Identity theft happens faster than most people realize. Criminals open accounts, rack up charges, and damage credit scores while victims remain unaware for months.

Credit identity theft symptoms often go unnoticed until the damage is severe. At Bontrager Law, we’ve helped countless people recover from this financial devastation, and we know that spotting warning signs early makes all the difference.

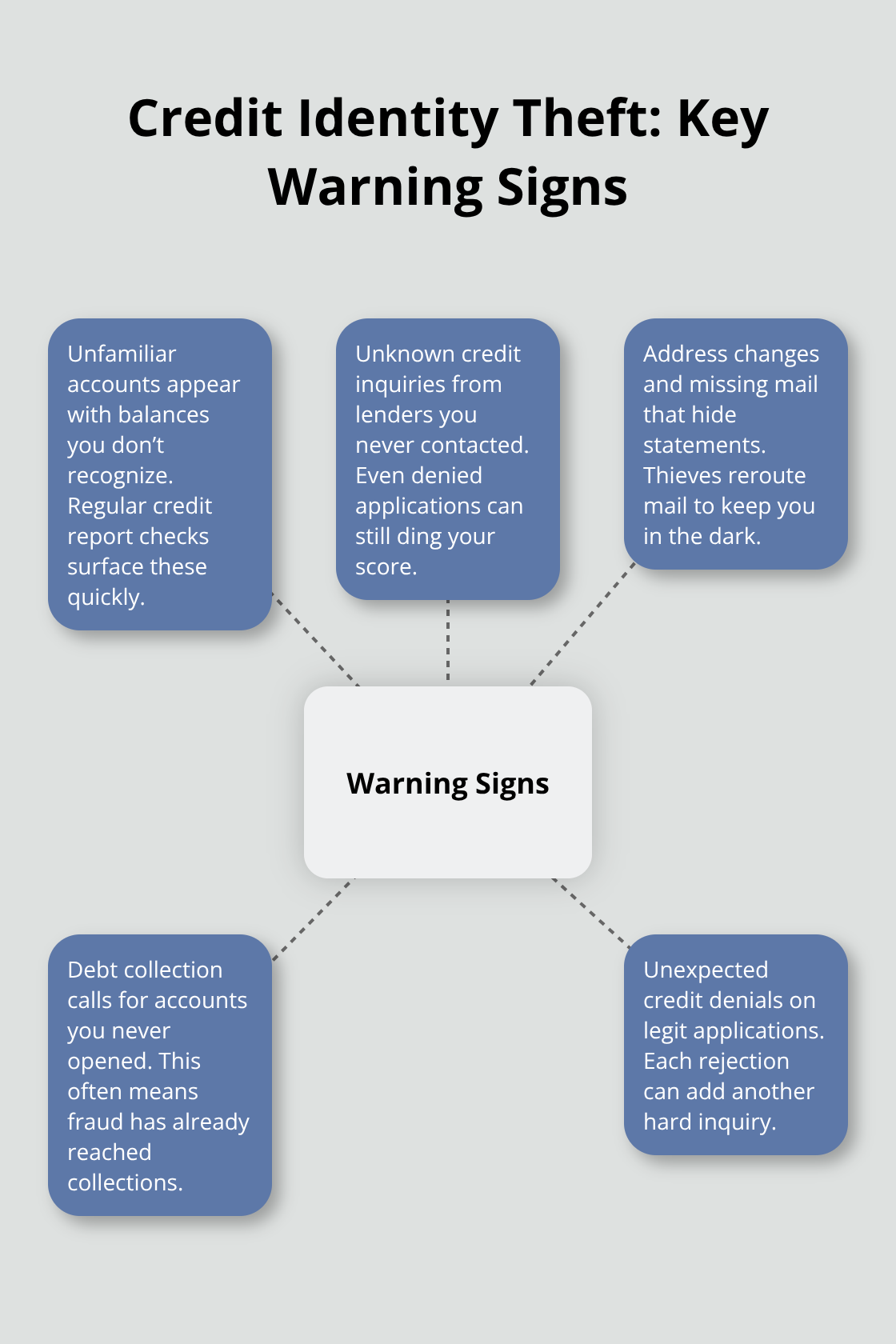

What Warning Signs Actually Appear on Your Credit

Unfamiliar Accounts Signal Immediate Trouble

The moment identity thieves open accounts in your name, traces appear across your credit profile. Checking your credit report regularly reveals these traces before criminals cause irreversible damage. The FTC reports that identity theft victims often discover the fraud months after it begins, which means the accounts have already tanked their credit scores and created a financial mess.

