Identity theft affects millions of Californians each year, and the financial and emotional toll can be devastating. Criminals are getting smarter about stealing personal information, which means you need someone who understands both the tactics they use and the laws that protect you.

We at Bontrager Law work with identity theft victims throughout California to recover damages and hold responsible parties accountable. If you’ve been targeted, knowing your legal rights and taking swift action makes all the difference.

How Criminals Steal Your Identity and What to Watch For

Data breaches remain the primary entry point for identity theft in California. The 2017 Equifax breach exposed 143 million Americans, and criminals continue to exploit similar vulnerabilities across retail, healthcare, and financial institutions. Beyond breaches, thieves inject malicious code into website payment forms-a tactic called formjacking-to harvest card details directly from unsuspecting shoppers. Mail theft poses equal danger; a stolen piece of mail containing a credit offer or tax document gives criminals everything they need to open accounts in your name. Phishing emails and texts that mimic legitimate companies trick you into revealing Social Security numbers, passwords, or account credentials. Public Wi-Fi networks become hunting grounds for criminals using packet-sniffing tools to intercept unencrypted data. Synthetic identity theft, where criminals blend real and fake information to create a new identity, is harder to detect but growing rapidly. The FTC reported over 1.1 million identity theft complaints in 2022, and that number continues to climb.

Watch for These Warning Signs Immediately

Unexpected bills, credit card statements you didn’t request, or collection calls about accounts you never opened signal fraud clearly. Check your credit reports from all three bureaus-Equifax, Experian, and TransUnion-at least once yearly through annualcreditreport.com to spot fraudulent accounts or suspicious inquiries before they damage your credit score. Hard inquiries from lenders you didn’t contact indicate that someone applied for credit in your name. A sudden drop in your credit score without explanation warrants immediate investigation. Missing mail or notices of address changes you didn’t authorize mean a thief may be redirecting your statements. Calls from debt collectors about debts you don’t recognize signal that someone has taken out loans or opened credit cards using your identity. Medical identity theft often surfaces when you receive bills for services or prescriptions you never received, or when your insurance denies claims due to fraudulent medical records already on file under your name.

