Identity theft defense in California requires swift action and knowledge of your rights. Criminals are targeting California residents at an alarming rate, and the consequences can devastate your finances and credit for years.

We at Bontrager Law have helped countless victims navigate recovery and reclaim their financial security. This guide walks you through the immediate steps to take, your legal protections, and how to rebuild what was stolen.

How Criminals Steal Your Identity in California

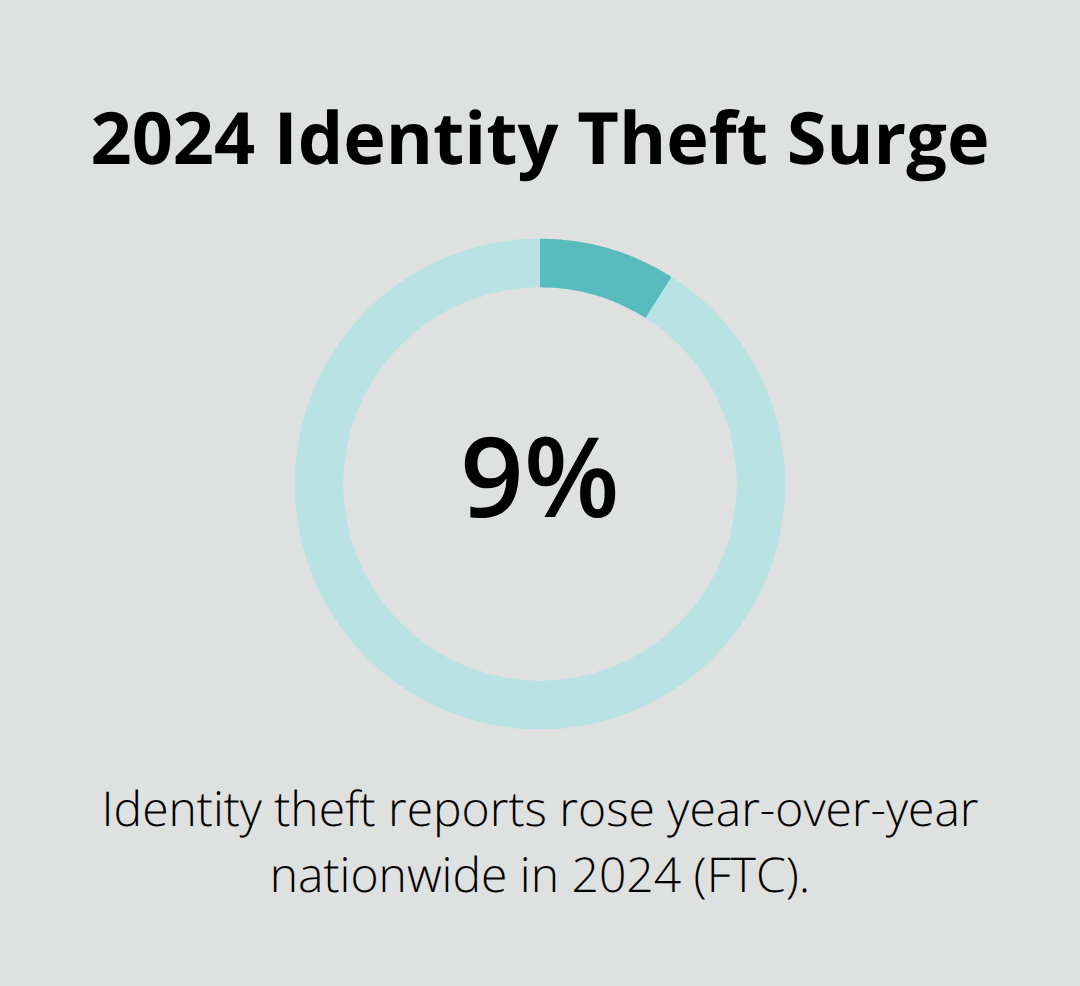

Data breaches remain the primary threat to California residents. In 2024, identity theft reports jumped 9% year-over-year nationwide according to FTC data, with large public breaches exposing nearly 3 billion records. Phishing emails trick you into revealing Social Security numbers and banking credentials by impersonating legitimate companies.