Unfamiliar accounts represent the most obvious red flag-accounts you never opened appearing with balances you never incurred. Credit inquiries from lenders you never contacted signal that someone used your information to apply for credit. These inquiries stay on your report and damage your score even if the applications were denied.

Address Changes and Missing Mail

Missing mail or mail arriving at addresses you don’t recognize can mean your identity thief changed your address to hide fraudulent statements. Some thieves deliberately redirect your mail so you remain unaware while they accumulate debt in your name. This tactic allows fraudsters to operate for months without detection.

Debt Collection Calls About Unknown Accounts

Debt collection calls about accounts you don’t recognize represent another critical warning sign that demands immediate action. Collectors contact you about balances supposedly owed on credit cards, medical bills, or loans you never opened. These calls indicate that fraudsters already damaged your credit and passed the accounts to collection agencies.

Unexpected Credit Denials

Denial of credit applications you actually submitted often signals identity theft operating in the background. Your credit score dropped without explanation, or lenders see fraudulent accounts on your report that block your approval. Some victims discover this when applying for a mortgage, auto loan, or credit card and face unexpected rejection despite having maintained responsible credit. The damage compounds because each rejected application adds another inquiry to your report.

Take Action Across All Three Bureaus

Contact all three credit bureaus-Equifax, Experian, and TransUnion-immediately to place a fraud alert and obtain free copies of your complete credit reports. Review every account listed, every inquiry, and every address. Fraudsters exploit the fact that most people check their credit only once yearly, if at all. Once you spot these warning signs, the next critical step involves understanding what actions produce real results in stopping the thieves and protecting your accounts from further damage.

