The Fair Credit Reporting Act received significant updates in 2026 that directly affect how your credit information is handled and protected. These 2026 FCRA updates give you stronger rights and faster ways to fix errors on your credit report.

At Bontrager Law, we want you to understand what changed and how it benefits you as a California consumer. This guide walks you through the new regulations, their impact on your credit, and the steps you should take right now.

What Changed in 2026

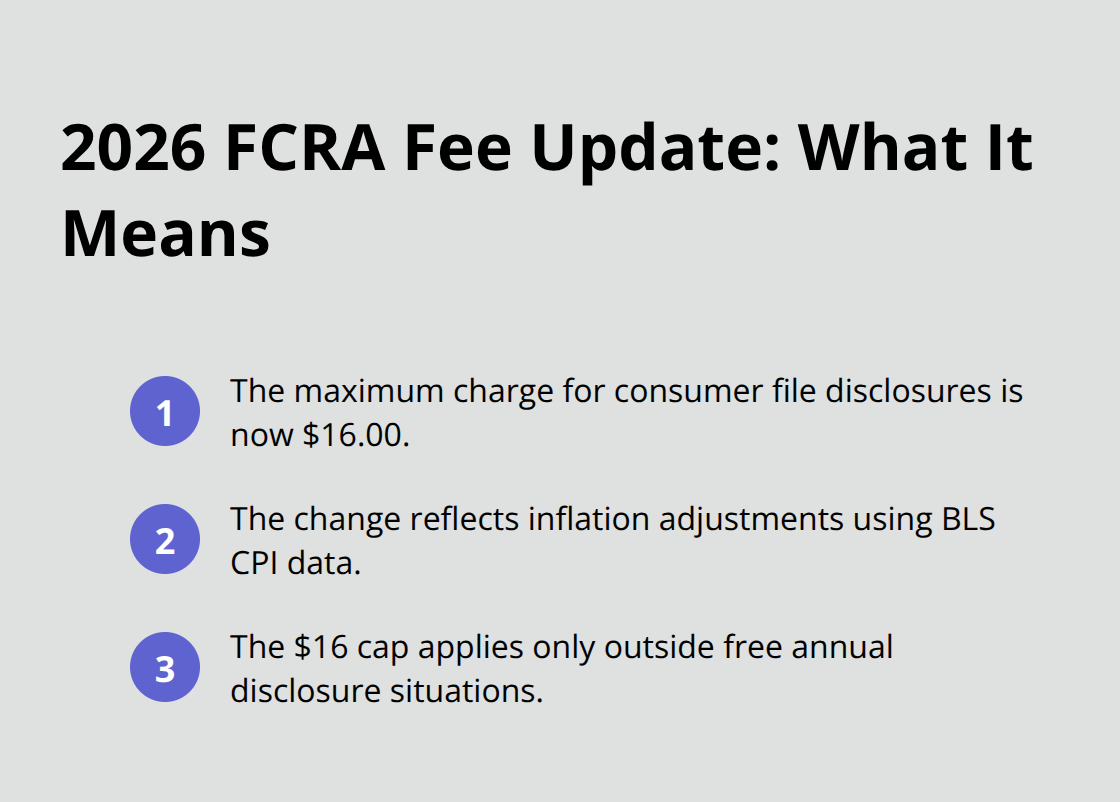

The CFPB finalized an update to Regulation V that took effect January 1, 2026, raising the maximum charge for consumer file disclosures from $15.50 to $16.00. This increase reflects inflation adjustments mandated by the Fair Credit Reporting Act since 1997, calculated using Consumer Price Index data from the U.S. Bureau of Labor Statistics. The $16 cap applies when you request a credit file disclosure outside the circumstances that qualify you for a free annual disclosure.

What matters most is understanding that you still have the right to one free file disclosure every 12 months from nationwide consumer reporting agencies like Equifax, Experian, and TransUnion. California residents can also access free weekly disclosures from these three bureaus, making routine credit monitoring entirely free if you plan strategically.

