A credit dispute attorney in California can help you fight back against the errors that are costing you money and opportunities. Inaccurate entries on your credit report don’t just hurt your score-they can block you from loans, housing, and jobs.

At Bontrager Law, we handle these disputes directly with credit bureaus and creditors to get your record corrected. This guide walks you through your rights and how legal representation makes a real difference.

How Credit Reporting Errors Tank Your Financial Prospects

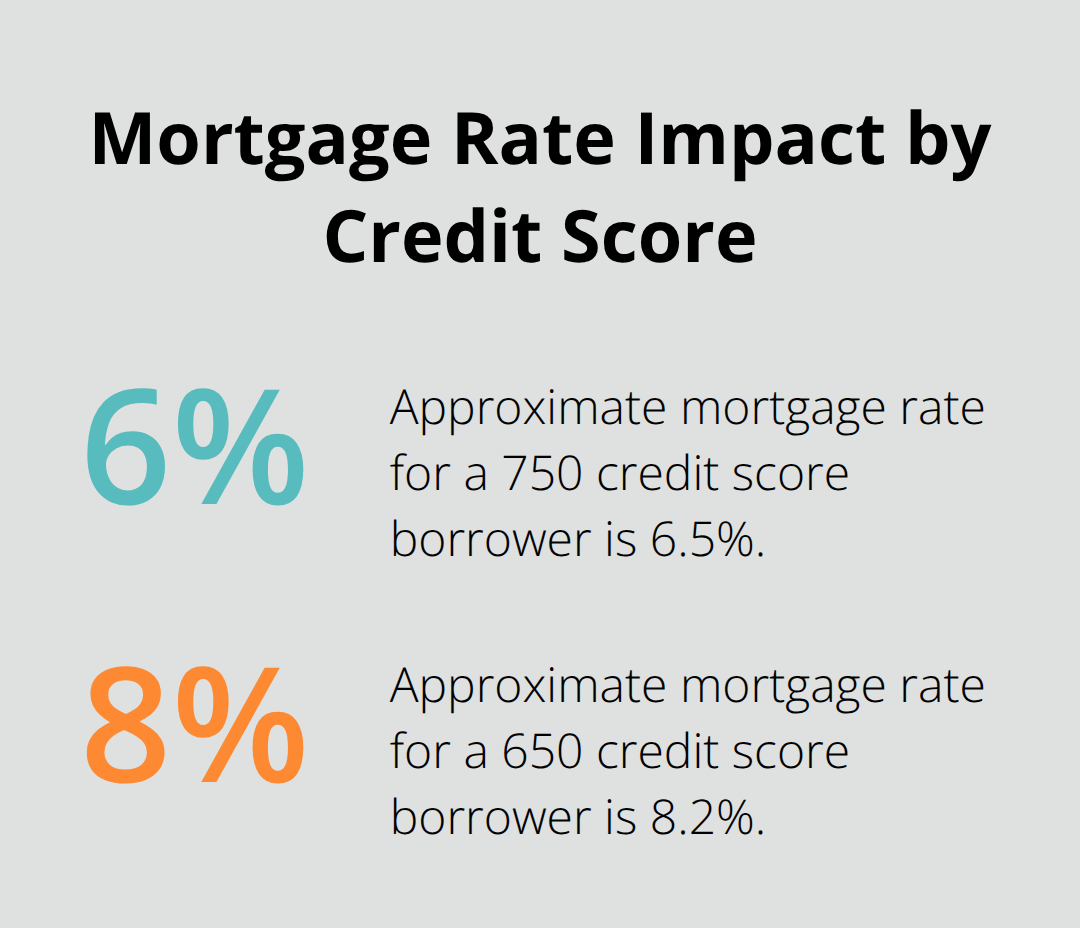

A single error on your credit report costs you thousands of dollars over time. If a collection account that isn’t yours appears on your file, your credit score drops 100 points or more, depending on your current score and history. That drop translates directly to higher interest rates on mortgages, auto loans, and credit cards. Someone with a 750 credit score qualifies for a mortgage at 6.5%, while someone with a 650 score pays 8.2%-a difference of nearly $200,000 in total interest over a 30-year loan. The Federal Trade Commission found that roughly one in five consumers identified an error on at least one of their three credit reports when they pulled them.

