Your rental payment history shapes your credit score more than you might realize. Late payments, evictions, and reporting errors can damage your profile for years.

At Bontrager Law, we help renters get renters credit report help by identifying and fixing these problems. This guide walks you through disputing errors and rebuilding your financial standing.

How Rental History Shapes Your Credit

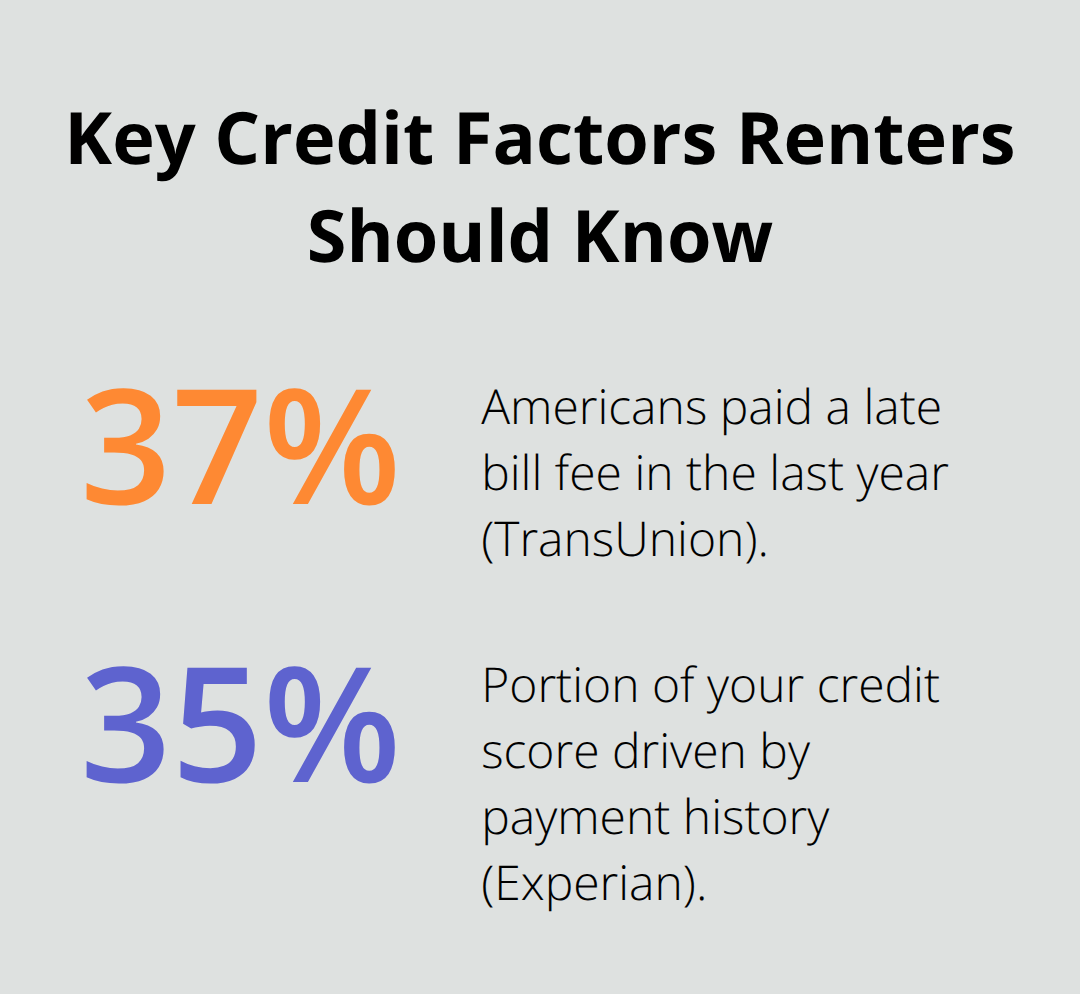

Your rental payment history is one of the most visible financial records a lender or landlord will examine about you. When you pay rent late or miss payments entirely, that information often flows into collections accounts, which then appear on your credit report and damage your score significantly. According to data from TransUnion, nearly 37% of Americans paid a late bill fee in the last year, which shows how common payment struggles are. If your landlord reports unpaid rent to a collections agency, that entry stays on your credit report for up to seven years from the delinquency date, making it extremely difficult to qualify for credit cards, loans, or even future rental housing.

