Your credit report affects everything from loan approvals to job opportunities. California FCRA updates have recently made it easier to protect yourself when errors appear on your report.

At Bontrager Law, we’ve seen how these changes shift the balance in consumers’ favor. Understanding what changed and how it impacts your rights is the first step toward safeguarding your financial reputation.

What the FCRA Actually Does

The Fair Credit Reporting Act is a federal law that governs how credit bureaus collect, maintain, and distribute information about you. It does not grant blanket debt removal rights, and it does not erase accurate negative information simply because you want it gone. What it actually does is enforce three core rights: the right to know what’s in your file, the right to dispute inaccuracies, and the right to have outdated items removed after set periods.

How Long Negative Information Stays on Your Report

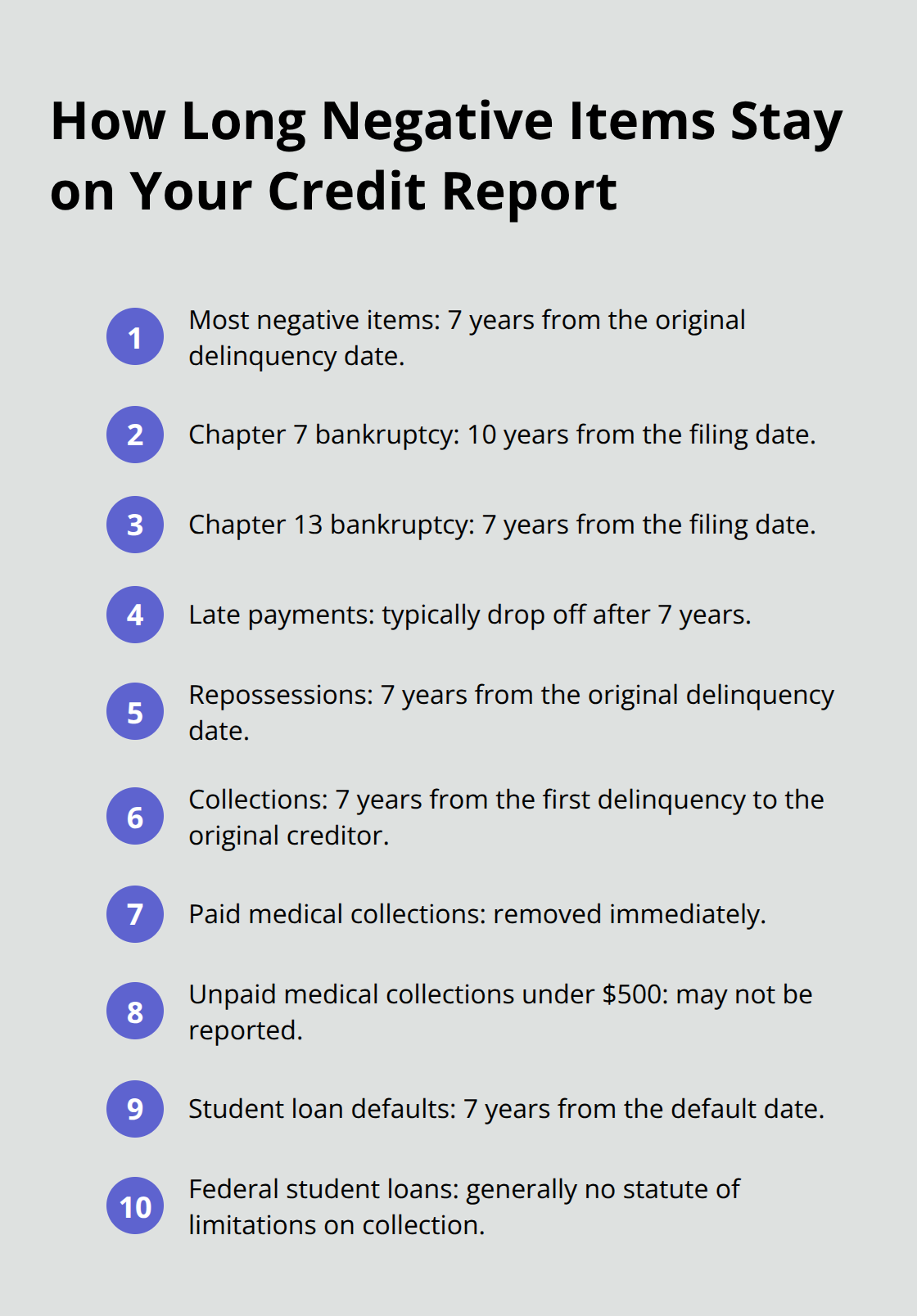

Most negative information must be removed after seven years from the original delinquency date, with bankruptcies staying for ten years under Chapter 7 or seven years under Chapter 13 from the filing date. Late payments typically drop off after seven years, repossessions stay for seven years from the original delinquency date, and collections also follow the seven-year rule starting from the date of first delinquency to the original creditor. Medical debt reporting has shifted significantly-paid medical collections are removed immediately, and unpaid medical collections under $500 may not be reported due to industry changes. Student loan defaults stay for seven years from the default date, though federal student loans generally have no statute of limitations on collection.

Why California Goes Harder Than Federal Law