Formjacking-injecting malicious code into payment websites-captures your financial information during checkout. Thieves also obtain personal data through physical theft of mail, wallet documents, or trash containing financial statements. Synthetic identity fraud, where criminals blend real and fake information to open accounts, has accelerated as AI tools make deepfakes and stolen credentials easier to weaponize. The FTC’s IdentityTheft.gov resource logs over 1.1 million reports annually, but many victims don’t realize they’ve been compromised for months.

Spotting the Red Flags Early

Unexplained withdrawals from your bank account should trigger immediate investigation. Credit card statements for accounts you never opened signal active fraud. Debt collectors calling about debts you don’t recognize indicate someone used your identity to borrow money. Being denied credit due to unknown accounts or inquiries in your name reveals unauthorized activity on your credit file. Unfamiliar charges appearing on your credit report demand immediate disputes with creditors. These warning signs often appear weeks or months after the initial theft, which is why regular credit monitoring matters. Check your credit reports from all three bureaus-Equifax, Experian, and TransUnion-at least every four months by rotating through AnnualCreditReport.com. The faster you detect fraudulent accounts, the faster you can stop additional damage and begin recovery. California residents who catch identity theft early report significantly lower financial losses compared to those who discover it after months of unauthorized activity.

The Real Cost to Your Wallet and Future

Identity theft victims face drained bank accounts, ruined credit scores, and mounting debt they never incurred. The emotional toll includes anxiety, depression, and destroyed trust in financial institutions. Beyond immediate financial loss, compromised credit affects your ability to secure mortgages, auto loans, and favorable interest rates for years. Medical identity theft can create healthcare debt and insurance claim denials tied to fraudulent treatment. Criminal identity theft-where someone commits crimes in your name-creates arrest records and legal complications that require police reports and court intervention to clear. Recovery costs include credit monitoring services, legal representation, and time off work to dispute fraudulent accounts.

Understanding these theft methods and their consequences prepares you to act decisively when warning signs appear. The next section outlines the immediate steps you must take the moment you suspect identity theft has occurred.

