A single error on your credit report can tank your score and cost you thousands in higher interest rates. The Fair Credit Reporting Act gives you the right to challenge inaccurate information, but most people don’t know where to start.

At Bontrager Law, we’ve helped countless clients navigate the FCRA dispute process and reclaim their financial standing. This guide walks you through each step, from identifying errors to escalating your case when credit bureaus refuse to cooperate.

Understanding Credit Report Errors and Your Rights

What Errors Actually Appear on Credit Reports

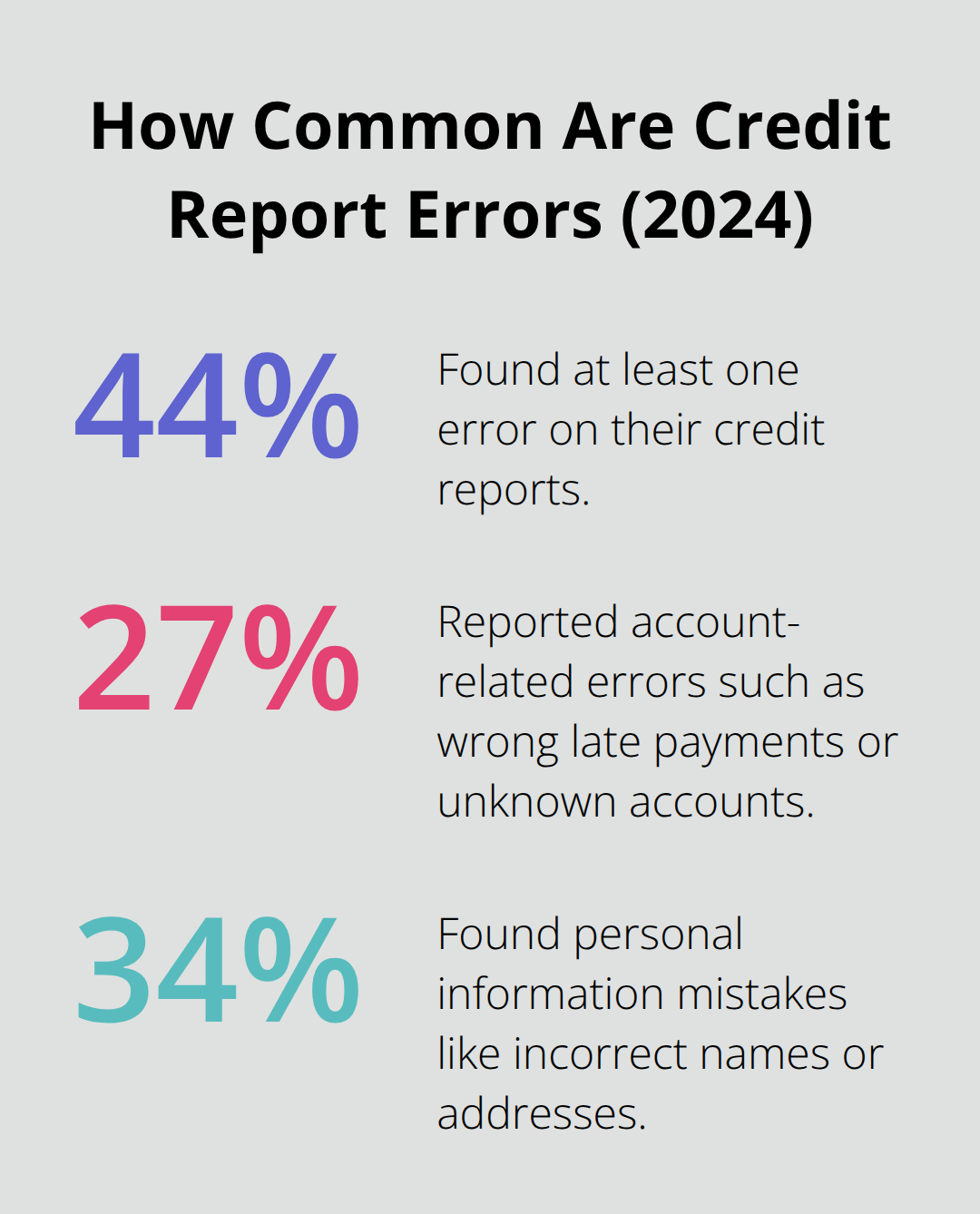

Credit report errors are far more common than most people realize. A 2024 study by Consumer Reports and WorkMoney surveyed over 4,000 participants and found that 44% discovered at least one error on their credit reports. The most damaging errors fall into two categories: account information mistakes and personal information errors.

Account errors include unrecognized accounts, late payments reported despite being paid on time, and debts that don’t belong to you listed in collections. Personal information errors show up as incorrect names, addresses, or birth dates. The 2024 study revealed that 27% of participants found account errors and 34% found personal information mistakes. These aren’t rare edge cases-they’re widespread problems affecting millions of Americans.

Why the FCRA Exists

The Fair Credit Reporting Act exists specifically because credit bureaus and the companies that report data to them frequently get things wrong. The law gives you the right to demand accuracy at no cost. Both credit bureaus and furnishers (the companies reporting the data) must investigate disputes and correct inaccurate information when you challenge them.

How Errors Tank Your Finances

A single error can devastate your financial life. When inaccurate information stays on your report, it directly lowers your credit score, making lenders view you as a higher-risk borrower. This means higher interest rates on mortgages, auto loans, and credit cards. A late payment error that shouldn’t be there can cost you tens of thousands in extra interest over the life of a home loan.