These aren’t small mistakes; they’re financial wounds that bleed money month after month. Inaccurate negative items remain on your report for seven years unless you actively challenge them, which means years of paying inflated rates or getting rejected outright for credit you need.

Employers and Landlords Access Your Credit File

Your credit report extends far beyond loans. Employers pull credit reports on job applicants, particularly for positions involving financial responsibility or security clearances. A damaged credit file costs you a job offer-not just a lower salary but the entire opportunity. Landlords routinely check credit reports before approving rental applications, and an error showing unpaid debt or a fraudulent collection account gets your application rejected immediately. Housing discrimination based on credit errors happens constantly; you never get a second chance to explain that the account doesn’t belong to you. Inaccurate information on your file creates barriers you can’t see coming until you’re denied.

Identity Theft Entries Multiply Your Problems

When someone steals your identity and opens fraudulent accounts, those accounts appear on your credit report as legitimate debt in your name. The damage compounds because each fraudulent account tanks your score, and creditors pursue you for money you never borrowed. California’s Identity Theft Act allows you to pursue damages for losses and emotional distress when this happens, but you must act fast and document everything. Fraudulent entries require more than a simple dispute-you need proof that the account wasn’t authorized (which means gathering police reports, affidavits, and correspondence with creditors). The longer fraudulent accounts sit on your report, the more damage they inflict on your financial standing and borrowing power. Getting these removed requires aggressive action, not passive hoping that the credit bureau notices the problem on its own.

Why You Need Legal Help to Fight Back

Credit bureaus process hundreds of millions of transactions daily, and errors slip through constantly. When you dispute an error on your own, credit bureaus often dismiss your claim or conduct inadequate investigations. The Fair Credit Reporting Act gives you the right to demand verification and correction, but bureaus frequently ignore these rights. A California credit dispute attorney knows how to pressure credit bureaus and creditors to take your dispute seriously. Bontrager Law handles these disputes directly with credit bureaus and creditors to get your record corrected, turning passive disputes into aggressive legal action that produces results.

What Are Your Federal Credit Rights

The Fair Credit Reporting Act handed you three powerful weapons to fight inaccurate entries on your credit report, but most people never use them. The Federal Trade Commission enforces these rights, and they exist specifically because credit bureaus fail to police themselves. You can dispute inaccurate information directly with the credit bureau, demand that they verify the debt within 30 days, and receive free annual credit reports from all three major agencies-Equifax, Experian, and TransUnion. These aren’t suggestions; they’re legal entitlements. The problem is that credit bureaus bank on your passivity. They process hundreds of millions of transactions daily, and errors vanish into the noise unless you force them to investigate. When you send a written dispute, the bureau must stop reporting the item while they verify it with the creditor or debt collector who supplied the information. If they can’t verify it within 30 days, they must remove it. That’s the law. Most bureaus conduct cursory investigations, contact the furnisher once, get a non-response or vague confirmation, and declare the account verified anyway. A dispute letter sent by certified mail with return receipt creates a paper trail that matters in court if the bureau ignores your rights.

Get Your Free Credit Reports and Spot Errors

You’re entitled to one free credit report annually from each of the three major bureaus through AnnualCreditReport.com, the federally authorized site. Most people never check their reports, which means errors compound for years before they realize the damage. A credit report runs 50 pages or longer, filled with personal data and detailed account information for every tradeline (account status, balance, payment history, dates, amounts). Scanning that much information takes time, but you must do it yourself because the bureaus won’t catch their own mistakes. Look specifically for accounts you don’t recognize, incorrect payment histories showing late payments you never made, wrong balances, duplicate entries, and accounts marked as unpaid when you paid them. Write to the bureau and the furnisher simultaneously with a clear, specific dispute letter identifying each inaccuracy and requesting removal or correction. Include copies of supporting documents-receipts, canceled checks, payment confirmations-that prove the item is wrong. Send everything by certified mail with return receipt requested so you have proof of delivery.