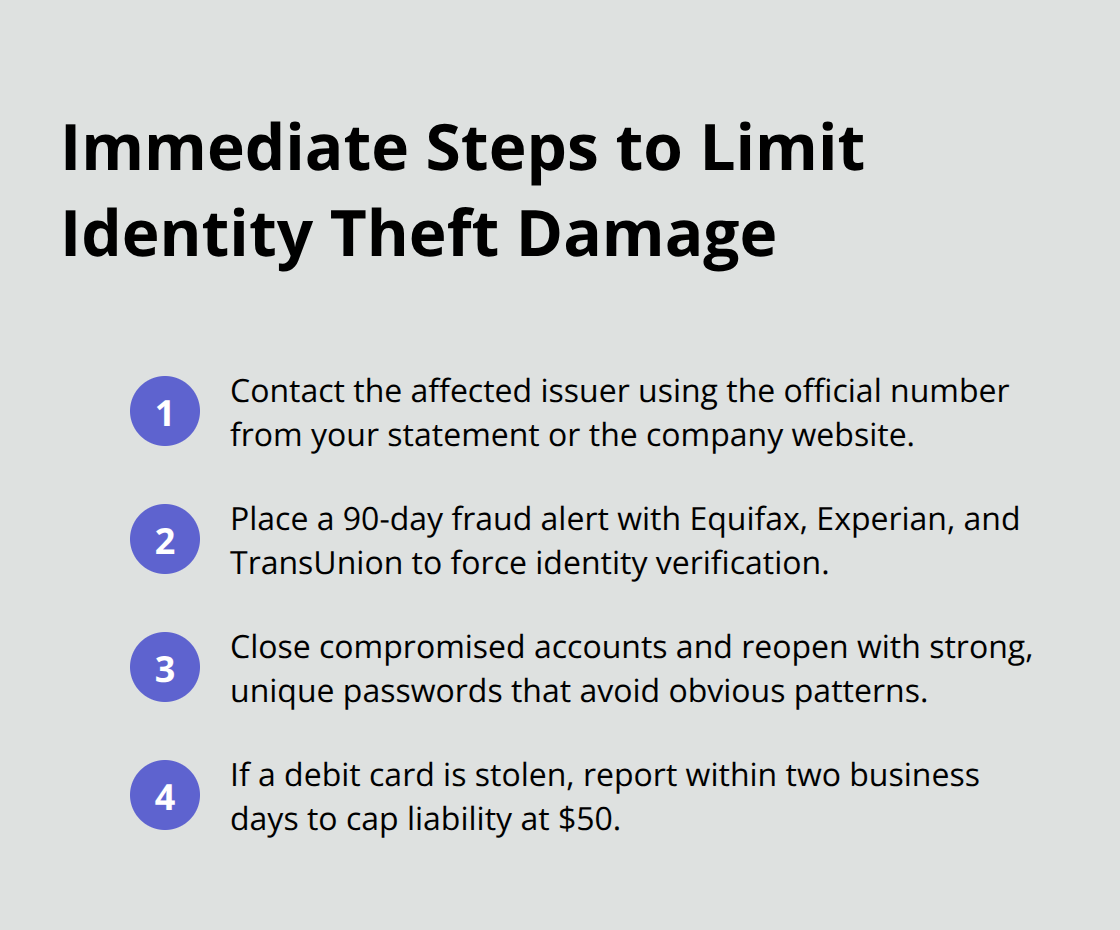

Contact Your Bank and Credit Bureaus Today

Speed matters tremendously in identity theft cases. The moment you suspect fraud, contact the affected account issuer directly-not through the phone number on a suspicious letter, but using the number on your legitimate statement or the company’s official website. Place a fraud alert with all three credit bureaus online or by phone within the same day; Equifax can be reached at 800-525-6285, and fraud alerts last 90 days, forcing creditors to verify your identity before opening new accounts. Close any compromised accounts immediately and open new ones with strong, unique passwords that avoid obvious patterns (such as your mother’s maiden name or the last four digits of your Social Security number).

If your debit card was stolen, contact your bank immediately; your liability caps at $50 if you report within two business days, but waiting longer increases your exposure significantly.

File Reports With Law Enforcement and the FTC

File a police report and obtain a copy; law enforcement needs this documentation, and creditors require it to process disputes. File a complaint with the FTC at identitytheft.gov-their complaint database feeds directly into law enforcement investigations nationwide. Dispute fraudulent items with credit bureaus by certified mail, including your police report and the FTC Identity Theft Affidavit (which most bureaus and creditors accept as proof). Keep meticulous records of all communications, including dates, times, names of representatives, and copies of every letter or email you send.

The steps you take in these first hours and days determine how quickly you regain control of your identity and finances. Understanding your legal rights under California and federal law strengthens your position considerably when holding responsible parties accountable.

