A mistake on your credit report can tank your score and cost you thousands in higher interest rates. If you’ve spotted errors, notifying credit bureaus in California is your first step toward fixing them.

We at Bontrager Law help people challenge inaccurate credit reporting every day. This guide walks you through the process, your rights, and how to hold credit bureaus accountable.

How Credit Bureaus Collect and Report Your Information

Equifax, Experian, and TransUnion dominate credit reporting in California, and they operate on a simple but flawed system: creditors feed them data, and they package it into reports that lenders, landlords, and employers use to make decisions about you. These three bureaus don’t communicate with each other in real time, which means errors can sit undetected on one report while your other two reports remain clean. This fragmentation works in your favor when you dispute-you can catch and fix errors bureau by bureau rather than waiting for some mythical synchronized correction.

Where Your Information Comes From

The bureaus collect information from banks, credit card companies, utility providers, landlords, collection agencies, and court records. They track payment history, account balances, credit inquiries, public records like judgments and liens, and personal details like your name, address, and Social Security number. Not every creditor reports to all three bureaus, which is why your Experian report might show an account that doesn’t appear on your Equifax file. This inconsistency matters because a lender might pull only one or two reports and make decisions based on incomplete data.

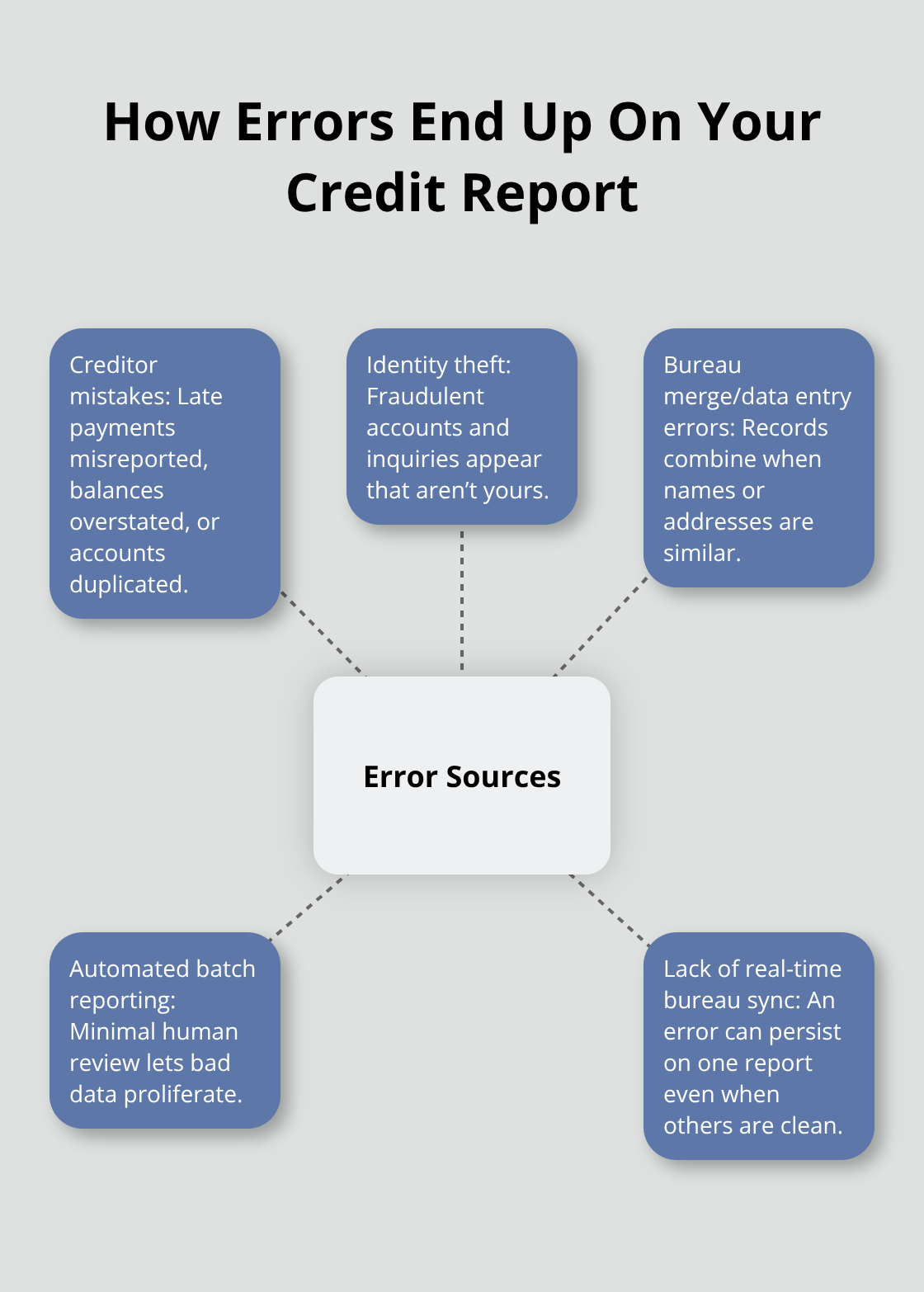

How Errors Land on Your Report

Errors appear on your report in three main ways. First, creditors submit incorrect information-a payment marked late when you paid on time, a balance reported higher than your actual amount, or an account listed twice under slightly different names. Second, identity theft introduces fraudulent accounts and inquiries that aren’t yours. Third, the bureaus themselves make mistakes during data entry or when merging records, especially if you share a name with someone else or have moved frequently.

The Fair Credit Reporting Act requires furnishers (creditors and collection agencies) to report accurate information, but enforcement remains inconsistent. Many creditors use automated systems that batch-report data with minimal human review, meaning errors can spread across thousands of consumer files. When you dispute an error with a bureau, that bureau contacts the furnisher to verify the information-but if the furnisher’s records are wrong in the first place, verification simply confirms the mistake.

Why These Errors Matter for Your Next Steps

Understanding how these errors originate prepares you to challenge them effectively. The bureaus’ reliance on furnisher data means your dispute strategy must address both the bureau and the source of the error. Your documentation and evidence will need to prove the furnisher reported inaccurate information, not just that the bureau made a clerical mistake. With this foundation, you’re ready to file your dispute and hold both parties accountable.