California layers additional protections on top of the FCRA that give you stronger rights than consumers in other states. The state’s enforcement has intensified, with state attorneys general collaborating with the Consumer Financial Protection Bureau to pursue FCRA violations aggressively. California’s Fair Chance Act, updated in July 2023 by the California Civil Rights Council, expanded protections in hiring and background screening that directly intersect with credit reporting.

San Diego’s Fair Chance Ordinance, effective October 1, 2024, requires local employers to notify applicants of their right to file complaints with the California Civil Rights Department and the San Diego Office of Labor Standards and Enforcement. These state-level requirements mean that employers cannot simply rely on inaccurate credit information to deny you employment-they must follow strict procedures and consider mitigating circumstances. If you live outside California but deal with California employers or lenders, these protections apply to you.

What This Means for Your Position

California’s stricter standards create liability for companies that cut corners on accuracy and disclosure, which strengthens your position when pursuing claims for violations. The practical takeaway is that you hold more leverage in California than in most other states when inaccurate information harms your credit or employment prospects. This foundation of state-level enforcement sets the stage for understanding what specific changes now affect your rights as a consumer.

What Actually Changed in 2026

Fee Increases and Free Access Rights

Starting January 1, 2026, the maximum charge for obtaining your FCRA file disclosure rose to $16.00, up from $15.50 the previous year. However, this fee increase does not affect your most important right: you still access free weekly file disclosures from Equifax, Experian, and TransUnion at no cost. The fee applies only when you request paid disclosures beyond your free annual reports, so most consumers never pay this charge.