The Damage Collections Accounts Inflict

A single collections account can drop your credit score by 100 points or more, depending on your starting score and overall credit profile. This damage is substantial and immediate. Addressing missed payments right away matters far more than hoping the issue resolves itself. The longer you wait, the more entrenched the negative mark becomes on your record.

When Evictions Create Long-Term Barriers

An eviction itself does not appear directly on your credit report, but the financial fallout from one absolutely does. If you were evicted due to nonpayment and that debt went to collections, the collections account will show up and harm your score for years. More broadly, eviction records appear in tenant screening reports and can remain visible for up to seven years, which means future landlords will see that you were previously evicted.

This creates a difficult cycle: you struggle to rent because of the eviction record, which limits your housing options and makes it harder to rebuild your financial stability. The cost to landlords of eviction ranges from about $1,000 to $5,000 or more depending on court costs and repairs (according to TransUnion data), which explains why landlords are extremely cautious about applicants with eviction histories. If you have an eviction on your record, prepare to explain it to future landlords and consider offering a larger security deposit or a cosigner to reduce their perceived risk.

Rent Payments as a Path Forward

The good news is that consistent, on-time rent payments can actively build your credit if your landlord reports them to the major credit bureaus. Payment history accounts for roughly 35% of your credit score according to Experian, making it the single most influential factor. If your landlord uses a rent-collection platform that reports payments to Equifax and TransUnion, every on-time payment strengthens your credit history and demonstrates financial responsibility to future lenders.

Automating your rent payments eliminates the risk of forgetting a due date and ensures that positive payment records accumulate month after month. Over time, a solid rental payment history can offset previous damage from late payments or collections, especially if those negative items are aging off your report. Your path forward depends on establishing new positive payment behavior now-not on erasing the past. Once you understand how your rental history affects your credit, the next step is identifying whether errors on your report are making your situation worse than it actually is.

Credit Report Errors That Hit Renters Hardest

Credit reporting errors are far more common than most renters realize, and they disproportionately damage your ability to secure housing or credit. The Fair Credit Reporting Act limits most negative information to seven years on your report, but errors can persist indefinitely if nobody catches and disputes them. According to the Consumer Financial Protection Bureau, inaccuracies on tenant background checks range from misidentified individuals to incomplete eviction outcomes and outdated records that should have been removed years ago. When a landlord pulls your report and sees incorrect payment information, fraudulent accounts, or records belonging to someone else entirely, they make rental decisions based on false data. This is why reviewing your actual credit report matters far more than guessing what might be on it.

You can pull your free annual credit reports from all three bureaus through AnnualCreditReport.com or by calling 1-877-322-8228.