Medical Debt and Data Broker Changes

A federal court vacated the CFPB’s Medical Information Rule in July 2025, which means coded medical debt no longer faces federal restrictions in your credit reports (as long as the information does not identify your provider or reveal the nature of your medical services). Medical debt can still appear on your report, but furnishers and creditors cannot use certain restrictions that the rule would have imposed.

The CFPB also withdrew its proposed rule on data broker practices in May 2025, signaling a pullback from tighter federal oversight of how companies buy, sell, and use your personal data for now.

Free Disclosures Remain Your Best Tool

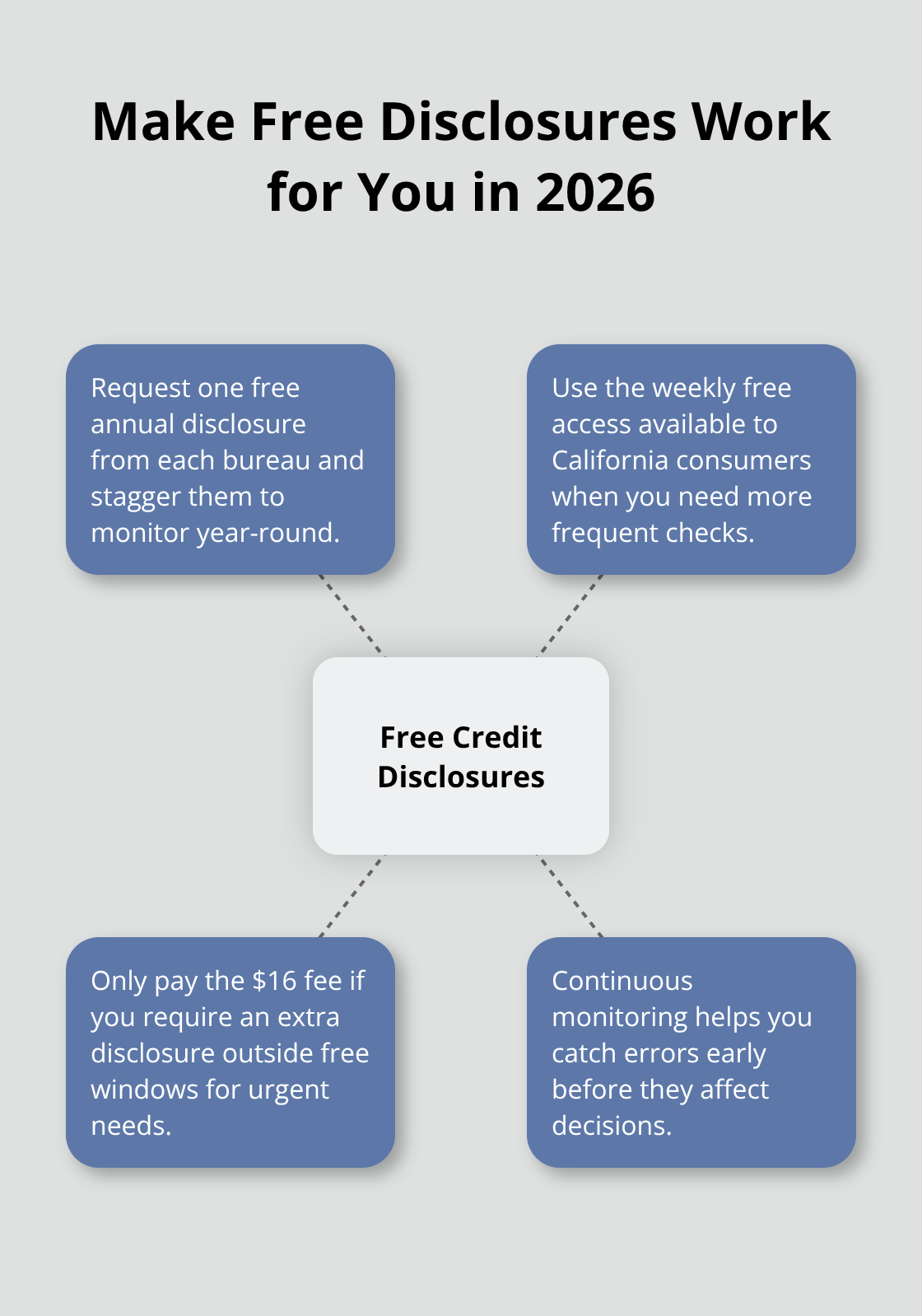

You can request a free annual disclosure from each of the three major bureaus and space these requests throughout the year for continuous monitoring without spending a dollar. If you need to check your credit file more frequently, the free weekly option provides access to all three bureaus simultaneously. Only pay the $16 fee if you have a genuine reason to obtain a disclosure outside these free windows-such as needing immediate proof of your credit file after discovering suspicious activity. The rising fee makes free disclosures even more valuable than before.

Your Dispute Rights Stay Strong

Your right to dispute inaccurate information has not weakened under 2026 changes. Furnishers of information to consumer reporting agencies still have a legal duty to investigate disputed information and correct errors, a requirement that has remained consistent under the Fair Credit Reporting Act. When you submit a dispute, you receive notice if an adverse action was taken based on your credit report (whether the adverse action involves credit, insurance, or employment decisions). The faster you identify errors through regular free disclosure reviews, the sooner you can initiate disputes and have them corrected.

Understanding these specific changes positions you to protect your credit file effectively in 2026. The next section explains how these updates directly affect your credit report and what impact they have on your financial standing.

How Your Credit Report Benefits From 2026 Changes

The 2026 FCRA updates improve your ability to monitor and correct your credit file without bearing the full cost of frequent reviews. The $16 maximum fee for non-free disclosures, while higher than 2025’s $15.50 cap, matters less than you might think because free access options eliminate the need for paid disclosures for most California residents. The three major bureaus-Equifax, Experian, and TransUnion-provide free weekly disclosures to all California consumers, so you can review your complete credit file fifty-two times per year at zero cost. This access fundamentally changes how errors affect your credit score. Errors that previously sat undetected for months now surface within days if you monitor strategically. A study by the FTC found that one in five consumers identified errors on their credit reports, and roughly one-third of those errors were significant enough to affect credit decisions. When you catch these errors faster through regular free reviews, you prevent them from damaging your score during the months they might otherwise remain hidden.

