The Fair Credit Reporting Act protects your financial reputation, but the rules governing it keep changing. Recent FCRA rights updates have shifted how credit bureaus report information, how you can dispute errors, and what data brokers must disclose.

At Bontrager Law, we’ve seen how these changes affect our clients’ ability to challenge inaccurate reports and protect their credit. This guide walks you through what’s new and what it means for your financial life.

What Changed in FCRA Rules This Year

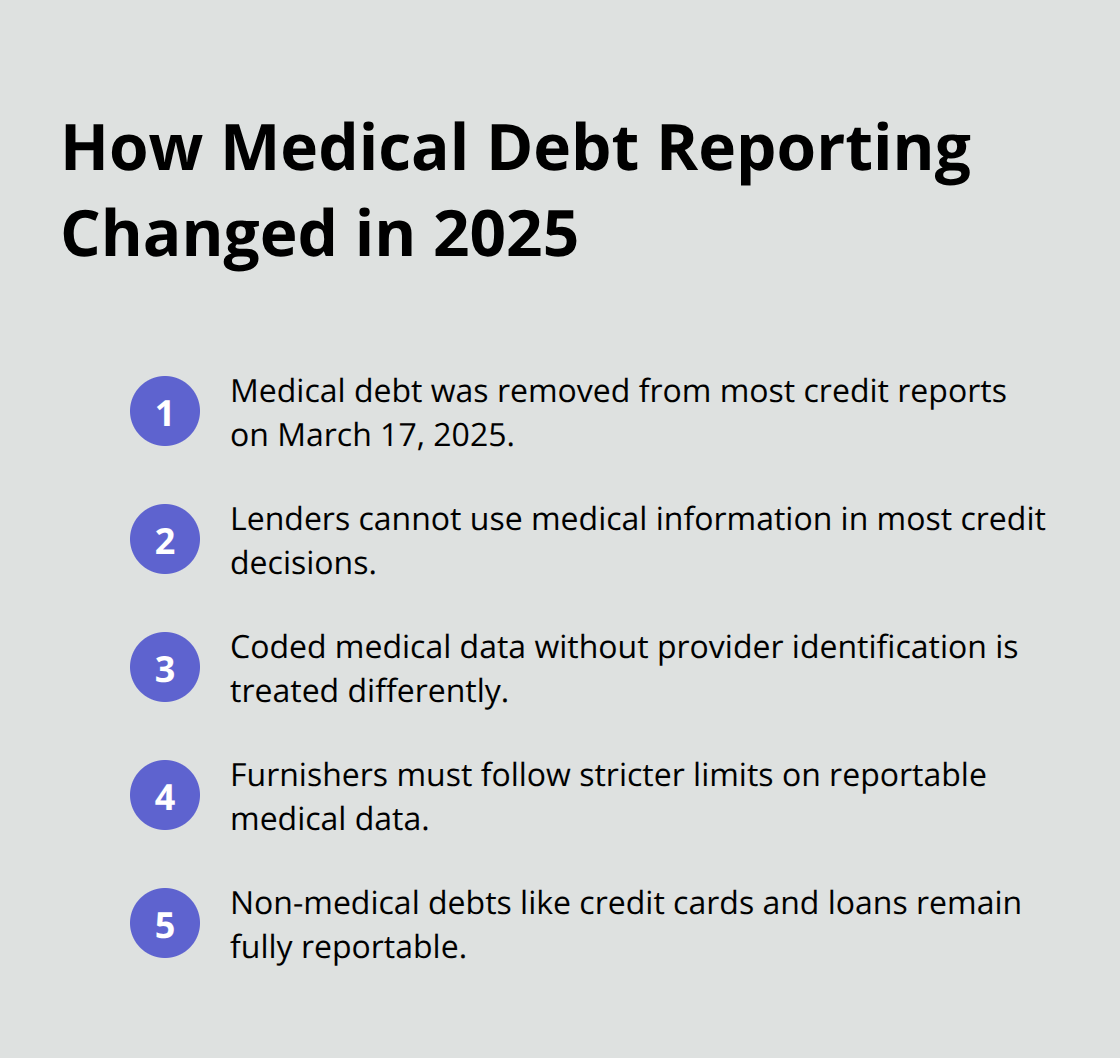

The FCRA landscape shifted significantly in 2025, and the changes directly affect how your credit information flows through the system. On January 1, 2025, the maximum fee for obtaining your credit file jumped to $15.50, up from $14.50, according to the Federal Register. More importantly, starting March 17, 2025, credit bureaus and creditors stopped reporting medical debt on most credit reports following a CFPB final rule. This change matters because medical debt no longer tanks your credit score the way it used to-lenders can no longer use medical information to make credit decisions in most situations. The court vacated the CFPB’s broader medical information rule in July 2025, but the practical effect remains: coded medical debt without provider identification now receives different treatment, and furnishers must follow stricter guidelines on what medical data they can report.

Medical Debt No Longer Dominates Credit Decisions

Medical debt removal represents the most tangible change affecting your creditworthiness. Before March 2025, a hospital bill sent to collections could devastate your score even if you had excellent payment history elsewhere. Now that medical accounts are largely excluded from reporting, lenders adjust their underwriting processes accordingly.