Payment Data That Doesn’t Belong to You

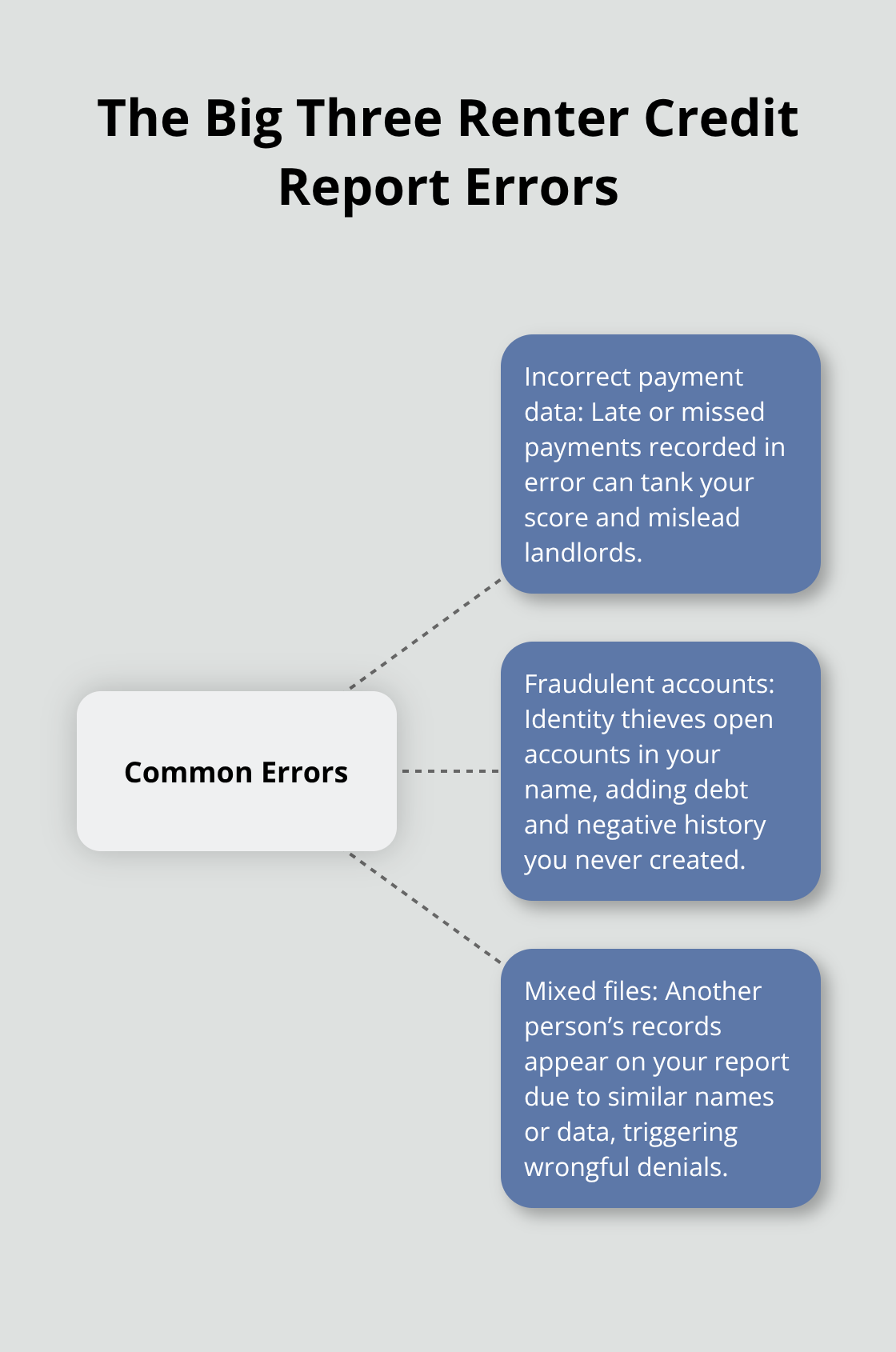

Incorrect payment information appears on renter reports constantly. A landlord’s clerical error, a collection agency’s data entry mistake, or a reporting lag can show a payment as late when you actually paid on time. Sometimes a payment gets recorded under the wrong account or the wrong tenant entirely, especially if you share a common name. If your report shows missed payments that you made, or if it lists accounts with payment statuses that don’t match your actual history, this directly tanks your score and gives landlords false reasons to reject your application.

Pull your report and cross-reference every tradeline against your actual payment records. If you automated rent payments through your bank, your bank statements serve as definitive proof of what actually happened. Document the correct payment dates and amounts, then contact the credit bureau and demand correction. The bureau must investigate within 30 days and provide written results.

Accounts That Aren’t Actually Yours

Fraudulent accounts opened in your name represent a more serious problem than simple data errors. Someone uses your Social Security number or personal information to open a credit account, and suddenly your report shows debt you never incurred. This tanks your credit utilization ratio, adds negative payment history if the fraudulent account falls behind, and creates immediate alarm for landlords reviewing your application.

Check every account listed on your credit report and verify that you actually opened each one. Pull your detailed credit report and look for the account number, opening date, and creditor name. Contact that creditor directly and ask them to verify who opened the account and provide documentation. If they cannot produce a legitimate signature or identification matching yours, request that they remove the account from your report. Then file a dispute with the credit bureau and consider filing an identity theft report with the Federal Trade Commission at IdentityTheft.gov.

