Your credit report shapes your financial future, yet many Californians don’t know their rights when errors appear or collectors cross the line. Credit reporting mistakes and illegal collection tactics happen more often than you’d think, and fighting back requires knowing exactly what protections California law gives you.

At Bontrager Law, we help residents navigate these challenges and reclaim their financial standing. This California credit rights blog walks you through your legal protections, common reporting errors, and the concrete steps to take action.

California’s Credit Protection Laws and How to Use Them

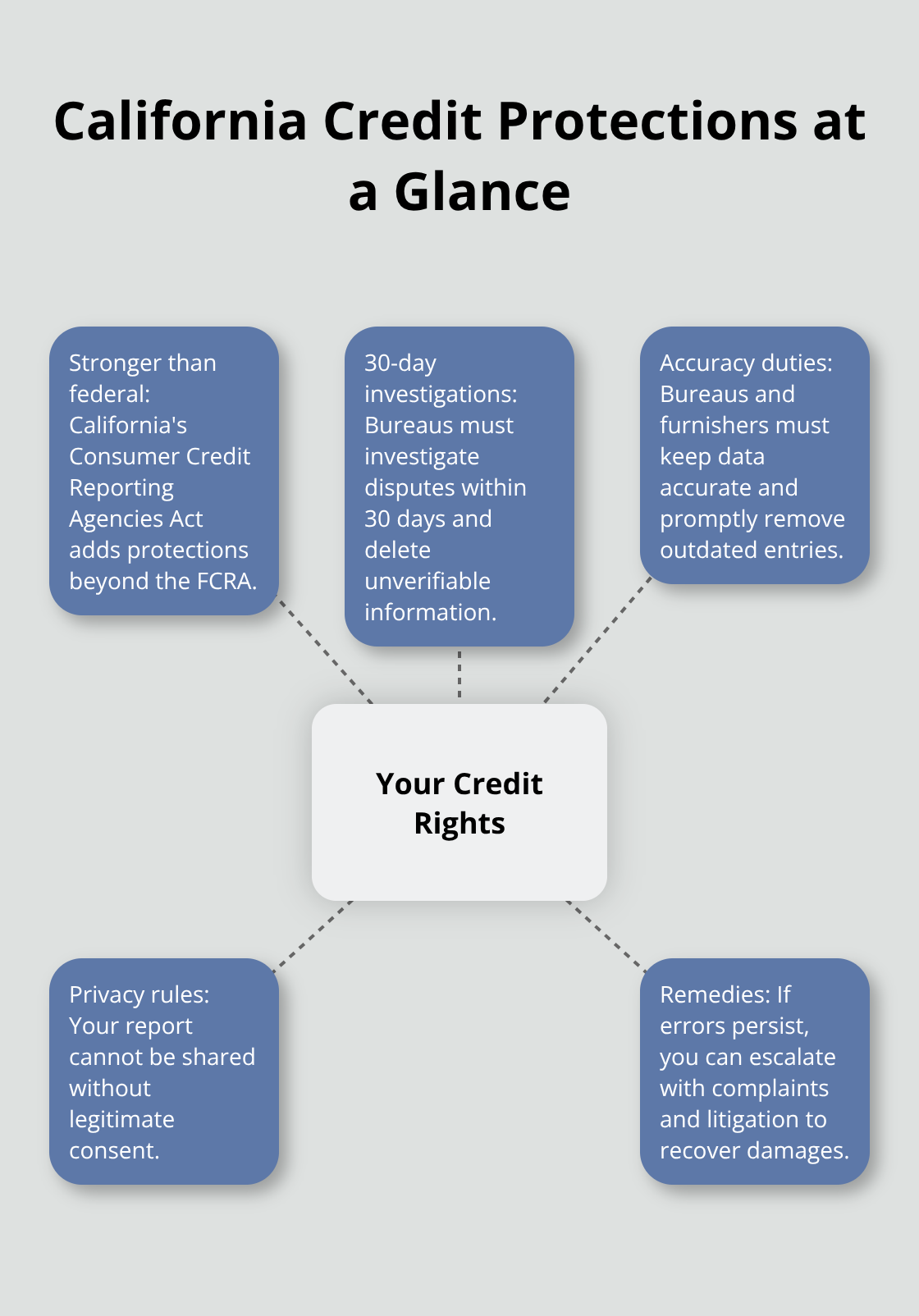

What Legal Protections Do California Credit Laws Give You

California’s credit protection framework gives you teeth to fight back against inaccurate reporting and unlawful collection practices. The Fair Credit Reporting Act sets federal baseline standards, but California goes further. The state’s Consumer Credit Reporting Agencies Act provides protections that exceed federal requirements, meaning you have more grounds to challenge errors and hold reporting entities accountable. Under these laws, credit bureaus and any entity that reports your credit data must keep information accurate, remove outdated entries promptly, and respect your privacy by not sharing your report without legitimate consent. When an error lands on your credit report-whether it’s a closed account showing as open, a late payment you actually made on time, or fraudulent accounts from identity theft-you have the explicit right to dispute it. The law requires credit bureaus to investigate disputes within 30 days and remove information that cannot be verified. This matters because inaccurate credit reports directly damage your borrowing costs. According to the CFPB, consumers with lower credit scores pay significantly higher interest rates on mortgages and auto loans. A single reporting error can cost you thousands in excess interest over the life of a loan.

How to Build a Dispute That Works

Most people send disputes to credit bureaus and assume the process will work. It won’t, not without documentation. When you dispute an error, include copies of proof (not originals) such as canceled checks, payment receipts, or bank statements showing you paid on time or that an account was closed. Send your dispute by certified mail and keep the receipt. The credit bureau must tell you in writing what they found, and if they cannot verify the information, they must remove it. If they refuse to remove inaccurate data, you have grounds for legal action under both federal and California law.

What Happens When Credit Bureaus Ignore Your Dispute

The California Attorney General’s Office handles complaints about credit reporting violations, and you can file complaints with the FTC and CFPB as well. Document everything: dates of disputes, names of people you spoke with, and outcomes. This documentation becomes critical if you eventually need legal representation to recover damages for willful violations or to force removal of false information from your report. Inaccurate information that persists on your credit report affects not only your loan rates but also your auto insurance costs and rental or housing decisions. The longer false data remains, the more financial damage accumulates. When credit bureaus fail to investigate your dispute properly or refuse to remove unverifiable information, you move from the administrative complaint phase into potential litigation territory.

