A single error on your credit report can cost you thousands in higher interest rates. At Bontrager Law, we’ve helped countless Californians conduct a thorough California credit report review and challenge inaccurate information that was dragging down their scores.

The good news: you have legal rights to dispute these mistakes, and the process is straightforward. This guide walks you through exactly how to identify errors, file disputes, and rebuild your credit.

Getting Your Free Credit Reports and Spotting What’s Wrong

Federal law gives you the right to one free credit report every 12 months from each of the three major bureaus-Equifax, Experian, and TransUnion. Head to AnnualCreditReport.com, the official site directed by federal law. Avoid look-alike sites that promise free reports but charge fees or collect your data; they’re common traps. Request all three reports at once or stagger them throughout the year. We recommend getting all three simultaneously so you can compare them side by side and catch discrepancies that appear on one bureau’s report but not the others. The reports arrive within days, either online or by mail depending on your preference. Once you have them, print copies and set aside time to review each one thoroughly.

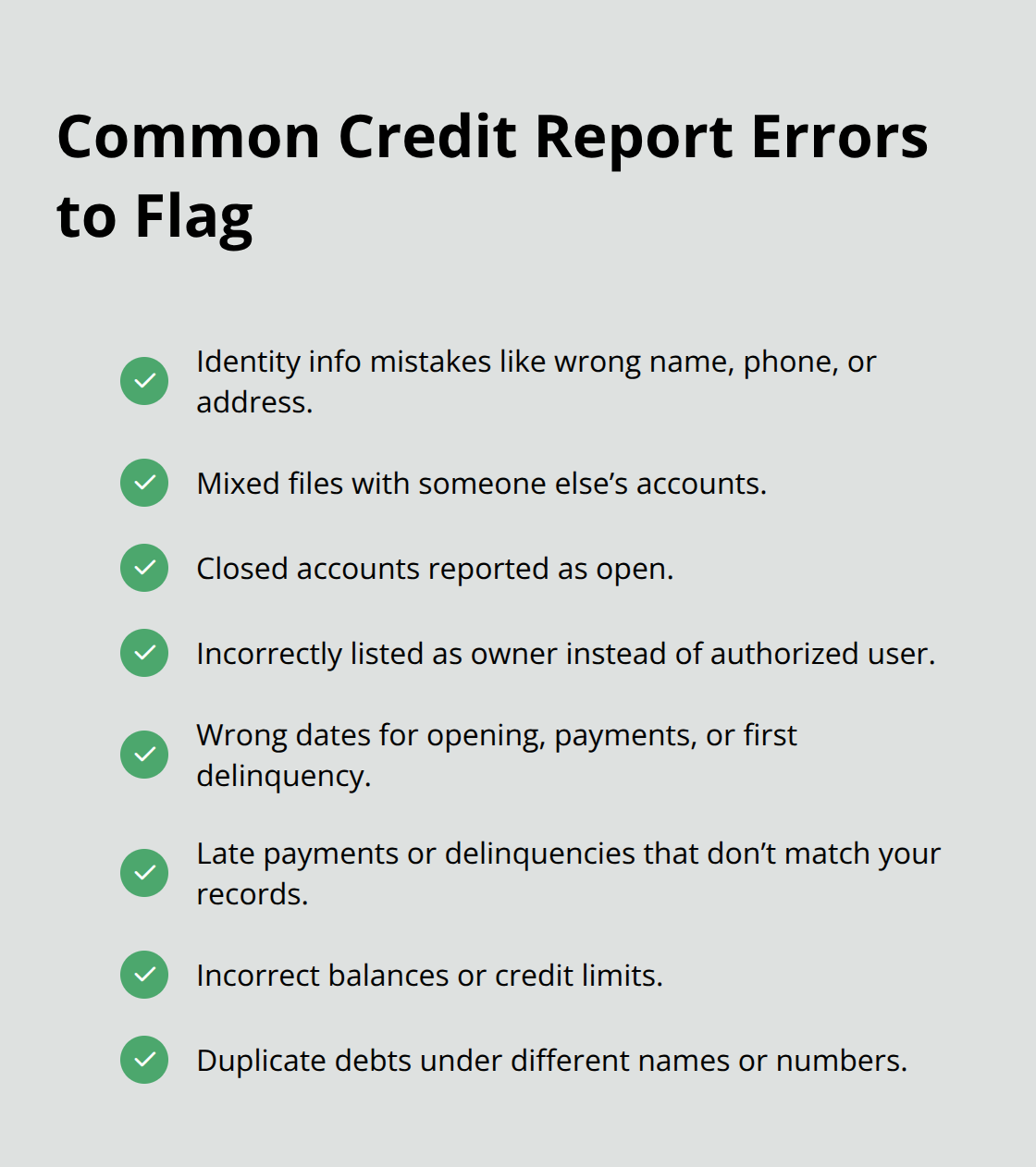

What errors actually look like on your report

Look for identity information mistakes first-wrong name, phone number, or address listed under your accounts. These errors create confusion and can hurt your score without you realizing it. Next, scan for mixed files where accounts belong to someone else with the same or similar name. This happens more often than people think and requires immediate attention. Check whether closed accounts still appear as open, which inflates your available credit and distorts your utilization ratio. Verify that you’re listed as the owner of accounts, not just an authorized user, since authorized user accounts shouldn’t affect your credit profile the same way. Examine dates carefully: the date opened, last payment date, and date of first delinquency should match your actual history. If you see late payments or delinquencies that don’t align with when you actually missed payments, that’s a reportable error. Check current balances and credit limits for accuracy; an incorrect limit can make your utilization appear worse than it actually is.