Records Belonging to Someone Else

Credit bureaus sometimes mix up tenant records between individuals who share similar names, birthdates, or addresses. You might see an eviction, collections account, or criminal record on your report that actually belongs to another person entirely. This happens more often than it should, and it creates immediate rejection from landlords who see a false eviction history on your file.

Verify your personal information at the top of your credit report: full legal name, date of birth, current address, and Social Security number should all be exactly correct. If the report lists a previous address or alternate name that isn’t yours, flag that immediately. Then review every account, collection, and public record and confirm that each one is actually yours. If you find an account or record that belongs to someone else, contact the credit bureau in writing with supporting documentation (such as a copy of your ID or a statement showing your correct information). Request removal of the incorrect item and ask the bureau to correct any personal information that’s inaccurate. The bureau must investigate and respond within 30 days.

Once you identify errors on your report, the next step involves taking formal action to correct them. The dispute process itself is straightforward, but persistence and documentation determine whether you succeed in removing false information from your file.

How to Challenge Errors on Your Credit Report

Obtain and Review Your Credit Report Thoroughly

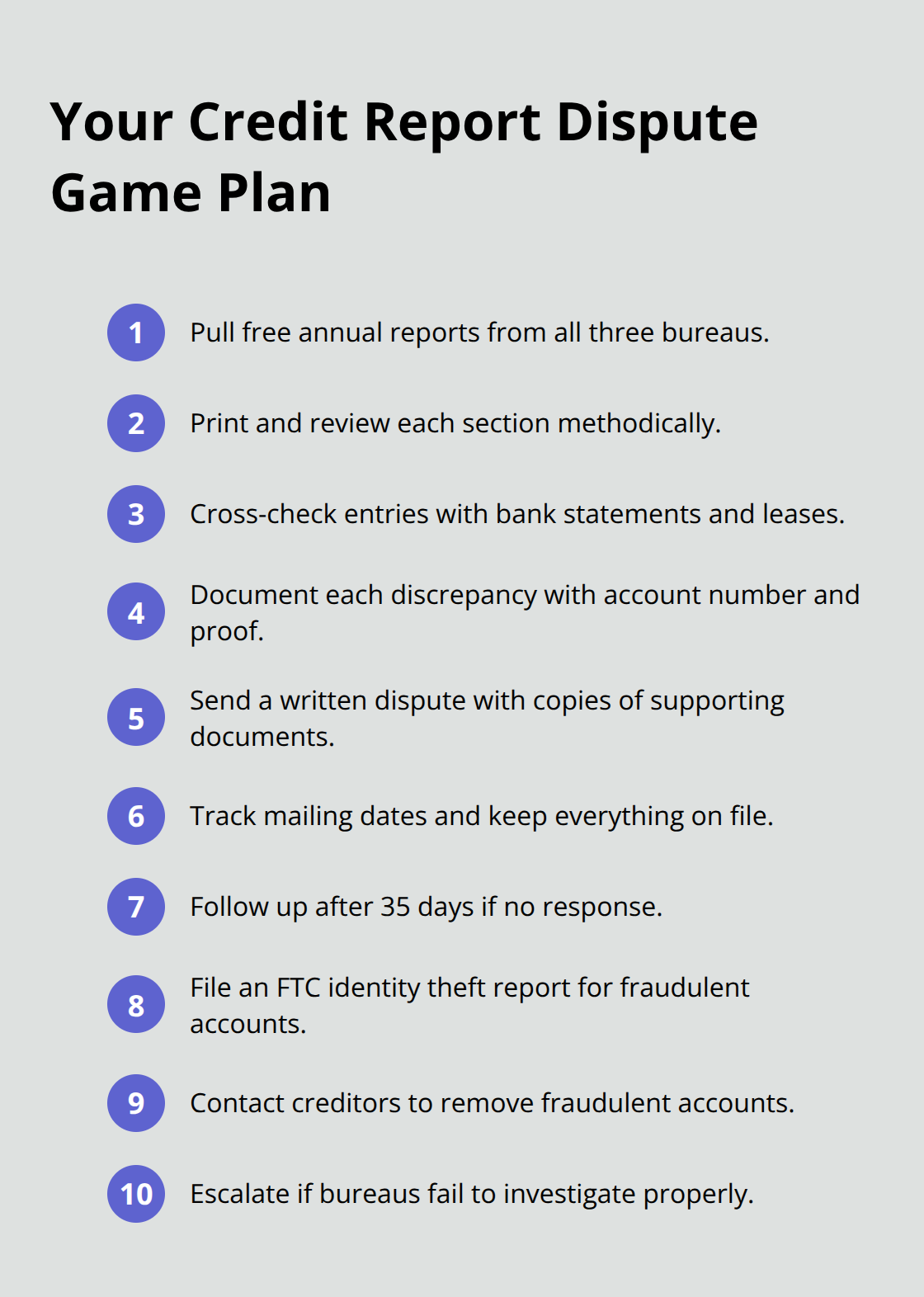

Start by pulling your free annual reports from all three bureaus at AnnualCreditReport.com or call 1-877-322-8228, then print them out and review each section methodically. The profile summary shows your total tradelines, public records, collections, and inquiries at a glance. The tradelines section lists every credit account with balances, credit limits, payment status, and delinquencies. The collections section shows debts referred to collectors with the collection agency name, debt type, balance, and status.

Check every single entry against your actual payment records, bank statements, and lease agreements. If you automated rent payments through your bank, pull those statements as proof of what you actually paid and when. Cross-reference dates obsessively because a payment recorded one day late when you paid on time is the kind of error that tanks your score and gives landlords false reasons to reject you.

Document Every Discrepancy with Precision

Write down every discrepancy with the account number, the error description, the correct information, and your supporting documentation. This takes time, but precision here determines whether the credit bureau takes your dispute seriously. Organize your evidence in a folder-physical or digital-so you can reference it quickly when you contact the bureau. The stronger your documentation, the faster the bureau investigates and corrects the error.

File a Written Dispute with the Credit Bureau