Beyond credit access, errors create ripple effects into employment, housing, and insurance decisions. Landlords use credit reports to screen tenants, employers may review reports for certain positions, and insurers use credit scores to set rates. The FCRA protects you from this cascading damage by requiring both credit bureaus and furnishers to investigate disputes and correct inaccurate information.

What the FCRA Actually Covers

The law applies to all consumer reporting agencies, not just credit bureaus. Medical information companies and tenant screening services fall under FCRA protections too, meaning errors in those systems carry the same weight as traditional credit report mistakes. The FCRA also prevents frivolous disputes from clogging the system: bureaus can dismiss disputes they reasonably determine are frivolous or irrelevant, though they must notify you within five business days if they do so.

Now that you understand what errors look like and why they matter, the next step is learning how to identify errors on your own report and file an effective dispute.

Filing Your Dispute With the Credit Bureaus

Getting Your Credit Reports

Start by obtaining your actual credit reports from all three bureaus-Experian, Equifax, and TransUnion. You can access them free once yearly at AnnualCreditReport.com, and Equifax currently offers up to six free reports per year through 2026. Pull all three reports because errors often appear on one bureau’s file but not the others. Once you have them in hand, go through each report line by line and mark every error you find. The 2024 Consumer Reports and WorkMoney study showed that 25% of participants initially struggled to access their reports due to security questions or system errors, so if you hit a wall, try a different bureau’s website or call their phone line directly-Experian at 888-397-3742, TransUnion at 800-916-8800, or Equifax at 866-349-5191.