Duplicate debt entries-the same debt listed twice under different names or account numbers-appear surprisingly often and must be removed.

Document everything before you dispute

Create a spreadsheet listing each error you find, the account number, the bureau reporting it, and exactly what’s wrong. Gather supporting documents: bank statements, payment receipts, correspondence with creditors, and anything else proving the information is inaccurate. Take screenshots of the errors on your credit report with dates and times visible. This paper trail becomes critical if your dispute gets denied or if you need to escalate to the Consumer Financial Protection Bureau (CFPB). Write down which bureau reported each error and which creditor (the furnisher) provided the information to that bureau. You’ll need this information when you file disputes with both parties. Store copies of everything in a safe place-digital copies in a secure folder and physical copies in a file. The more documentation you have, the stronger your dispute case becomes.

Prepare for the next step

With your errors documented and your supporting materials organized, you’re ready to file formal disputes. The process involves contacting both the credit bureau that issued the report and the creditor who provided the inaccurate information. Each party has specific responsibilities under federal law, and understanding how to communicate with them makes the difference between a quick resolution and a prolonged battle.

How to File Disputes That Actually Get Results

Send a Written Dispute to the Credit Bureau

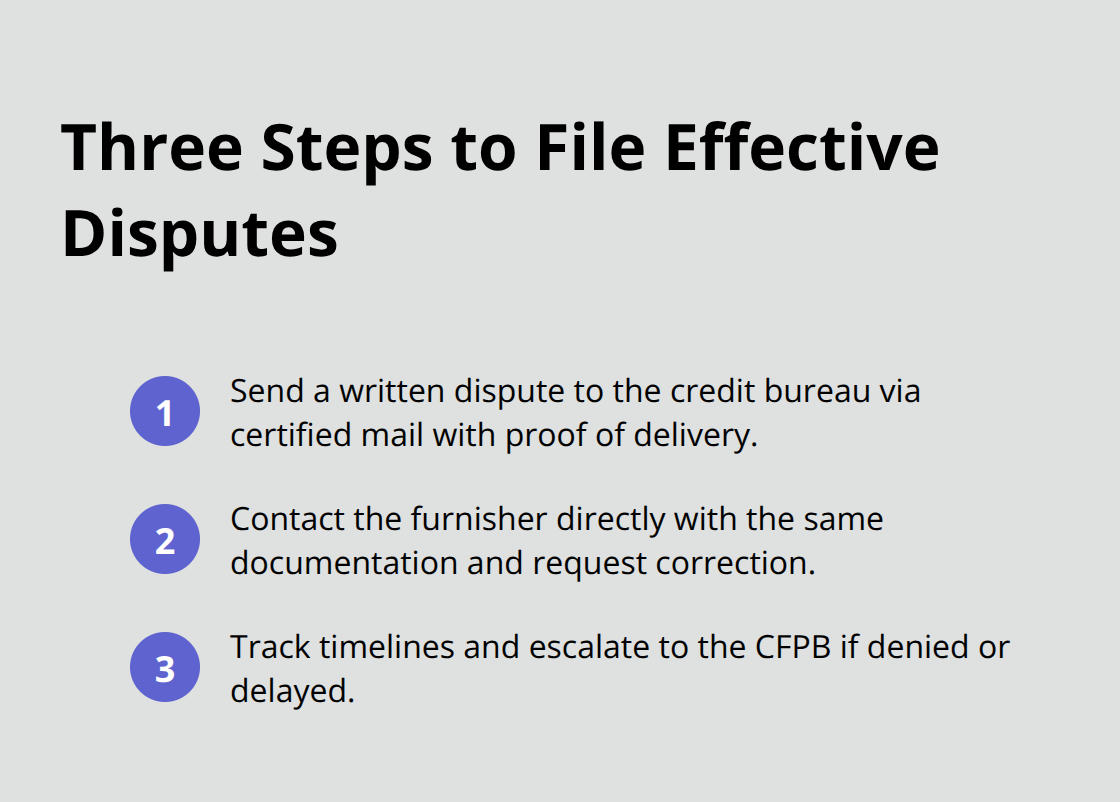

File your dispute with the credit bureau in writing. Mail your letter directly to the bureau that issued the report containing the error, using certified mail with return receipt so you have proof of delivery. This matters if the bureau later claims they never received your letter.