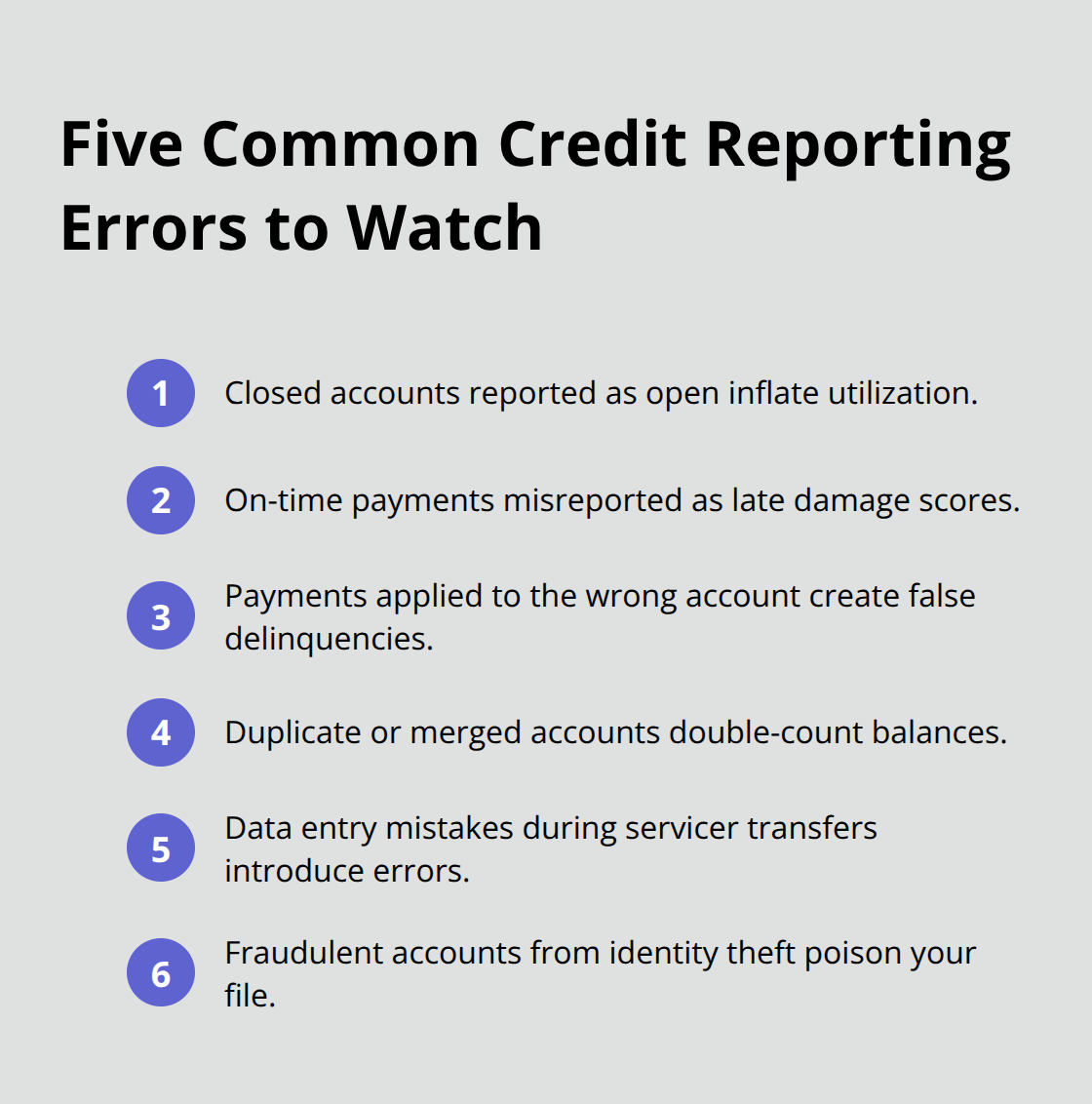

Common Credit Reporting Errors and How to Challenge Them

Closed Accounts That Still Show as Open

Closed accounts that remain listed as active rank among the most damaging reporting errors because they artificially inflate your credit utilization ratio. When a credit bureau reports a closed account as open, lenders see you carrying more debt than you actually owe, which tanks your credit score and makes borrowing more expensive. This happens frequently after you pay off accounts, transfer balances, or close cards intentionally. Credit bureaus sometimes fail to update account status when creditors report closures late or inconsistently.

If you closed an account and it still appears open on your report, pull your free annual credit reports from Equifax, Experian, and TransUnion at annualcreditreport.com and verify the status immediately. Document the account closure date from your own records-a final statement, email confirmation, or bank screenshot works. Then dispute the inaccuracy with the credit bureau by certified mail.

Incorrect Payment History and Late Payments

Incorrect payment history errors cut deeper because they suggest you missed payments you actually made on time. A single late payment can drop your credit score by 100 points or more, according to CFPB data, and stays on your report for seven years. These errors occur when creditors report payments to the wrong account, credit bureaus merge duplicate accounts, or data entry mistakes happen during transfers between servicers.

When you spot this error, do not call the credit bureau by phone. Disputes filed by phone lack documentation and bureaus frequently mishandle them. Instead, send a written dispute letter by certified mail that includes your account number, a description of the error, and copies of proof showing the correct information (such as canceled checks or bank statements).