How Identity Theft Damages Your Credit and Finances

Your Credit Score Takes an Immediate Hit

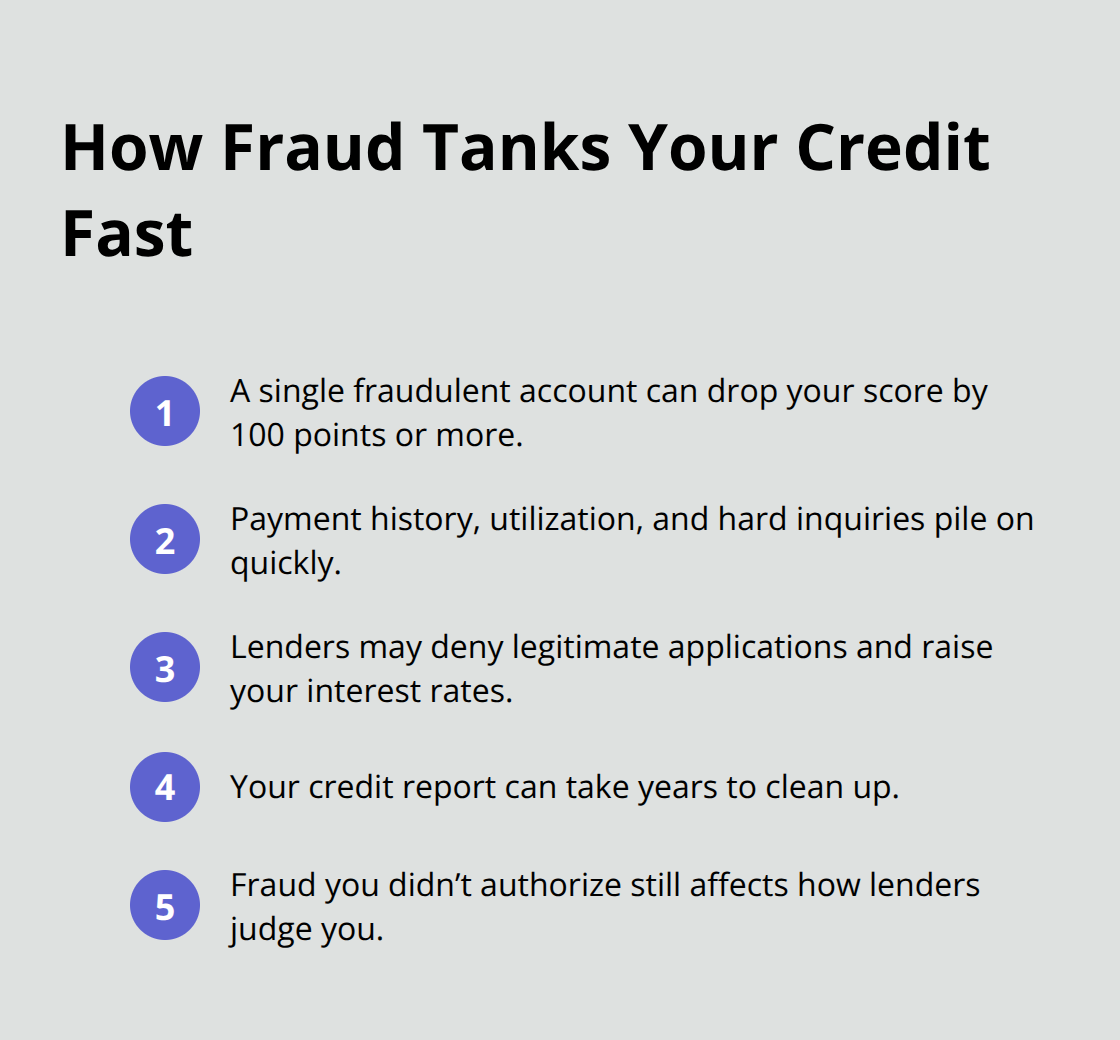

Identity theft destroys your credit score faster than almost any other financial mistake. When a thief opens accounts in your name, those accounts generate payment history, credit utilization, and inquiries that tank your score immediately. A single fraudulent account can drop your score by 100 points or more, depending on the account type and balance.

Lenders see the fraudulent accounts and deny your legitimate applications, forcing you to accept higher interest rates on any credit you qualify for. Your credit report becomes a mess that takes years to untangle, and lenders judge your trustworthiness based on fraudulent activity you never authorized.

Fraudulent Charges Create Immediate Financial Bleeding

Fraudulent charges and accounts drain your finances faster than most victims anticipate. A thief opening a credit card in your name with a $5,000 limit and maxing it out means you’re responsible for those charges until you prove fraud. Medical identity theft, where thieves use your information for healthcare services, creates hospital bills that appear on your credit report and send to collections within months. Loan fraud causes even worse damage-someone taking out an auto loan or personal loan in your name means you’re liable for thousands in debt plus interest.

Long-Term Consequences That Extend Years Into Your Future

The damage extends far beyond the initial fraud. Negative accounts remain on credit reports for seven years from the date of first delinquency. During this period, you face higher insurance premiums, difficulty renting apartments, and barriers to employment (since many employers check credit reports). Some victims have been denied housing because landlords viewed the fraudulent accounts as proof of financial irresponsibility. The financial toll isn’t just the stolen amounts-it’s the compounding costs of higher interest rates on legitimate credit, security deposits required from skeptical lenders, and the time spent proving fraud to each creditor and bureau separately.

The damage compounds because each fraudulent account and rejected application adds another layer of complexity to your financial recovery. Once identity thieves establish themselves in your credit profile, stopping them requires swift action across multiple fronts-and understanding exactly what steps produce real results in halting the fraud and protecting your remaining accounts matters more than ever.