Preparing Your Dispute Letter

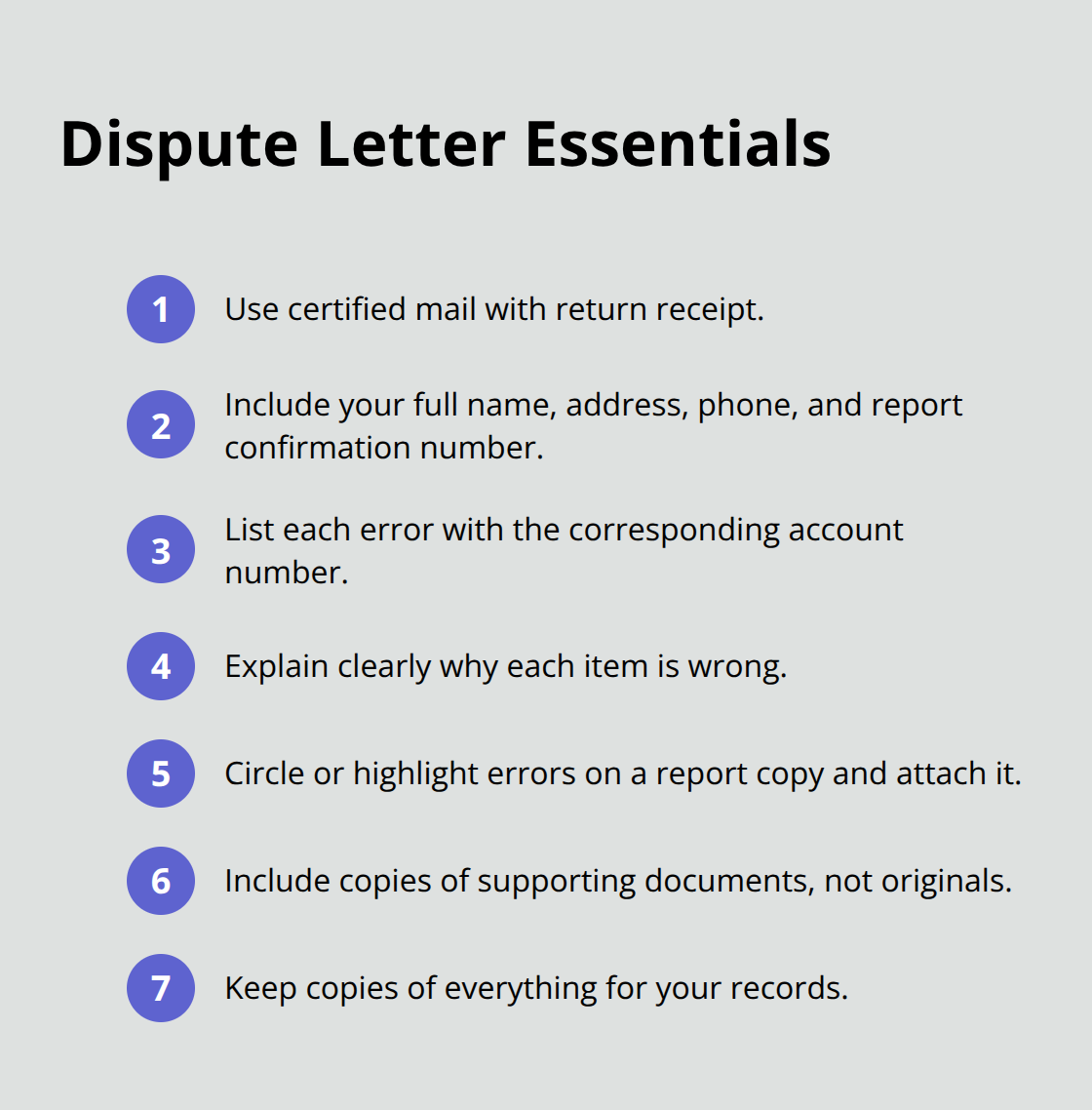

When you’re ready to dispute, contact each bureau reporting the error in writing. Use certified mail with return receipt so you have proof of delivery. Your dispute letter needs your full name, address, phone number, and the credit report confirmation number if available. List every error separately with the account number for each disputed item and explain clearly why it’s wrong. Circle or highlight the errors on a copy of your report and attach it to your letter.

Include copies of supporting documents-payment receipts, statements showing the account was paid on time, or proof that an account doesn’t belong to you. The FTC provides a ready-to-use sample letter template on their website that you can adapt for your situation. Send copies only, never originals, and keep everything for your records.