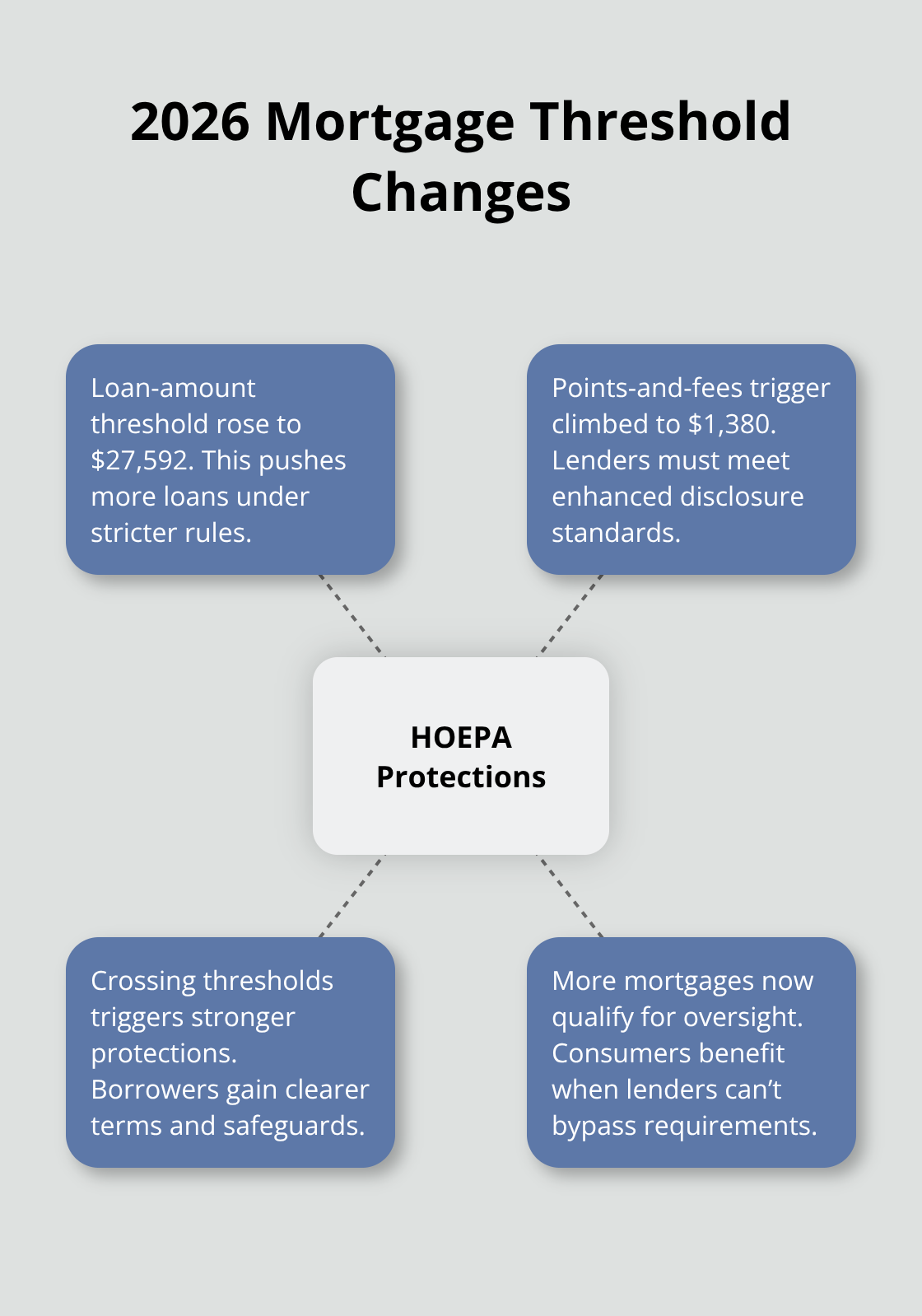

Mortgage Threshold Changes That Affect Your Protections

Mortgage regulations shifted significantly in 2026, with high-cost mortgage thresholds under HOEPA jumping in your favor. The loan-amount threshold rose to $27,592, and the points-and-fees trigger climbed to $1,380. These numbers matter because lenders crossing these thresholds must follow stricter disclosure and protection requirements that benefit you as a borrower.

If you shop for a mortgage or challenge one already in place, these higher thresholds mean more loans now qualify for enhanced consumer protections that lenders cannot bypass.

Medical Debt Reporting Gets Consumer-Friendly

Medical debt reporting underwent the most significant shift in recent years. Paid medical collections now disappear from your report immediately, and unpaid medical collections under $500 may not appear at all due to industry-wide changes. This change removes a major source of credit damage for consumers facing medical hardship, since medical debt no longer haunts your file indefinitely.

California’s Arbitration Restrictions and Data Security Rules

California’s SB 82, effective January 1, 2026, fundamentally restricted arbitration clauses in consumer and credit agreements-arbitration now covers only the specific goods, services, or credit actually addressed in your contract, not every dispute that might arise. This change gives you more power to pursue claims in court rather than being locked into private arbitration. The FTC also strengthened data security requirements: financial institutions must report to the FTC any unauthorized access event involving 500 or more unencrypted customer records. Data breaches involving your personal information now trigger mandatory notification and regulatory scrutiny, increasing accountability and your ability to document harm if your information was compromised.