What Laws Protect You After Identity Theft

The Fair Credit Reporting Act Gives You Real Power

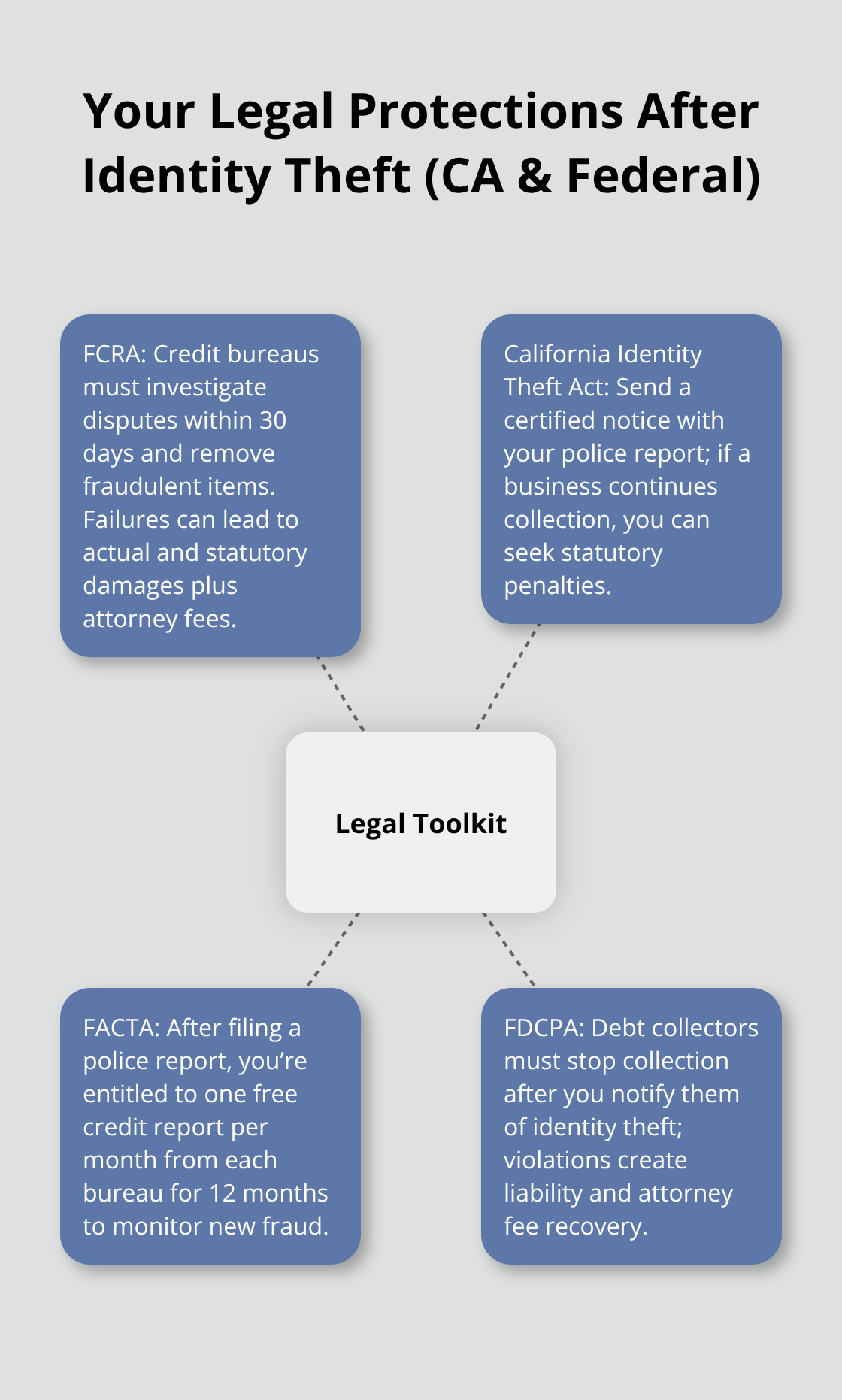

California and federal law give you concrete tools to fight identity theft and recover damages from both criminals and the companies that failed to protect your data. The Fair Credit Reporting Act stands as your primary federal protection, requiring credit bureaus to investigate any disputes you file within 30 days and remove fraudulent accounts or inquiries if the investigation reveals errors. When a credit bureau ignores your dispute or a creditor fails to investigate after you prove identity theft, you can sue for actual damages-including the cost of credit restoration, lost wages, and emotional distress-plus statutory damages up to $1,000 per violation and attorney fees.

California’s Identity Theft Act Holds Businesses Accountable

California’s Identity Theft Act strengthens this protection by holding businesses liable when they continue pursuing fraudulent claims despite receiving notice of identity theft and evidence of the fraud. To trigger liability under this law, send the business a certified letter with your police report and documentation of the theft; if they ignore this notice and keep pursuing collection, you gain the right to recover statutory penalties. The Fair and Accurate Credit Transactions Act adds another layer by entitling identity theft victims to one free credit report per month from each bureau for 12 months after filing a police report, allowing you to monitor for new fraudulent accounts.

These aren’t theoretical rights-they translate directly into leverage when negotiating with creditors and credit bureaus.