Steps to Notify Credit Bureaus of Errors

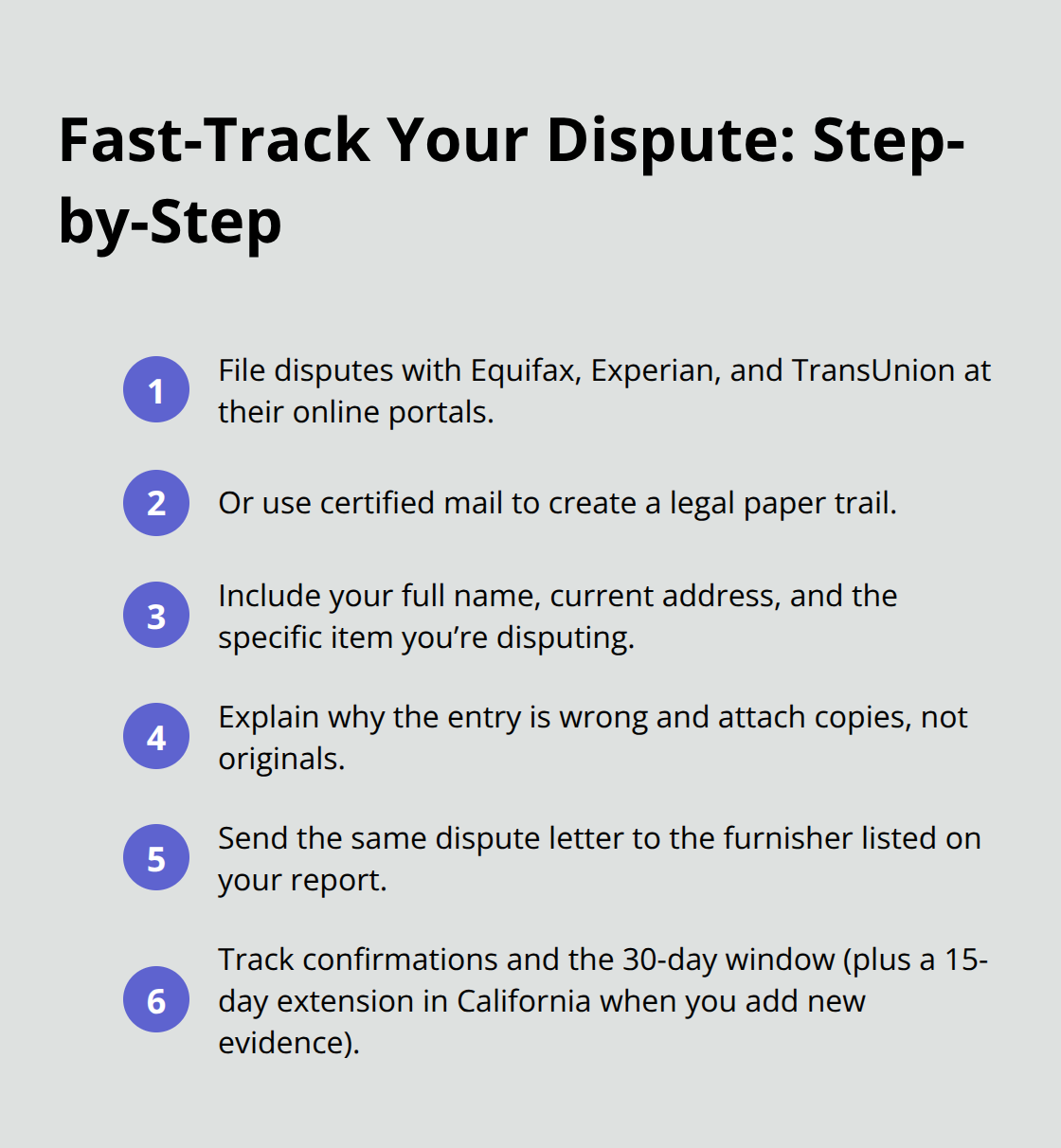

Filing a dispute with Equifax, Experian, and TransUnion takes roughly 15 minutes per bureau if you go online, though certified mail gives you a paper trail that protects you legally. We recommend filing with all three bureaus simultaneously rather than staggering them, because errors often appear across multiple reports and waiting weeks between disputes delays your credit recovery. Start by visiting each bureau’s dedicated dispute portal: Equifax.com, Experian.com, and TransUnion.com all have online dispute tools that process your claim faster than mail. If you prefer certified mail, address your letter to the dispute department listed on your credit report itself, include your name and current address, identify the specific account or item in dispute, explain why it’s wrong, and attach copies (never originals) of your supporting documents.

Send the same dispute letter to the furnisher-the creditor or collection agency that reported the error-using their address from your credit report. The Federal Fair Credit Reporting Act requires bureaus to investigate within 30 days, though California law allows a 15-day extension if you provide new documentation after filing.

Gather Your Evidence Before You File

Your supporting documents separate a successful dispute from one the bureau dismisses as frivolous. Create a spreadsheet listing each error you find, the account number, the bureau reporting it, and exactly what’s wrong. If a payment was marked late, pull your bank statements or canceled checks showing the payment cleared before the due date. If a balance is wrong, obtain your account statements from the creditor showing the accurate amount. For identity theft, collect a police report number, copies of fraudulent account statements, and any correspondence from the creditor confirming the account wasn’t yours. For duplicate accounts listed under slightly different names, collect statements showing the same account number or final balance. Organize these documents into a single folder before filing so you can attach them immediately. The bureau and furnisher will request verification from each other during their 30-day investigation window, and having your evidence front-loaded means the furnisher can’t claim they lack documentation to verify the error. Keep digital copies of everything you send, including confirmation numbers from online disputes and tracking numbers from certified mail.

Understand the Investigation Timeline

Once the bureau receives your dispute, they forward it to the furnisher within five business days and give the furnisher 30 days to respond. If the furnisher can’t verify the information or confirms it’s wrong, the bureau must correct or delete it from your report and send you a corrected copy at no charge. If the furnisher verifies the item is accurate, the bureau reports back to you with that result. California law requires the bureau to explain the outcome in writing, so you’ll receive a letter detailing whether the item was corrected, deleted, or verified as accurate. If the result frustrates you, you can request a re-investigation and submit new evidence within 15 days, which restarts the 30-day clock. Many disputes resolve on the first round if your evidence is clear, but complex cases involving multiple errors or furnisher resistance often require a second or third dispute cycle spanning two to three months total.