What These Changes Mean for Your Next Steps

These 2026 updates collectively shifted enforcement and consumer protections in your favor, making credit bureaus and lenders more cautious about accuracy and more transparent about what information they collect. Understanding these changes positions you to challenge inaccurate reporting more effectively and to recognize when companies fail to follow the rules. The next section walks through exactly how to exercise these rights when errors appear on your report.

How to Actually Fix Credit Report Errors

Errors on your credit report cost you money. A single inaccuracy can tank your score by 50 to 100 points, which translates directly into higher interest rates on mortgages, auto loans, and credit cards. The 2026 FCRA updates made the dispute process faster and clearer, but most consumers still miss critical steps that could strengthen their claims.

Start With Your Free Reports

Obtain your free credit reports from all three bureaus at annualcreditreport.com, not from the bureaus’ own websites where they may try to upsell you. Review each report line by line and document every error in writing-do not rely on phone calls or memory. You need written evidence of what you reported and when.

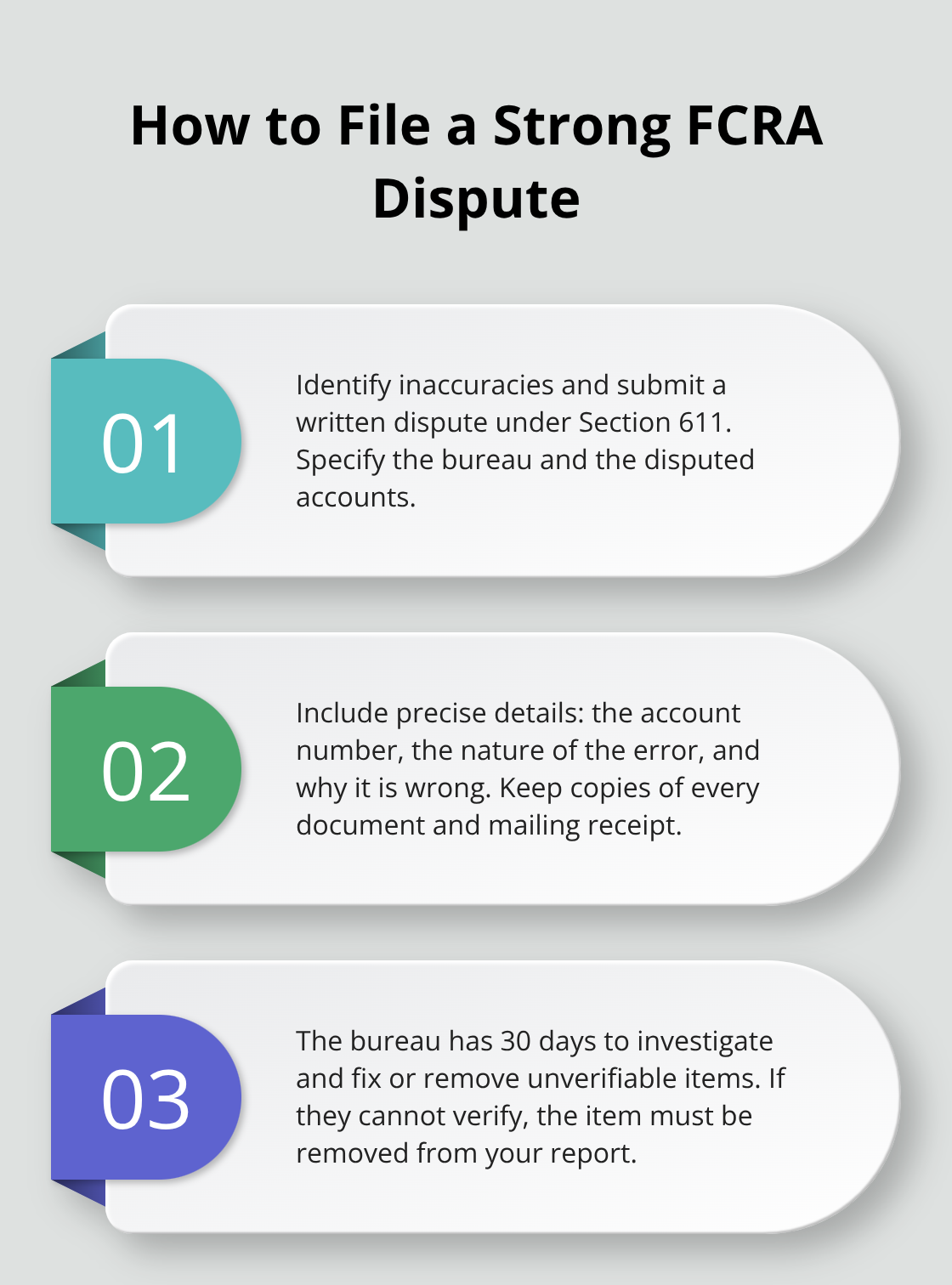

File Your Written Dispute

Once you identify inaccuracies, submit a written dispute to the credit bureau using Section 611 of the FCRA. Include specific details: the account number, the nature of the error, and why the information is wrong. Keep copies of everything. The credit bureau then has 30 days to investigate and either correct or remove the inaccuracy, or verify it’s accurate. If they cannot verify the information, it must come off your report.

Know Your Legal Remedies

If 30 days pass with no response or if they fail to remove an inaccuracy after investigation, you have grounds for a claim under FCRA Section 1681n, which can award actual damages plus statutory damages of up to $1,000 per violation, plus attorney fees. California’s SB 82 strengthened your position further by restricting arbitration clauses in consumer agreements, meaning you can now pursue disputes in court rather than being forced into private arbitration where your case stays hidden and you have fewer discovery rights.

Act Fast When Errors Appear