Steps to Take Immediately After Discovering Identity Theft

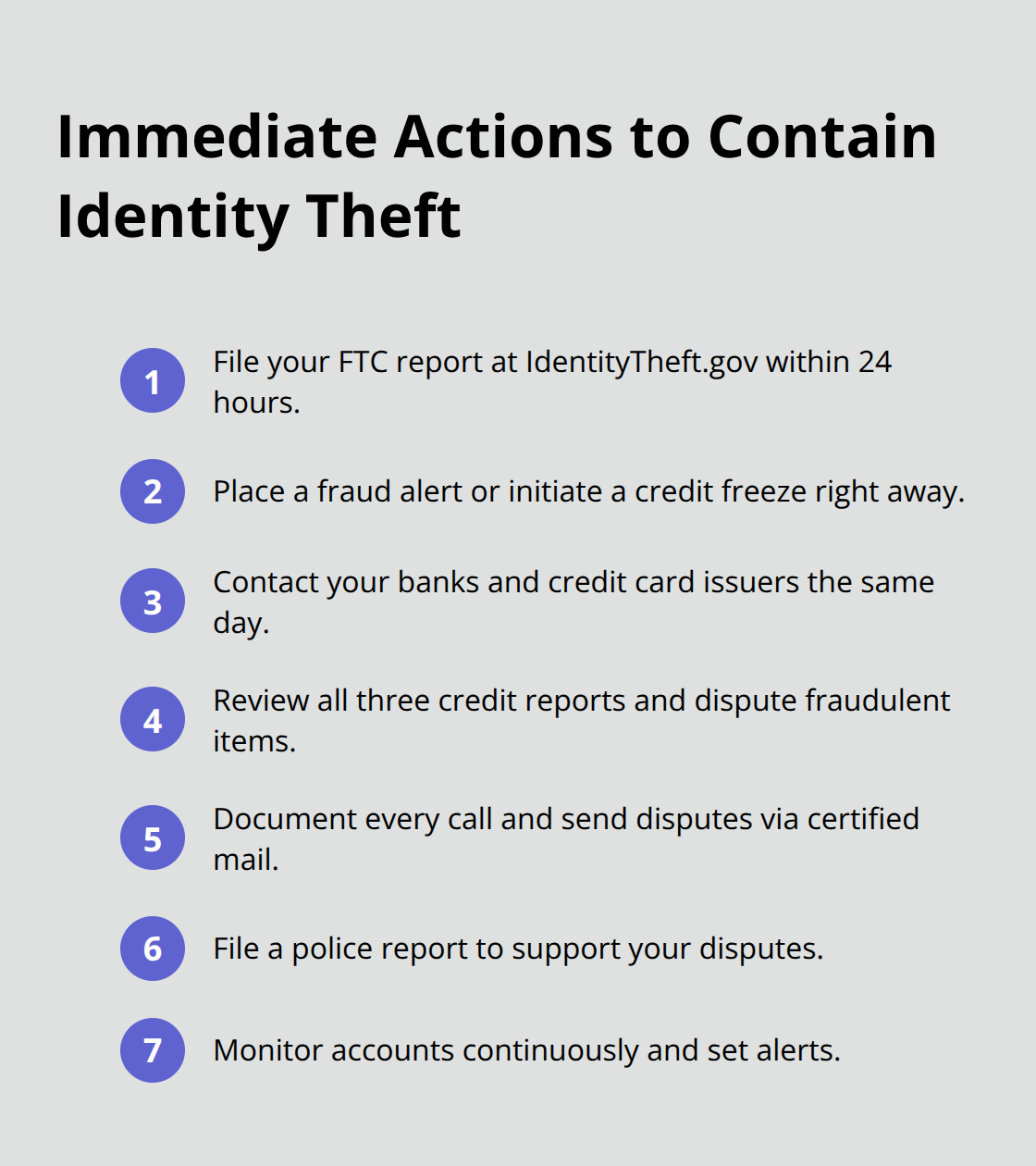

File a Report with the Federal Trade Commission Within 24 Hours

The window between detecting identity theft and preventing further damage is brutally narrow. Within the first 24 hours, you must file a report with the Federal Trade Commission at IdentityTheft.gov. This report creates an official record that creditors must recognize under federal law, giving you standing to dispute fraudulent accounts and demand removal from your credit file. The FTC report establishes your victim status and protects you from liability for unauthorized charges made after you filed.

Place a Fraud Alert or Credit Freeze Immediately

Contact all three credit bureaus-Equifax, Experian, and TransUnion-to place a fraud alert on the same day you file your FTC report. You only need to contact one bureau; they are required to notify the other two within 24 hours. A fraud alert lasts one year and tells lenders to verify your identity before opening new accounts, blocking most immediate account creation. If you want stronger protection, request a credit freeze instead, which prevents any new accounts from being opened without your explicit authorization.

Freezes remain in place until you lift them, giving you control over when credit access resumes. Place your fraud alert or freeze before reviewing your credit reports, since inquiries from lenders trying to open accounts will stop immediately.

Contact Your Banks and Credit Card Companies the Same Day

Contact your bank and credit card companies on the same day you file your FTC report. Tell them specifically which accounts show fraudulent activity and request they cancel those cards, reverse unauthorized charges, and issue replacement cards with new account numbers. Most banks will reverse fraud within 10 business days if you report it promptly, but delays beyond 48 hours reduce your protection under the Electronic Funds Transfer Act. Ask each bank for written confirmation of the fraud claim, the date you reported it, and the case number assigned. Request they send you a copy of any fraudulent transactions and the account application if an unauthorized account was opened in your name.

Document Everything in Writing

Keep detailed records of every call you make-write down the date, time, name of the representative, and what was discussed. This paper trail becomes critical evidence if you later dispute charges or pursue legal action against creditors who ignored your fraud alert. Send dispute packets via certified mail, fax, or email rather than plain mail to minimize further identity theft risk. This documentation becomes essential when disputing the debt with creditors or pursuing claims under the Fair Credit Reporting Act and California Consumer Legal Remedies Act.