Contact the credit reporting agency in writing, not by phone. The Fair Credit Reporting Act mandates that bureaus investigate disputes within 30 days and provide written results, but only if you document your claim properly. Send a letter to the bureau’s dispute address (available on your credit report) and include copies of your supporting documents, a clear description of what’s wrong, and a statement of what the correct information should be.

Keep a copy of everything you send and track the mailing date. The bureau must respond in writing with the results of their investigation. If they find the information is inaccurate, they must correct or delete it and send you a corrected report.

Handle Fraudulent Accounts and Identity Theft

If you identify a fraudulent account, also file an identity theft report with the Federal Trade Commission at IdentityTheft.gov and keep that report number for your records. This creates an official record that protects you if the fraudulent account causes additional damage. Contact the creditor directly and demand that they remove the account from your report, then follow up with the credit bureau to confirm removal.

Follow Up and Persist Until Resolution

Follow up with the bureau 35 days after sending your dispute if you have not received a response. Send a second letter referencing your original dispute and the investigation deadline. Persistence matters because bureaus handle thousands of disputes monthly, and they sometimes miss deadlines or lose documentation. If the bureau refuses to correct an error or fails to investigate properly, you have legal options available. Document everything throughout this process because your paper trail is what proves you took action and that the bureau failed to correct legitimate errors.

Final Thoughts

Disputing credit reporting errors takes persistence, but the payoff justifies the effort. You now understand how to pull your reports, identify inaccuracies, and file formal disputes that force credit bureaus to investigate within 30 days. The Fair Credit Reporting Act gives you legal rights to challenge false information, and those rights exist specifically because errors happen constantly.

Your rights extend beyond credit bureaus themselves. If a landlord makes a rental decision based on inaccurate information, they must provide you with an adverse action notice that includes the reporting company’s contact details, allowing you to request a free copy of the report within 60 days and dispute any errors directly. The Federal Trade Commission and Consumer Financial Protection Bureau enforce these protections, and both agencies offer resources on their websites to guide you through disputes.

Renters credit report help is available through multiple channels-you can work independently by pulling your reports and filing disputes yourself at no cost, or you can contact local legal aid organizations if you need guidance. If credit reporting errors prevent you from securing housing or if a company refuses to correct legitimate inaccuracies, Bontrager Law represents renters across California in disputes over credit reporting errors and offers a free case review to evaluate your situation.