Debt Collectors Must Stop When You Notify Them of Fraud

Debt collectors pursuing fraudulent debts face liability under the Fair Debt Collection Practices Act if they continue collection efforts after you notify them of identity theft. California’s version of this law mirrors federal protections and allows recovery of attorney fees, making it economically viable to fight back. When a debt collector contacts you about an account you didn’t open, respond in writing within 30 days stating you are a victim of identity theft and attaching your police report and FTC Identity Theft Affidavit; this documented response creates a record of your dispute and shifts the burden to the collector to verify the debt. If a collector ignores this notice, they violate federal law and expose themselves to liability.

Additional Protections: Intrusion Upon Seclusion and Beyond

California also recognizes intrusion upon seclusion as a tort, meaning you can sue individuals or companies that intentionally access or misuse your private information in a way that’s highly offensive and causes harm. The combination of these federal and state protections means you have multiple pathways to hold responsible parties accountable and recover compensation without paying attorney fees upfront-most identity theft claims operate on contingency. Understanding which law applies to your situation determines your recovery options and the strength of your negotiating position with creditors, bureaus, and collectors.

Why Local Representation Matters for Identity Theft

Companies Exploit Victims Who Fight Alone

Identity theft recovery demands more than knowing the law-it requires someone who understands how California courts interpret these protections and how creditors, debt collectors, and credit bureaus actually respond to legal pressure. When you handle disputes alone, companies exploit gaps in your knowledge. Debt collectors continue calling despite your written disputes. Credit bureaus ignore your fraud documentation. Creditors refuse to remove fraudulent accounts. These aren’t accidents; they’re calculated moves based on the assumption that most victims lack the resources to fight back.

How Multiple Legal Pathways Create Real Leverage

A strategic approach combines federal protections under the Fair Credit Reporting Act and Fair Debt Collection Practices Act with California’s Identity Theft Act to build multiple leverage points simultaneously. When a creditor sees that you’ve filed a police report, obtained your FTC Identity Theft Affidavit, and now have an attorney pursuing statutory damages under California law, their negotiating position collapses. Most cases settle before trial because companies calculate that fighting costs more than paying.