File a Police Report to Strengthen Your Position

File a police report if identity theft occurred, since many creditors require it before accepting your dispute claim. The police report doesn’t guarantee arrest or prosecution, but it establishes legal standing and signals to creditors that fraud is documented with law enforcement. California residents should know that placing fraud alerts and filing police reports are free-never pay anyone to perform these steps. Many identity theft victims waste money on restoration services or credit monitoring when the initial protective measures cost nothing and provide the foundation for recovery.

These immediate actions stop the bleeding and create the legal foundation you need. Once you’ve secured your accounts and filed your reports, you can move forward with disputing the fraudulent accounts themselves and understanding the laws that protect you.

Legal Rights and Recovery Options for California Victims

California Law Protects You Against Fraudulent Debt

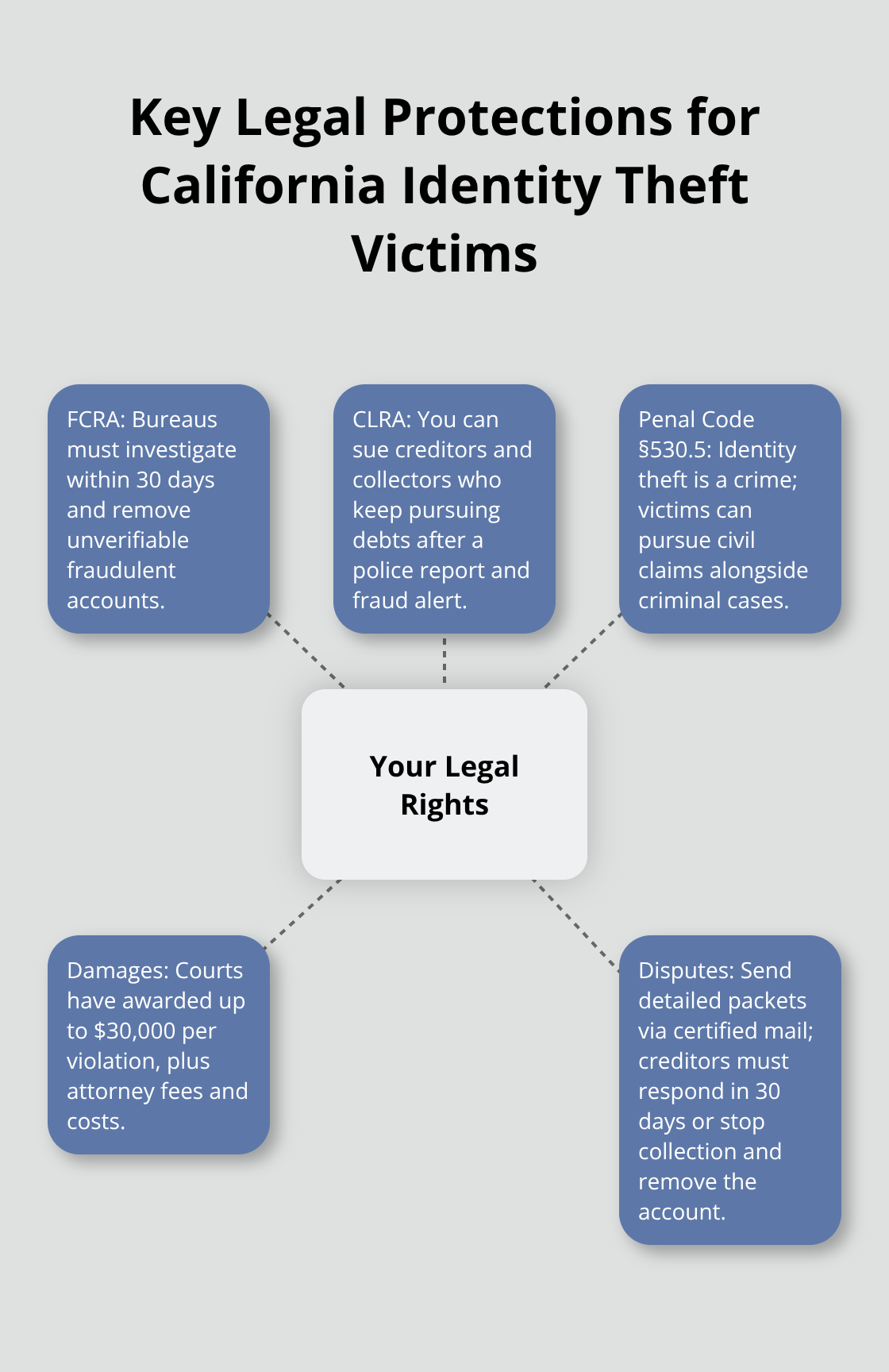

California law gives you powerful tools to fight identity theft and demand compensation from creditors who ignore your fraud alerts. The Fair Credit Reporting Act requires credit bureaus to investigate disputed items within 30 days and remove fraudulent accounts from your report if they cannot verify them. California’s Consumer Legal Remedies Act goes further, allowing you to sue creditors and debt collectors who continue pursuing debts after you’ve provided a police report and placed a fraud alert.

This means creditors cannot simply ignore your dispute and keep reporting the fraudulent account to damage your credit. Under California Penal Code section 530.5, identity theft is a crime, and victims can file civil claims separate from criminal prosecution.

Damages You Can Recover

The law allows you to recover actual damages including credit monitoring costs, time spent on recovery, and attorney fees. Courts have awarded up to $30,000 per violation in identity theft cases, and you can pursue multiple violations if a creditor repeatedly reports the same fraudulent debt or ignores your disputes. These damages reflect both your financial losses and the harm creditors caused by failing to respect your fraud alert and police report.

How to Dispute Fraudulent Accounts Effectively