Fraudulent Accounts from Identity Theft

Fraudulent accounts from identity theft represent the worst-case scenario: someone opens credit in your name, misses payments, and your credit report takes the hit while you discover the fraud months later. This error demands immediate action because the damage compounds daily as fraudulent accounts age on your report.

When you identify a fraudulent account, send a written dispute to the credit bureau immediately by certified mail. Request investigation and removal of the fraudulent account. The credit bureau has 30 days to investigate and respond. If they cannot verify the information, they must remove it.

What Happens When Credit Bureaus Refuse to Remove False Data

If a credit bureau refuses to remove inaccurate data despite your dispute, you have grounds to pursue legal action against both the credit bureau and the entity that reported the false information. Document everything: dates of disputes, names of people you spoke with, and outcomes. This documentation becomes critical if you eventually need legal representation to recover damages for willful violations or to force removal of false information from your report.

Inaccurate information that persists on your credit report affects not only your loan rates but also your auto insurance costs and rental or housing decisions. The longer false data remains, the more financial damage accumulates. When credit bureaus fail to investigate your dispute properly or refuse to remove unverifiable information, you move from the administrative complaint phase into potential litigation territory-and that’s where understanding your legal options becomes essential.

How Debt Collectors Break the Law and What You Can Do About It

The Rules Debt Collectors Must Follow

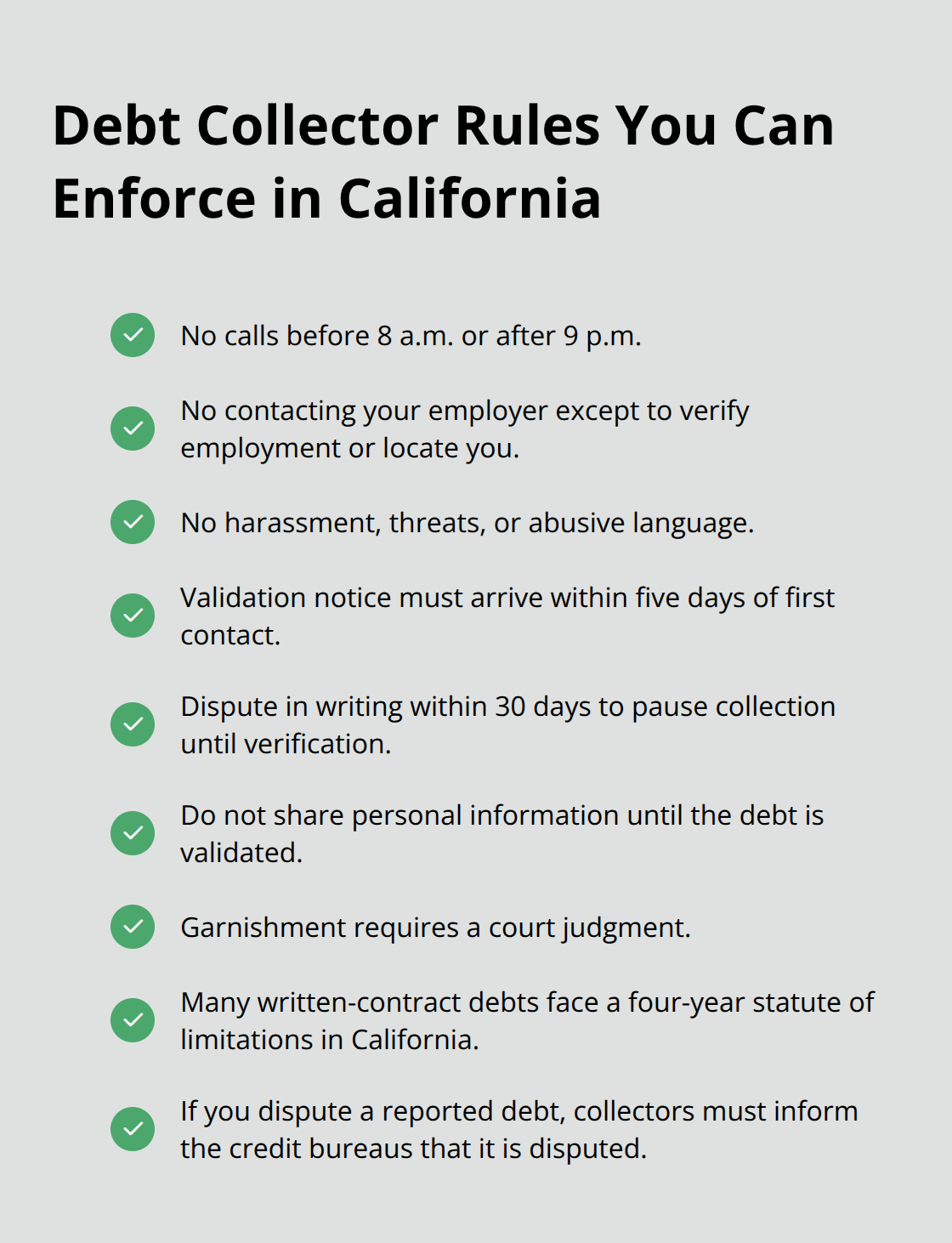

Debt collectors operate under strict federal and California rules, yet violations happen constantly because many collectors bet you won’t fight back. The Fair Debt Collection Practices Act sets baseline federal standards, but California law adds enforcement teeth through licensing requirements and the California Attorney General’s oversight. A debt collector cannot call before 8 a.m. or after 9 p.m., cannot contact your employer except to verify employment or obtain location information, and cannot harass you through repeated calls, threats, or abusive language. They must send you a written validation notice within five days of first contact showing the debt amount, the creditor’s name, and how to dispute the debt.

Why the Validation Notice Matters