The True Cost of Fraudulent Accounts and Credit Damage

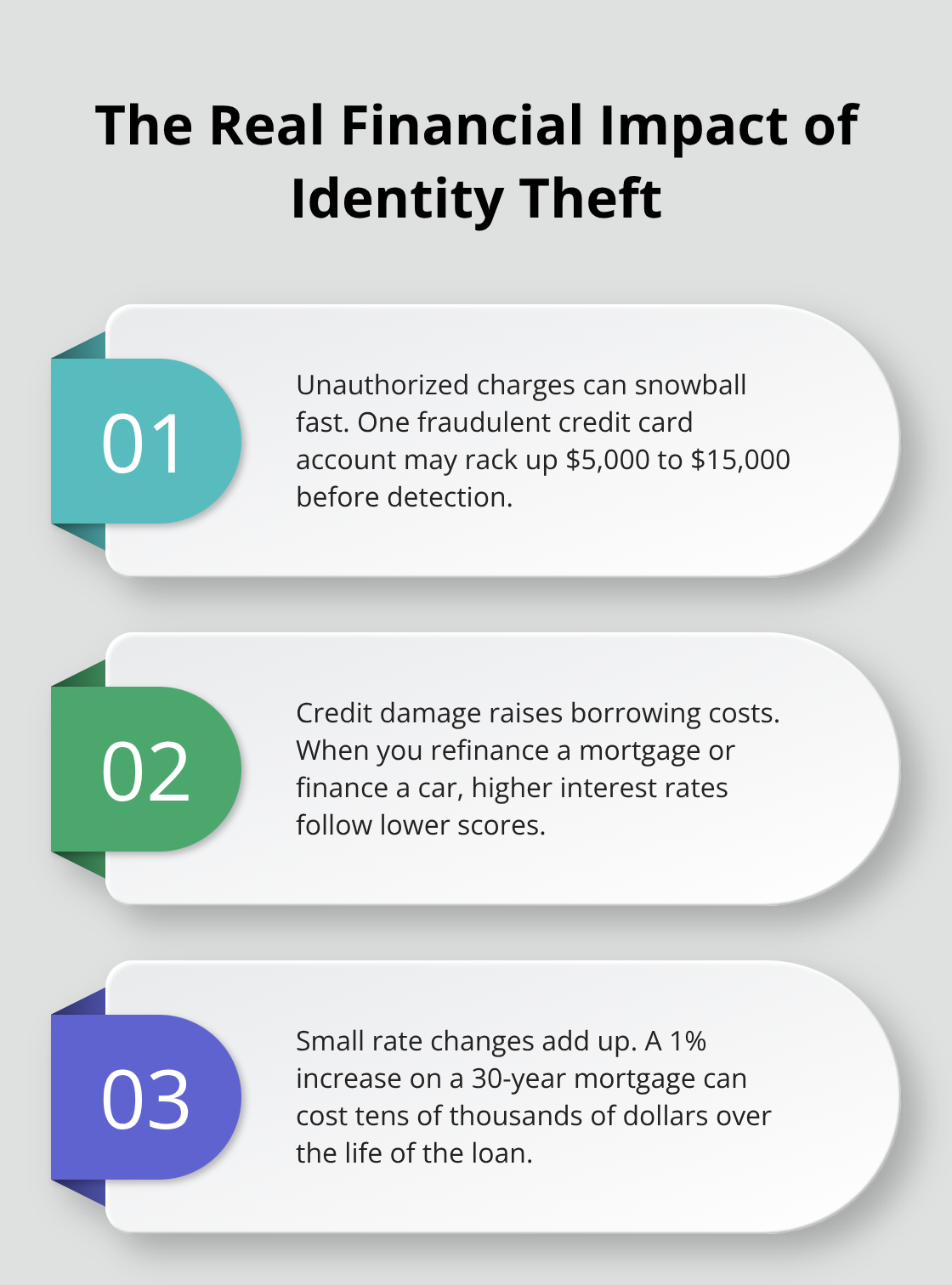

The financial stakes in identity theft cases are substantial. A single fraudulent credit card account opened in your name can generate $5,000 to $15,000 in unauthorized charges before you catch it. More damaging, fraudulent inquiries and accounts tank your credit score, which means when you refinance your mortgage or take out a car loan, you’ll pay higher interest rates. A 1% increase on a 30-year mortgage translates to tens of thousands of dollars in additional costs.

Emotional Distress Damages Are Real and Recoverable

Beyond financial losses, identity theft victims report severe emotional distress-anxiety about mail, fear of opening statements, sleepless nights worrying about new fraudulent accounts. California law recognizes these harms and allows recovery for emotional distress damages alongside actual financial losses. A free case review identifies which damages apply to your situation and estimates the realistic value of your claim.

Contingency Representation Removes Financial Barriers

Professional legal representation on contingency means you pay nothing upfront and only if money is recovered. This structure eliminates the financial barrier that keeps most victims from pursuing justice. When you contact an attorney, they gather your FTC report, police report, credit reports, and documentation of fraudulent accounts, then analyze which companies failed their legal obligations and which collectors violated the law. That analysis determines your recovery strategy and the potential compensation you can obtain.

Final Thoughts

Identity theft in California exposes you to financial losses, damaged credit, and emotional harm that can persist for years. The Fair Credit Reporting Act, California’s Identity Theft Act, and the Fair Debt Collection Practices Act provide real pathways to recover damages and hold responsible parties accountable. These protections only work when you act quickly and strategically-filing a police report, placing fraud alerts, and documenting everything creates the foundation for a strong claim.

Creditors, debt collectors, and credit bureaus count on victims fighting alone and abandoning disputes when initial responses are ignored. An identity theft lawyer in California brings the legal knowledge and negotiating power that shifts the balance in your favor. When companies see professional representation pursuing statutory damages under multiple laws simultaneously, settlement becomes their rational choice (fraudulent accounts generate thousands in unauthorized charges, and damaged credit costs you tens of thousands in higher interest rates over time).

We at Bontrager Law represent California consumers in identity theft cases and recover damages through a coordinated strategy that maximizes your recovery without requiring upfront attorney fees. Contact Bontrager Law today to discuss your situation and take the next step toward clearing your name and recovering what you’ve lost.