep thorough records of everything: your letters, supporting documents, certified mail receipts, and responses from both the bureau and furnisher. If you disagree with the results, file a complaint with the Consumer Financial Protection Bureau, which provides a template letter and instructions to streamline the process. The CFPB tracks complaints and can investigate agency practices that harm consumers. If the violation is significant-such as the bureau failing to investigate or the furnisher refusing to correct verified errors-you have the right to sue for actual damages or statutory damages of $100 to $1,000 per violation, plus attorney’s fees if you win.

When disputes don’t resolve the problem, legal action becomes your next option, and understanding what violations qualify for a lawsuit helps you determine whether to pursue a claim.

Fighting Credit Reporting Violations

File a CFPB Complaint When Disputes Stall

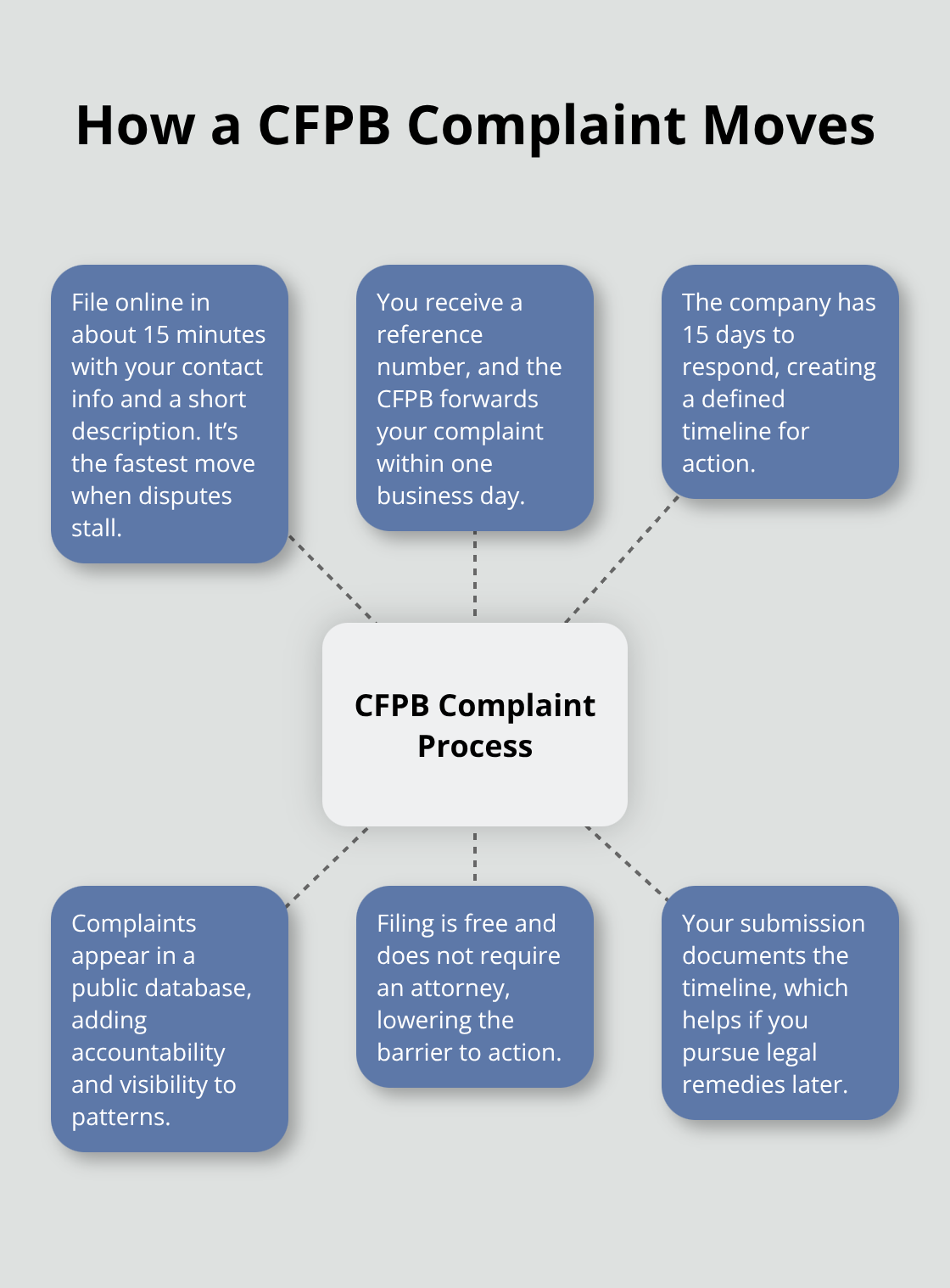

The CFPB received over 2.7 million complaints in 2024, with credit reporting issues ranking among the top concerns consumers file. If your dispute with a credit bureau or furnisher stalls, the CFPB offers your fastest path forward. File your complaint through the CFPB’s online portal at ConsumerFinance.gov, which takes about 15 minutes and requires only your name, contact information, and a description of what happened. The CFPB assigns your complaint a reference number and forwards it to the company within one business day. The company then has 15 days to respond, and the CFPB publishes a public database of all complaints, which creates accountability when companies see their patterns exposed. Many bureaus and furnishers prioritize CFPB complaints because the agency tracks response times and complaint resolution rates.

Your complaint costs nothing and requires no legal representation, making it the most practical first step when informal disputes fail. Document your timeline carefully: note the date you sent your initial dispute letter, when you received responses, and what the bureau or furnisher claimed they investigated. This documentation becomes critical if you later pursue legal action, since courts want to see you exhausted administrative remedies first.

Understand Your Right to Sue for Violations

The Fair Credit Reporting Act allows you to sue credit reporting agencies, furnishers, and third-party debt collectors in state or federal court for statutory damages ranging from $100 to $1,000 per violation, plus actual damages if you can prove financial harm. If the violator is an individual rather than a company, statutory damages jump to $1,000 per violation. You can also recover attorney’s fees and court costs if you win, which means a firm can take these cases on contingency and advance the legal costs. The statute of limitations for FCRA violations is two years from discovery or five years from the violation itself, giving you a reasonable window to act.

Many consumers wait too long, assuming violations will resolve on their own, but credit bureaus only respond when pressured. Contact a consumer protection firm once your CFPB complaint has been pending for 30 days without meaningful resolution, or immediately if the violation caused documented financial harm (such as a denied mortgage or higher interest rates). A free case review clarifies whether your claim has value and what damages you might recover.

Final Thoughts

Your FCRA rights in California give you concrete tools to fight inaccurate credit reporting, yet most people never use them. Credit bureaus and furnishers must investigate disputes within 30 days, remove unverifiable information, and correct errors that damage your financial standing. California’s additional protections through the Consumer Credit Reporting Agencies Act and state privacy laws strengthen these federal safeguards, meaning you have multiple layers of legal protection when your credit report contains false information.

A single error costs thousands in higher interest rates, denied housing applications, or lost job opportunities. The seven-year reporting period means inaccurate information lingers long enough to cause real financial harm, which is why you must act quickly. When you spot an error, pull all three credit reports from AnnualCreditReport.com and file written disputes with both the bureau and the furnisher using certified mail, then file a CFPB complaint if disputes stall beyond 30 days.

If informal resolution fails, you can sue for statutory damages of $100 to $1,000 per violation, plus attorney’s fees if you win. This legal remedy exists because credit reporting errors are widespread and companies respond only when facing consequences. Contact Bontrager Law for a free case review if the bureau or furnisher refuses to correct verified errors or fails to investigate your FCRA rights in California.