Disputing fraudulent accounts requires sending detailed dispute packets via certified mail to each creditor and credit bureau showing the account is fraudulent. Include your police report, FTC Identity Theft Affidavit from IdentityTheft.gov, copies of your driver’s license and Social Security card to prove the account wasn’t opened by you, and documentation showing where fraudulent charges originated. Creditors must respond within 30 days under federal law, and if they cannot prove you authorized the account, they must remove it from your credit file and stop collection efforts. Many victims make the mistake of negotiating directly with creditors instead of sending formal dispute letters, which weakens their legal position significantly.

Report Fraud to Law Enforcement

Contact law enforcement through your local police department or the FBI’s Internet Crime Complaint Center if you suspect criminal identity theft or online fraud. Forward phishing emails to reportphishing@apwg.org to alert authorities about ongoing threats. California’s Attorney General provides free Identity Theft Information Sheets and resources through the state DOJ website, offering guidance tailored to California residents facing identity theft situations.

Get Professional Legal Help

A consumer protection attorney can handle these disputes, communicate with creditors on your behalf, and pursue settlement options for damages and legal fees if creditors violate your rights. Bontrager Law, a Los Angeles-based consumer protection firm with nearly 20 years of experience, represents California residents in identity theft disputes and offers a free case review to assess your situation and recovery options.

Final Thoughts

Identity theft defense in California starts with action, not panic. The steps outlined in this guide-filing your FTC report, placing fraud alerts, contacting your banks, and disputing fraudulent accounts-form the foundation of recovery. Speed matters because victims who act within the first 24 hours typically recover faster and suffer less financial damage than those who delay.

California gives you real legal weapons to fight back through the Fair Credit Reporting Act, California Consumer Legal Remedies Act, and state identity theft laws that allow you to demand creditors stop pursuing fraudulent debts and remove false accounts from your credit report. You can recover actual damages, attorney fees, and costs associated with your recovery, and California courts have awarded substantial damages to victims whose creditors ignored fraud alerts and continued damaging their credit. What many victims discover too late is that creditors often ignore fraud alerts unless you pursue formal legal action.

Bontrager Law represents California residents in identity theft disputes, handling creditor communications, pursuing settlements, and recovering damages on your behalf. With nearly 20 years of experience and thousands of claims resolved, we offer a free case review to assess your situation and recovery options. Contact us today to start your path toward restored credit.