This validation requirement matters because many collectors pursue debts that are time-barred, already paid, or incorrectly attributed to you. If you dispute the debt in writing within 30 days of receiving the validation notice, the collector must stop attempting to collect until they verify the debt. Send disputes by certified mail with return receipt requested and keep copies of everything. Do not share personal or financial information before receiving validation, as scams involving fake debt collectors are common.

Protecting Yourself from Wage and Account Garnishment

Wage and bank account garnishment only happen after a court judgment, and federal benefits like Social Security are generally protected from garnishment. In California, there is generally a four-year statute of limitations for filing a lawsuit on a debt based on a written agreement, though partial payments can restart the clock. If you receive a court summons, do not ignore it-responding is essential to avoid default judgment and possible garnishment. Collectors may report the debt to credit bureaus, and if you dispute, they must inform the bureaus that you dispute the debt.

Filing Complaints Against Violating Collectors

If a collector violates these rules, file a complaint with the California Attorney General’s Office, the FTC, or the CFPB, and document every violation with dates, times, names, and what was said. When collection violations occur, you have grounds for legal action to recover damages. Bontrager Law represents California residents in disputes with unlawful debt collectors and helps recover compensation for violations.

Final Thoughts

Start your recovery by collecting every document that proves reporting errors or collection violations occurred. Pull your credit reports from all three bureaus, gather bank statements and payment receipts, and document every contact from debt collectors with dates and details. This documentation forms your foundation for action and strengthens any complaint or legal claim you file.

Send a cease and desist letter to any collector violating the law, and file complaints with the California Attorney General’s Office, the FTC, and the CFPB when violations occur. These agencies track patterns and take enforcement action against repeat offenders, and your complaint contributes to holding bad actors accountable. When credit bureaus refuse to remove false information or collectors continue illegal tactics despite your efforts, legal action becomes necessary to recover damages and force removal of inaccurate data from your credit report.

We at Bontrager Law represent California residents across the state in credit reporting disputes, identity theft cases, and unlawful debt collection claims. Contact us for a free case review to discuss your situation and learn what damages you may recover. Your California credit rights matter, and you don’t have to navigate this alone.