The Federal Fair Credit Reporting Act mandates that the bureau investigate your dispute within 30 business days and must contact the furnisher (the creditor who reported the information) to verify accuracy. Include your full name, address, phone number, and the confirmation number from your credit report if available. For each error, state the account number clearly, explain exactly what is wrong, and specify whether you want the item removed or corrected.

Attach copies (never originals) of your supporting documents: bank statements, payment receipts, correspondence with the creditor, or anything proving the information is inaccurate. The CFPB provides a sample dispute letter template you can adapt, which helps you hit all required elements. Mail your dispute letter to the specific address listed on your credit report for disputes-Equifax, Experian, and TransUnion each maintain different addresses, and using the correct one prevents delays.

Contact the Furnisher Directly

Simultaneously, send a separate dispute letter directly to the furnisher, the company that provided the false information to the bureau. This step matters because the furnisher must also investigate and correct inaccurate data they reported within 30 days under federal law. Address your letter to the disputes or compliance department, not a general customer service line.

Include the same documentation and state clearly what information is wrong and why. If the furnisher corrects or removes the information, they must notify all three bureaus so your reports get updated. This dual approach (contacting both the bureau and the furnisher) significantly increases your chances of resolution.

Track Your Disputes and Follow Up

Create a timeline spreadsheet noting the date you mailed each dispute, to whom, what you included, and when you expect a response. Keep copies of dispute letters, proof of mailing, all supporting documents, and any responses you receive. If 30 days pass and you hear nothing, send a follow-up letter referencing your first dispute and requesting a status update.

If either the bureau or furnisher denies your dispute or claims it’s frivolous, you can file a complaint with the CFPB, which will investigate and assign you a tracking number to monitor progress. The CFPB takes these complaints seriously and forwards them to the company for response within 15 business days.

What Happens Next in Your Case

Once you file disputes with both the bureau and furnisher, the investigation process begins. The furnisher must review your claim and either correct the information, remove it entirely, or confirm it’s accurate. If they confirm accuracy, you can request that the bureaus include a dispute statement in your file for future reports-this statement appears whenever someone requests your credit report going forward.

The bureau must update your credit reports once corrections occur, and you receive a copy of the updated file. If inaccuracies remain after the investigation, your next move involves understanding what options exist for further action and how to monitor your credit score as corrections take effect.

Rebuilding Your Credit After Dispute Corrections

Once the credit bureaus and furnishers update your reports with corrections, your score won’t jump overnight. Credit scoring models from Equifax, Experian, and TransUnion take time to recalculate, typically 30 to 45 days after corrections post. During this window, check your credit reports monthly to confirm that disputed items were actually removed or corrected. Some bureaus take longer than others to reflect changes across all three reports, so don’t assume one updated report means all three have been fixed.

Track Progress Over Three Months

Pull fresh reports from AnnualCreditReport.com every 30 days for the next 90 days to track progress. Your score may rise by 10 to 100 points depending on how severe the errors were and how prominently they featured in your credit profile. A removed collection account or corrected late payment typically produces faster improvement than fixing identity information errors. The Federal Fair Credit Reporting Act allows most negative information to remain on your report for seven years, and bankruptcy for ten years, so corrected accounts still appear as paid late or settled, not erased from history.