If you apply for credit, expect less scrutiny around past medical issues. Non-medical debt remains fully reportable, so credit card defaults and missed loan payments still appear on your file. The CFPB also clarified that furnishers must handle disputes more carefully, investigating claims across multiple consumers when systemic errors emerge-not just individual disputes.

Data Brokers Face New Transparency Rules

Data brokers operated with minimal oversight historically, but the CFPB proposed rules in December 2024 that would treat data brokers as consumer reporting agencies if they assemble or evaluate personal information for third-party sharing. Though the CFPB withdrew broader proposed rules by May 2025, the regulatory direction is clear: data brokers will face tighter FCRA obligations. Credit header data like your name, address, and Social Security number can no longer be sold freely for marketing purposes under future rules. This matters because data brokers have expanded dramatically, often using AI tools to profile consumers for everything from lending to employment screening. The proposed rules would require written consumer consent or a legitimate business need before data sharing occurs, giving you more control over who accesses your personal information.

What This Means for Your Credit Applications

These changes reshape how lenders evaluate your creditworthiness and what information they can access. Creditors now receive less medical data in consumer reports, which means they focus more heavily on payment history and outstanding balances. Data brokers will eventually face restrictions on selling your personal information without consent, reducing the volume of third-party data used in credit decisions. If you’ve struggled with medical debt in the past, the March 2025 prohibition offers real relief-those accounts no longer haunt your credit file. Moving forward, understanding these shifts helps you anticipate how lenders will view your application and what disputes you can file if errors appear.