Demand Verification When Collectors Report Accounts

When a debt collector reports an account to your credit file, that account must be accurate and verifiable. If you dispute it, the collector must prove the debt exists and that you actually owe it. Collectors routinely report time-barred debts in California (accounts older than four years from the date of last payment on written agreements) knowing that many consumers won’t challenge them. You can demand verification in writing, and if the collector can’t produce legitimate documentation showing you borrowed the money and defaulted, the account should be removed. The Fair Debt Collection Practices Act requires validation notices within five days of first contact, stating the amount owed, the creditor’s name, and how to dispute in writing. If you don’t receive this notice, that’s a violation. Once you dispute in writing within 30 days, the collector must stop collection attempts until they verify the debt. Organize all your payments, receipts, letters, and call logs chronologically so you have everything ready if you need to prove you paid or that the debt belongs to someone else.

Know When Collectors Cross the Line

Collectors count on confusion and exhaustion to wear down consumers, but federal law sets clear boundaries on what they can do. They cannot harass you, make false threats, or contact you outside reasonable hours (typically 8 a.m. to 9 p.m.). You can request contact by mail or through an attorney, and you can ask them to stop contacting you entirely. If a collector violates these rules, you have grounds for legal action. A written dispute backed by documentation forces collectors to either verify legitimately or remove the account. When you understand these protections, you shift the power dynamic from passive victim to informed consumer who knows exactly what the law requires.

How We Challenge Credit Errors for You

Start With a Free Case Review

We at Bontrager Law begin every credit dispute case with a free case review where we examine your credit report, identify the specific errors, and assess what violations occurred. This initial conversation takes 20 to 30 minutes and costs you nothing. During this review, we pull your credit reports from all three bureaus and compare them against any documentation you have-payment records, creditor correspondence, collection notices, anything that proves the entry is wrong. We look for patterns that many consumers miss: accounts reporting the same debt twice under different collection agencies, items that should have aged off after seven years but remain on file, fraudulent accounts opened without your authorization, and time-barred debts that collectors are illegally reporting.

Identify Violations That Create Legal Leverage

We identify potential violations of the Fair Credit Reporting Act and the Fair Debt Collection Practices Act that give you legal leverage beyond simple disputes. If we see violations, we calculate what damages you may recover-actual damages for financial harm, statutory damages up to $1,000 per violation under the FCRA, and attorney fees that the law allows us to collect from the defendant. This matters because it shifts the negotiation from a passive dispute to a credible threat of litigation that credit bureaus and collectors take seriously.

Handle All Communication Directly

Once we take your case, we handle all communication with credit bureaus and furnishers directly, which immediately stops the back-and-forth that exhausts consumers. We send disputes by certified mail with return receipt to create the paper trail that courts require, and we include specific documentation that proves each error. When a bureau claims they investigated and verified the account, we demand they produce the actual verification-not a checkbox on a form, but legitimate documentation showing the account belongs to you and the balance is correct.

Force Verification or Removal

If bureaus cannot produce verification within 30 days, we file a lawsuit on your behalf seeking removal of the inaccurate entry and damages for their violation. Many cases settle before trial because bureaus and creditors know they cannot win when we have documentation proving the error and evidence of their inadequate investigation. We pursue actual damages for financial losses you suffered-higher interest rates paid, denied credit, lost housing or employment opportunities-plus statutory damages that the law provides. With nearly 20 years of experience handling thousands of claims and millions recovered for California consumers, we know exactly how much pressure to apply and when settlement becomes inevitable.

Final Thoughts

Inaccurate credit entries will not fix themselves, and credit bureaus will not voluntarily remove them. Waiting seven years for negative items to age off costs you thousands in higher interest rates and missed opportunities. A credit dispute attorney California can transform a passive dispute into aggressive legal action that produces real results, while handling this alone leaves you vulnerable to inadequate investigations and continued damage to your financial standing.

The difference between handling this yourself and working with legal representation comes down to leverage. When you send a dispute letter on your own, credit bureaus process it as routine paperwork and often conduct cursory reviews. When a California credit dispute attorney sends that same dispute backed by knowledge of violations and potential damages, bureaus take it seriously and respond accordingly. This shift in power dynamics changes everything about your outcome.

We at Bontrager Law handle credit disputes for California consumers with nearly 20 years of experience and millions recovered for clients. We start with a free case review where we identify the specific errors on your report and spot violations that create legal leverage. Contact us today and find out what legal options exist for your situation.