Build Positive Credit Activity Immediately

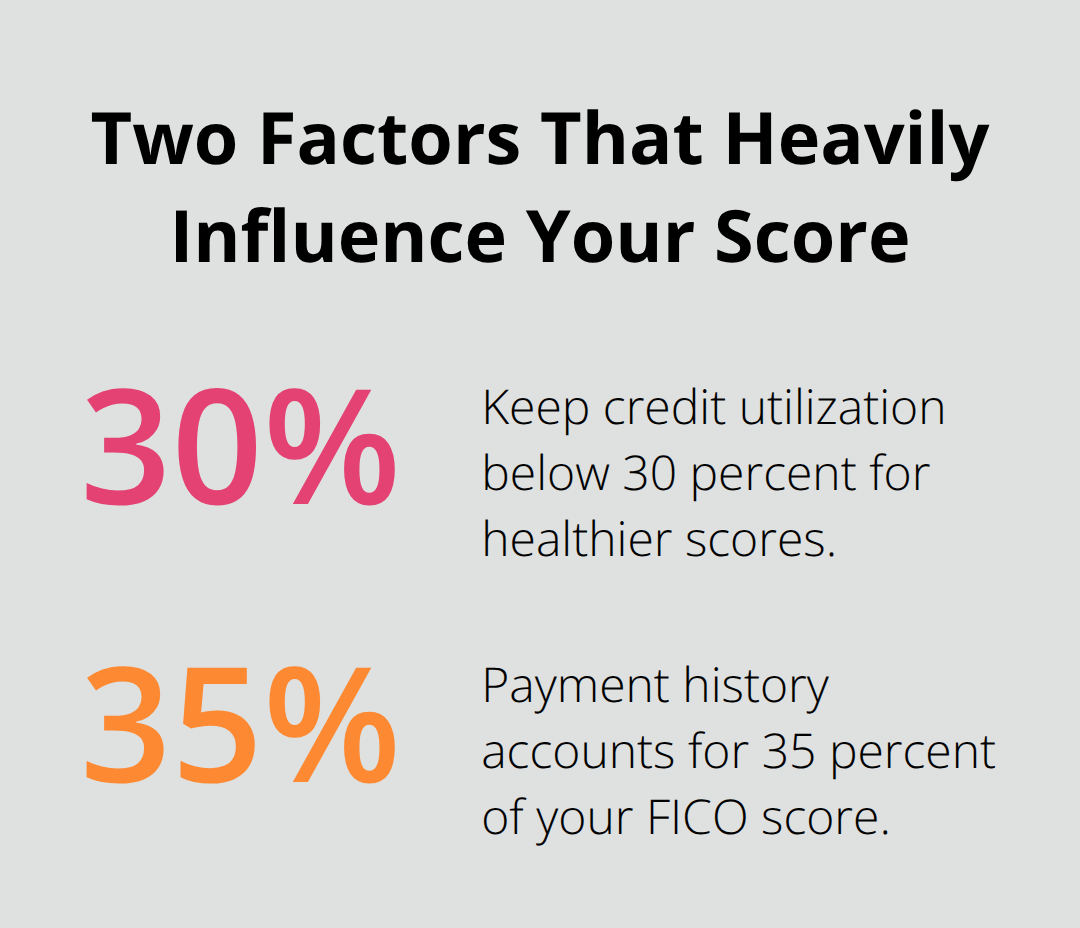

Removed negative items create space for positive credit activity to move your score higher. If your credit utilization ratio was distorted by incorrect credit limits, you now have accurate information to work with, which immediately improves your score if you keep balances low. Start using your credit cards for small purchases you pay off monthly, keeping utilization below 30 percent. Secured credit cards work well if traditional approval is difficult, requiring only a deposit while you rebuild.

Prioritize On-Time Payments

Make every payment on time moving forward, since payment history represents 35 percent of your credit score according to FICO’s scoring model. What matters is that inaccuracies are gone and your actual payment behavior going forward demonstrates responsibility. This consistent pattern of timely payments becomes your strongest tool for score recovery.

Address Remaining Negative Items

If you have accounts in collections that weren’t errors, negotiate a pay-for-delete agreement with the collector where they remove the account entirely once you pay (though this requires written agreement and isn’t guaranteed). Negative items that remain legitimate on your report will gradually age out and impact your score less significantly as years pass, so patience combined with positive action accelerates recovery.

Final Thoughts

California law protects your right to challenge credit reporting errors through California Civil Code § 1785.15 and the Federal Fair Credit Reporting Act. Credit bureaus must investigate your disputes within 30 business days and remove false data, while you retain the power to place security freezes, obtain your credit score, and see who accessed your report. A California credit report review puts you in control of your financial future and demonstrates that you can navigate this process successfully.

Once you identify inaccuracies, file disputes with both bureaus and furnishers, and watch your score recover, you’ve taken concrete action against companies responsible for reporting false information about you. If disputes become complicated, creditors ignore your letters, or the CFPB complaint process stalls, professional help can make the difference. Bontrager Law represents Californians in credit reporting disputes and has recovered millions for clients facing these exact situations.

Your credit report affects mortgage rates, job applications, apartment approvals, and major financial decisions-getting errors corrected matters enough to contact a professional if you need support. A free case review lets you understand your options without obligation, and the team provides personalized representation focused on results.