If a bureau ignores your dispute entirely, fails to respond within 30 days, or refuses to remove information they cannot verify, document the violation and contact a firm experienced in FCRA claims. Do not wait months hoping errors resolve themselves, because every month that inaccurate information stays on your report damages your creditworthiness and your employment prospects. If you face a denied loan application or job rejection due to a credit report error, request the adverse action notice from the lender or employer, which must include a copy of the report used in the decision. That notice gives you proof of harm and establishes the timeline for your claim. Many consumers settle their FCRA disputes without litigation once they show the bureau clear documentation of the error and the bureau realizes they cannot defend their position (especially when a firm with FCRA experience enters the case and demonstrates the violation).

Final Thoughts

California FCRA updates in 2026 fundamentally shifted how credit bureaus operate and what rights you hold when errors damage your financial life. Medical debt reporting changes removed a major source of credit damage for consumers facing medical hardship, while mortgage threshold increases mean more loans now qualify for enhanced protections that lenders cannot bypass. California’s SB 82 restriction on arbitration clauses gives you the power to pursue claims in court rather than being locked into private arbitration where disputes stay hidden.

Start by obtaining your free reports from annualcreditreport.com and document every error in writing. File a written dispute under FCRA Section 611 with specific details about the inaccuracy, keep copies of everything, and if the bureau fails to respond within 30 days or refuses to remove information they cannot verify, you have grounds for a claim that can award actual damages plus statutory damages up to $1,000 per violation, plus attorney fees. Do not wait months hoping errors resolve themselves, because every month that inaccurate information stays on your report damages your creditworthiness and employment prospects.

Many consumers settle their FCRA disputes without litigation once they document the error clearly and show the bureau they cannot defend their position. If you need guidance navigating these rights or pursuing a claim, Bontrager Law represents individuals across California in credit reporting disputes and related claims against banks, collectors, and large corporations, and the firm offers a free case review to evaluate your situation and explain your options.