What FCRA Rights Actually Mean for You

Access Your Credit Report Without Breaking the Bank

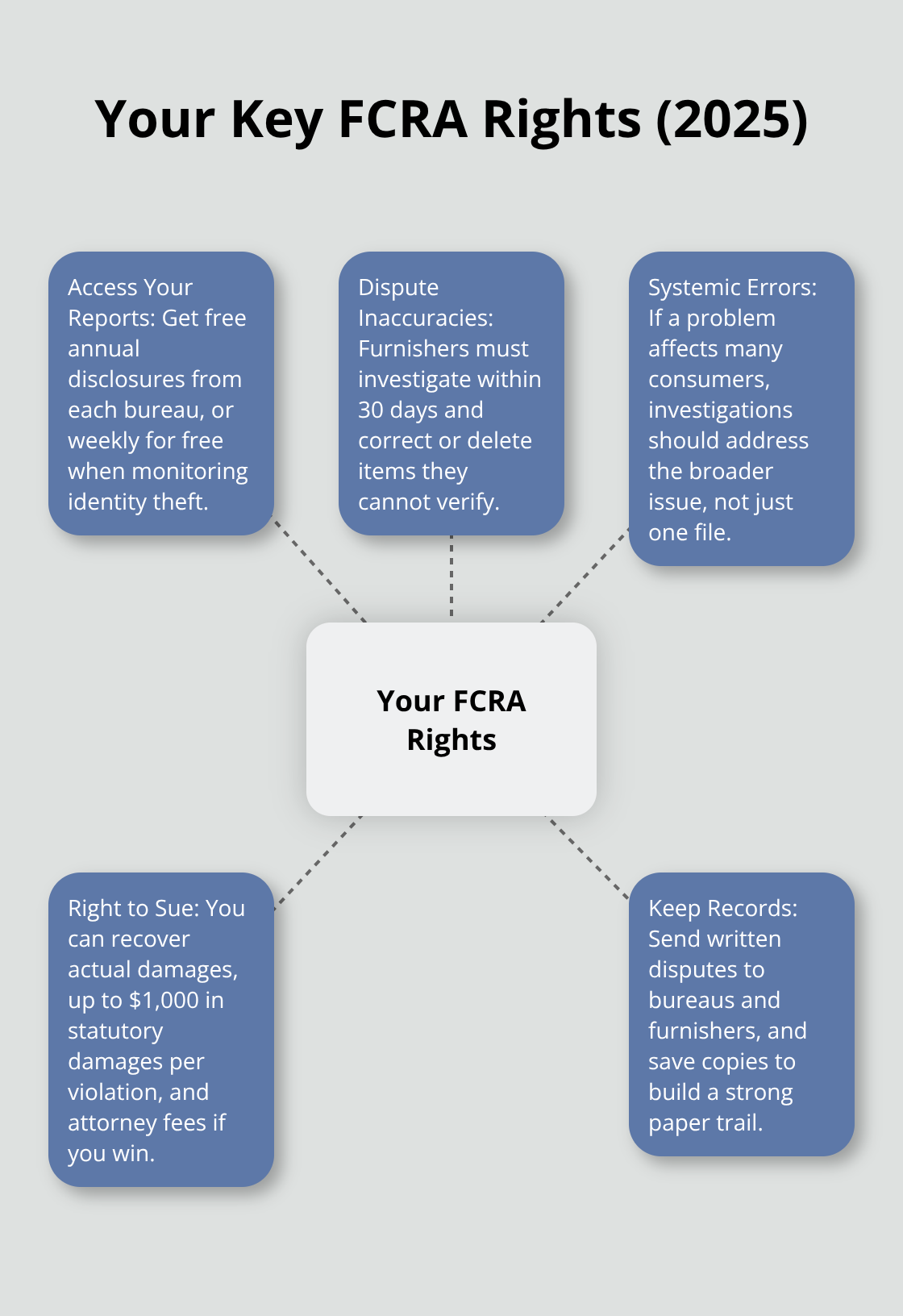

The FCRA gives you the right to access your credit report from any consumer reporting agency that maintains a file on you. You can obtain it free once per year from each of the three major bureaus through AnnualCreditReport.com, or weekly for free if you monitor for identity theft. The Federal Register increased the maximum fee for paid disclosures to $15.50 as of January 1, 2025, so plan for that cost if you need multiple reports beyond your free allotments.

Most people miss the real value of accessing reports regularly-catching errors before they damage your credit score. A late payment that doesn’t belong to you or a medical account still lingering after the March 2025 prohibition should have removed it will tank your creditworthiness if left unchecked. Pull your reports from all three bureaus at staggered intervals rather than all at once, giving you quarterly visibility into what lenders actually see.

Challenge Inaccurate Information Through Formal Disputes

Your second right is the ability to dispute inaccurate information, and the FCRA’s recent changes strengthen your position significantly. When you file a dispute, the furnisher-the company reporting the information-must investigate within 30 days and correct or delete the disputed item if they cannot verify it as accurate. The CFPB clarified in 2025 that furnishers must investigate systemic errors across multiple consumers, not just individual disputes, meaning if a debt collector reports false information to thousands of people, your dispute can trigger an investigation that helps others too.