What Happens During Investigation

The bureau has 30 days to investigate your dispute. If they determine your dispute is frivolous or irrelevant, they’ll notify you within five business days, but this rarely happens if you’ve provided solid documentation. During the investigation, the bureau must forward your dispute and all supporting materials to the furnisher-the company that originally reported the information. The furnisher then has 30 days to investigate and respond. If they find the information is wrong or can’t verify it, they must notify all three bureaus to correct or delete it. You’ll receive written results within that timeframe, and if information changed, you’ll get a free updated credit report.

When the Furnisher Disagrees

If the furnisher determines the information is accurate and won’t change it, you can ask the bureaus to include a short statement about your dispute in your file, and that statement appears on future reports to potential lenders. This dispute notation signals to creditors that you’ve challenged the accuracy of the information. However, if the furnisher refuses to correct legitimate errors or the investigation stalls, you’ll need to escalate your case with additional documentation and potentially seek outside help to force compliance.

What to Do If the Dispute Process Fails

When Bureaus Refuse to Correct Errors

The 30-day investigation window closes, and the bureau sends you a letter stating the furnisher verified the information as accurate. Or worse, the bureau simply ignores your dispute. At this point, most people assume they’re stuck, but the FCRA gives you multiple paths forward. The Consumer Financial Protection Bureau received 430,600 credit-report complaints in 2023, up from 165,129 in 2021, signaling that bureaus and furnishers frequently fail to correct legitimate errors on the first attempt.