Know What Happens If Bureaus Ignore Your Dispute

The bureaus must respond to your dispute in writing within the legal timeframe. If they fail to investigate, fail to correct a verified error, or fail to send you a corrected report, you have grounds to file a complaint with the California Attorney General or the Federal Trade Commission. You can also pursue a lawsuit under the Fair Credit Reporting Act if the bureau’s negligence or willful noncompliance causes you harm. Document every step of your dispute process-keep all letters, confirmation numbers, and tracking receipts-because this documentation becomes your evidence if you need to escalate beyond the initial dispute. The bureaus know consumers have these legal protections, which is why most respond appropriately when you file a proper dispute with solid evidence.

Your Rights Under California and Federal Law

What the Fair Credit Reporting Act Guarantees

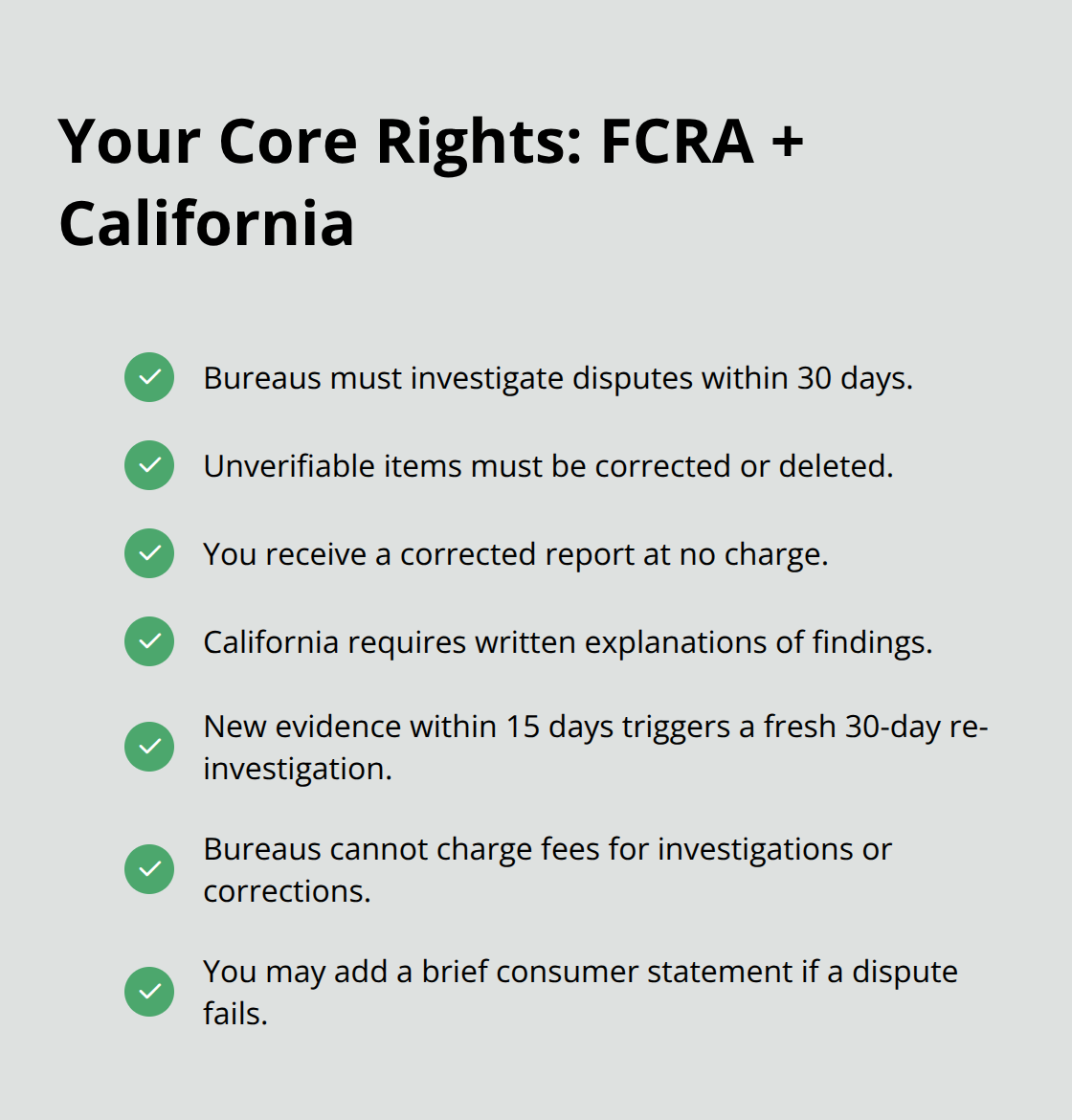

The Fair Credit Reporting Act sets a federal floor for your rights, but California stacks additional protections on top that give you real leverage in disputes. The FCRA requires credit bureaus to investigate your dispute within 30 days and correct or delete any information they cannot verify. If a furnisher cannot confirm the item is accurate, the bureau must remove it from your report entirely and send you a corrected copy at no charge. California’s Consumer Credit Reporting Agencies Act goes further by requiring bureaus to explain their investigation findings in writing and to delete unverifiable information promptly rather than leaving it on your file.

California’s Extra Layer of Protection

The state mandates that if you provide new evidence within 15 days of receiving a dispute result, the bureau must conduct a second investigation with a fresh 30-day window. This matters because many furnishers respond to initial disputes with vague verification claims, but a re-investigation with stronger documentation often forces them to admit they cannot verify the item. Under California law, bureaus cannot charge you for dispute investigations, corrected reports, or the removal of inaccurate data-fees for these services are illegal. The FCRA also allows you to add a brief consumer statement to your credit file explaining your position if a dispute fails, though this statement appears only on reports you request and not on reports sent to creditors or employers.

What to Do When Bureaus Fail to Comply