Many disputes fail because people submit them passively. Send written disputes directly to the credit bureau and the data furnisher simultaneously, keep copies of everything, and follow up after 30 days if you hear nothing. This approach creates a documented record that protects you if the dispute stalls.

Sue for Violations and Recover Damages

Your third right allows you to sue for violations-the FCRA permits you to recover actual damages, statutory damages up to $1,000 per violation, and attorney fees if you win. This structure makes violations expensive for companies and worth pursuing. Courts have found that failing to investigate disputes, reporting inaccurate information, and furnishing data without proper authorization all trigger liability, and creditors know this, which is why many settle disputes when faced with documented violations.

The combination of these three rights creates real leverage. Companies that ignore your access requests, dismiss your disputes, or furnish inaccurate data face financial consequences that motivate compliance. Understanding how to exercise each right transforms them from theoretical protections into practical tools that shape how your credit information flows through the system.

How FCRA Updates Reshape Your Credit Strategy

Medical Debt Disputes Now Work in Your Favor

The medical debt prohibition that took effect on March 17, 2025 transforms how you approach credit repair. If you filed disputes before that date targeting medical accounts, those disputes may have stalled because furnishers claimed the debt was valid. Now that same debt cannot legally appear on your report, which means your dispute has merit even if the original bill was legitimate. Pull your credit reports immediately after March 17 to identify medical accounts that should have been removed. If they remain, you have a violation to dispute. The 30-day investigation window the CFPB clarified in 2025 now works in your favor because furnishers cannot verify medical information as reportable.

Focus Your Disputes on Documentable Errors

Beyond medical debt, the broader dispute timeline stays at 30 days, but the shift in what data furnishers can legally report compresses their ability to defend inaccurate items. Non-medical debt still requires full investigation, so target your disputes on accounts with clear errors-wrong amounts, accounts that don’t belong to you, or closed accounts still showing as open. The CFPB’s 2025 guidance requires furnishers to investigate systemic errors across multiple consumers. If a debt collector reports false information to thousands of people, your individual dispute can trigger a broader investigation that forces corrections at scale.

How Lenders Now Evaluate Your Application

Creditors now build credit decisions around payment history and utilization rather than medical information, which fundamentally alters how lenders perceive your application. Data brokers selling your personal information faced proposed FCRA restrictions in December 2024 that would require written consent before sharing credit header data for marketing or employment screening. Though broader rules withdrew in May 2025, the regulatory direction signals tighter controls ahead. Lenders traditionally accessed data-broker profiles to supplement credit reports with behavioral signals. As data-broker access tightens, lenders rely more heavily on official credit reports and your direct financial history with them.