Steps to Take Immediately After Discovering Identity Theft

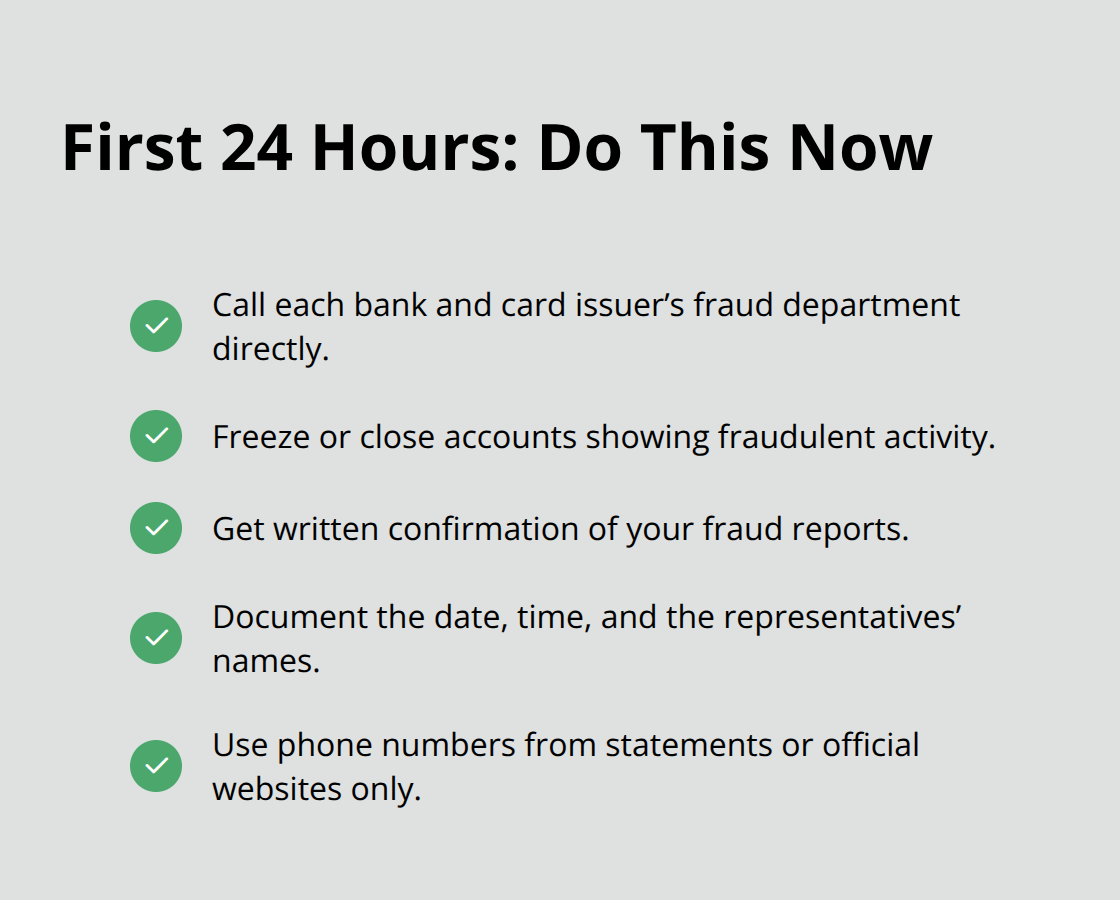

Act Within the First 24 Hours

The first 24 hours after discovering identity theft determine whether you contain the damage or watch it spiral. Contact your bank and credit card companies immediately-not tomorrow, not after work, today. Call the fraud departments directly using the phone numbers on your statements or official websites, never numbers from suspicious emails or letters. Tell them which accounts show fraudulent activity and request that they freeze or close those accounts. The FTC reports that quick action significantly reduces the total damage victims experience. Ask each institution to send written confirmation of your fraud report, and document the date, time, and name of every person you speak with. This documentation becomes critical later when disputing charges or proving you reported fraud promptly.

Place Fraud Alerts With All Three Credit Bureaus

Contact all three credit bureaus-Equifax, Experian, and TransUnion-to place fraud alerts on your accounts. You only need to contact one bureau, and that bureau will notify the other two, but calling all three directly confirms the alert was placed. An initial fraud alert lasts one year and lets you request free credit reports from all three bureaus without the standard waiting period. An extended fraud alert lasts seven years if you file a police report or complete an FTC identity theft report, and it removes you from marketing lists for unsolicited credit offers for five years. Tell the bureaus to add a statement to your credit file requesting that creditors call you before opening new accounts. Request that they mail your credit reports to your address, not electronically, since thieves may have compromised your email.

File Your FTC Identity Theft Report

File a report with the Federal Trade Commission at IdentityTheft.gov or call 1-877-438-4338. The FTC’s online tool guides you through creating a personalized recovery plan and generates an Identity Theft Report that you can share with creditors, bureaus, and law enforcement. This report carries legal weight-creditors must accept it as proof of fraud when you dispute charges. Forward copies to your bank, credit card companies, and any creditors associated with fraudulent accounts within 30 days of filing your FTC report.

Final Thoughts

Speed matters when you spot credit identity theft symptoms. Every hour you delay allows fraudsters to open more accounts, rack up more charges, and dig deeper into your financial life. Victims who contact their banks and credit bureaus within 24 hours typically limit their losses to a fraction of what those who wait experience, and FTC data confirms this reality.

We at Bontrager Law have spent nearly 20 years helping California residents recover from identity theft and credit reporting damage. Our team has handled thousands of claims and recovered millions for victims who felt powerless against fraudsters and unresponsive creditors (many of whom refuse to acknowledge fraud or reinstate fraudulent accounts months after removal). We know that identity theft recovery requires persistent follow-up with creditors, credit bureaus, and debt collectors who continue pursuing debts you never incurred.

File your FTC report today, contact your banks and bureaus, and document everything. If creditors resist your fraud claims or fraudulent accounts remain on your report after 30 days, contact us for a free case review. We represent individuals across California in identity theft disputes and handle the creditor negotiations and bureau disputes so you can focus on rebuilding your financial life.