If a bureau ignores your dispute, fails to investigate within the required timeframe, or refuses to correct verified errors, California and federal law give you a path forward. You can file a complaint with the California Attorney General’s office or the Federal Trade Commission, both of which investigate violations and can pursue enforcement actions against the bureau. More importantly, you have the right to sue under the FCRA for damages if the bureau’s conduct is negligent or willful, and California courts have awarded consumers thousands in statutory damages plus attorney fees when bureaus fail to follow the law.

Building Your Documentation Trail

Document everything from day one-keep copies of your dispute letters, certification receipts, confirmation numbers from online disputes, and all correspondence from bureaus and furnishers. This documentation becomes your evidence if escalation becomes necessary. The paper trail you create protects you legally and strengthens any claim you might file later. Courts and regulators rely on this documentation to determine whether a bureau violated the law, so treat every receipt and confirmation number as part of your case file.

When to Seek Legal Guidance

Bontrager Law handles credit reporting violations across California and can evaluate whether a bureau’s failure to investigate or correct errors rises to the level of a lawsuit. Many consumers discover they have legal claims only after consulting with someone who understands both the FCRA and California’s stricter requirements, which is why a free case review often reveals options you would not find on your own.

Final Thoughts

You now understand how to notify credit bureaus in California, what documentation strengthens your case, and which laws protect your rights. The dispute process itself is straightforward: file with all three bureaus simultaneously, attach supporting evidence, send a separate letter to the furnisher, and wait for the 30-day investigation window to close. Most errors resolve on the first round when your documentation is solid.

Monitor your credit reports for the bureau’s response and track your timeline carefully after you file. Prepare for a potential second dispute if the first round doesn’t fully resolve your issues, and keep every receipt, confirmation number, and piece of correspondence because this documentation becomes your evidence if you need to pursue legal action. Many consumers find that simply filing a proper dispute with strong evidence forces bureaus and furnishers to correct errors without further escalation.

If you’ve filed disputes and the bureaus still refuse to correct clear errors, or if you suspect the bureau violated the law through negligence or willful noncompliance, you may have a legal claim worth pursuing. Bontrager Law handles credit reporting violations across California and can evaluate whether your situation warrants a lawsuit. Contact us to discuss your dispute and learn whether you have grounds for legal action against the bureaus or furnishers responsible for the errors damaging your credit.