Protect Yourself Against Identity Theft

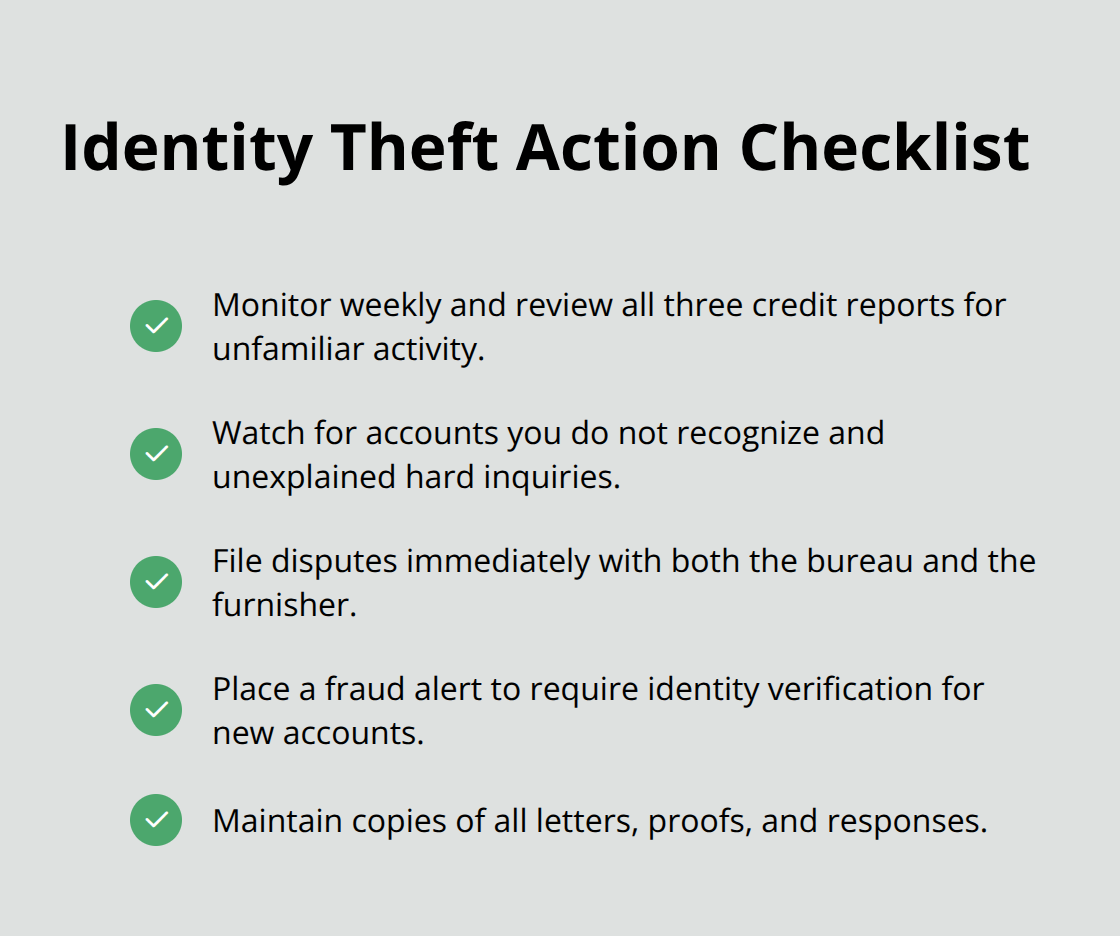

Identity theft protection gains concrete power under these changes because credit header data becomes harder to sell, reducing the volume of unauthorized data flowing through third-party networks. Monitor your credit reports monthly using the free weekly disclosures available from Equifax, Experian, and TransUnion, watching for accounts you don’t recognize or inquiries from lenders you never contacted. If unauthorized accounts appear, file disputes immediately and consider placing a fraud alert with the credit bureaus, which forces creditors to verify your identity before opening new accounts.

The 30-day investigation requirement now applies to identity-theft disputes the same as other inaccuracies, giving you a formal mechanism to force removal of fraudulent items.

Final Thoughts

The FCRA rights updates rolling out through 2025 fundamentally reshape how your credit information flows through the system. Medical debt no longer appears on most credit reports as of March 17, 2025, data brokers face tighter transparency requirements, and furnishers must investigate disputes more thoroughly when systemic errors emerge. These changes work in your favor if you understand how to use them.

Start by pulling your credit reports from all three bureaus using your free annual access or the free weekly disclosures available from Equifax, Experian, and TransUnion. Look specifically for medical accounts that should have been removed under the March 2025 prohibition, inaccurate amounts, accounts that don’t belong to you, or inquiries from lenders you never contacted. Document everything you find and file written disputes with both the credit bureau and the furnisher simultaneously, keeping copies of all correspondence.

If disputes stall, inaccurate information persists, or you discover identity theft, you have the right to sue for violations and recover damages. Companies take FCRA violations seriously because the financial consequences motivate settlement. Contact us for a free case review to discuss your situation and learn what recovery options apply to your circumstances.