Filing a Complaint With the CFPB

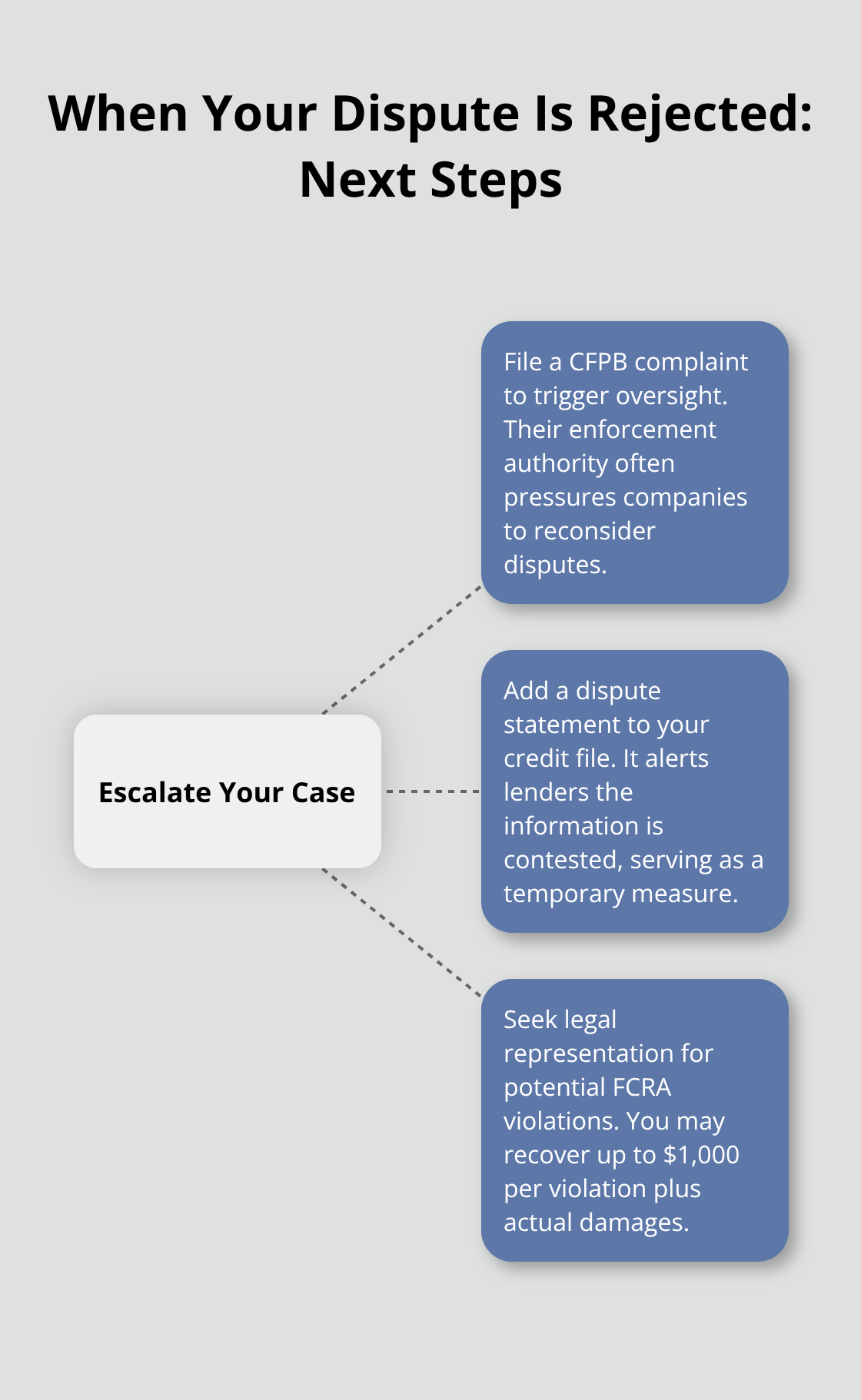

If your dispute stalled or the bureau refused to act, file a complaint with the CFPB at consumerfinance.gov. The CFPB has enforcement authority over credit bureaus and furnishers, and their investigation often pressures companies to reconsider disputes they initially rejected. Document everything in your complaint: the original error, your dispute letter, the bureau’s response, and why you believe their investigation was incomplete.

Include specific details about how the error affected you financially. The CFPB takes complaints seriously because they track patterns across thousands of consumers, and if they see a bureau repeatedly dismissing valid disputes, enforcement action follows.

Adding a Dispute Statement to Your File

Escalating beyond the CFPB requires adding a dispute statement to your credit file if the bureau refuses correction. This statement appears on your report and future reports sent to lenders, explaining that you’ve contested the accuracy of the information. While a dispute notation doesn’t remove the error, it signals to creditors that the information is contested. However, this is a holding action, not a solution.

Pursuing Legal Action for FCRA Violations

If the error remains and continues to damage your credit or prevent loan approval, you need legal representation. Many FCRA violations entitle you to statutory damages of up to $1,000 per violation plus actual damages, meaning you can recover money even if the error was eventually fixed. A consumer protection firm can demand that the bureau conduct a second investigation, file suit against the furnisher for failing to verify information, or pursue claims against the bureau itself for violating FCRA requirements. Courts have consistently ruled that when a bureau receives a dispute with supporting documentation and fails to investigate thoroughly, that constitutes a violation, regardless of whether the underlying information is ultimately correct. A consumer protection firm represents individuals across California in credit reporting disputes and related claims against banks, collectors, and large corporations, offering a free case review to evaluate your situation.

Final Thoughts

The FCRA dispute process gives you concrete tools to fight back against credit reporting errors, but success requires persistence and documentation. You now understand how to identify errors, file disputes with credit bureaus and furnishers, and escalate when initial attempts fail. The reality is that 44% of Americans find errors on their reports, and many of those errors persist through the first investigation cycle.

Credit bureaus and furnishers operate under financial pressure to process disputes quickly, not thoroughly. When you submit documentation showing an error, they sometimes ignore it or conduct investigations so cursory that legitimate disputes get rejected. If a bureau refuses to correct an error despite your evidence, or if an error continues damaging your credit score and loan applications, you need someone who understands FCRA violations and can demand accountability.

We at Bontrager Law represent individuals across California in credit reporting disputes and related claims against banks, collectors, and large corporations. Many FCRA violations entitle you to up to $1,000 per violation plus actual damages, meaning you can recover money even if the error was eventually corrected. Start with a free case review to understand your options and whether legal action makes sense for your situation.