Spot Errors Faster and Dispute Immediately

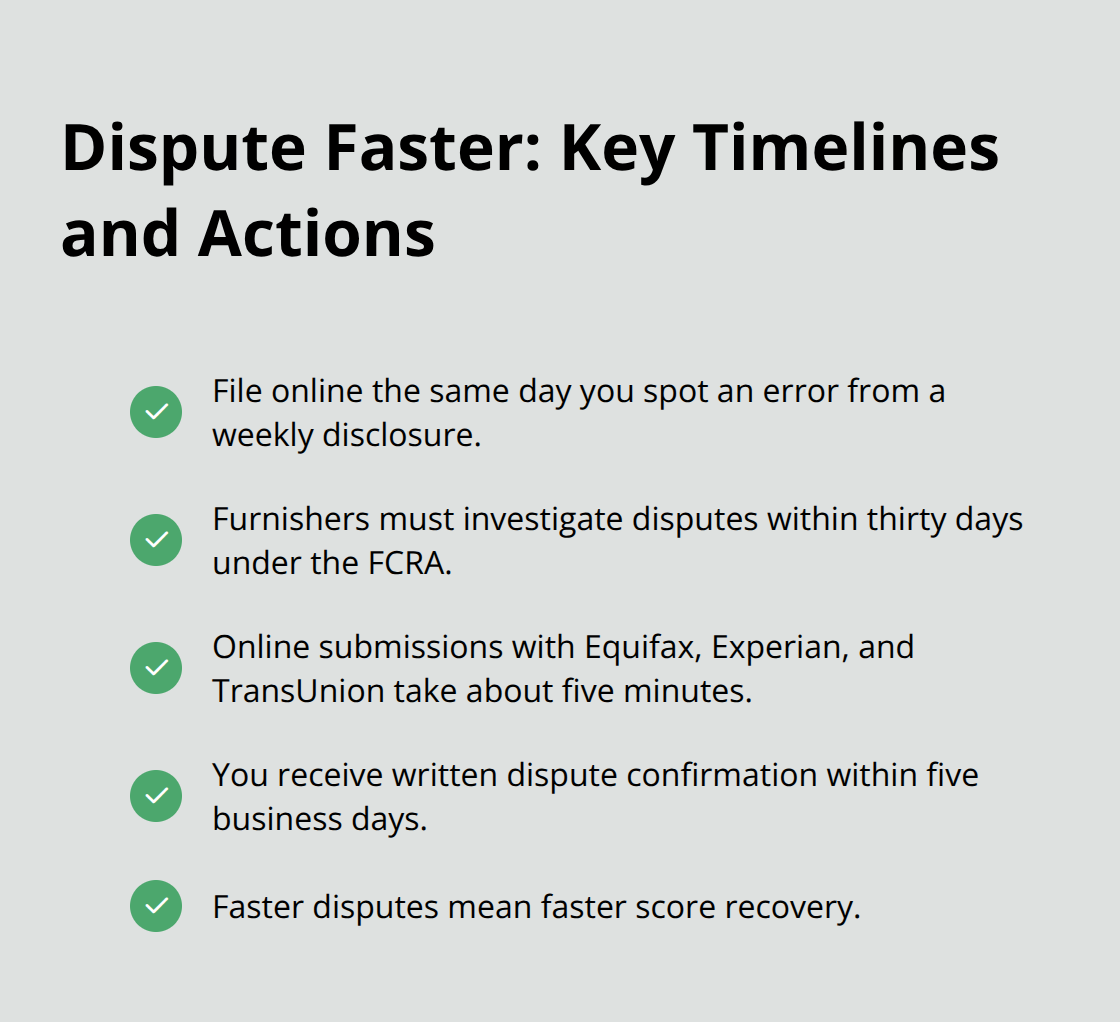

Furnishers must investigate disputed information within thirty days under existing FCRA requirements, but the real advantage in 2026 comes from your ability to initiate disputes immediately after spotting problems. If an error appears on your free weekly disclosure, you can file a dispute the same day rather than waiting for your annual free disclosure months later. This compressed timeline means errors get corrected faster, and your credit score recovers sooner. The CFPB emphasizes that furnishers have a duty to maintain reasonable procedures ensuring accuracy, so inaccurate accounts get removed or corrected more readily when disputes arrive promptly. Equifax, Experian, and TransUnion all accept disputes through their websites, taking roughly five minutes to file. The faster you dispute, the faster your score rebounds.

Identify Fraud and Unauthorized Accounts

Your credit file contains the specific data lenders, employers, and insurers use to make decisions about you. The free disclosure access in 2026 means you see exactly what decision-makers see before they see it. This transparency lets you identify not just errors, but also unfamiliar accounts you do not recognize-a sign of identity theft or fraud. The vacated medical debt rule means coded medical information can still appear on your report, so reviewing your file tells you whether medical debts are listed and whether they identify providers. This matters because some lenders treat medical debt differently than other debt, and knowing what appears on your file helps you understand how lenders might evaluate you. California consumers who check their files weekly catch unauthorized accounts within days rather than weeks, limiting fraud damage significantly.

Take Control of Your Credit Profile

Free weekly access transforms your credit file from a mystery into a tool you control. You no longer wait passively for errors to surface during a loan application or job interview. Instead, you actively shape what appears on your report by catching problems early and disputing them immediately. The combination of free disclosures and your unchanged right to dispute inaccurate information creates a powerful advantage in 2026. Your next step involves understanding exactly what rights you have when you spot problems and how to use them effectively.

Start Your Credit Review This Week

Access Your Free Disclosures Immediately

California residents have no reason to delay checking your credit file. Log into AnnualCreditReport.com, the official federal portal managed by Equifax, Experian, and TransUnion, and request your free annual disclosure from one bureau this week. Space your three free annual requests one month apart so you review your complete file quarterly without paying anything. If you want faster monitoring, visit each bureau’s website directly to access free weekly disclosures starting immediately. Most California consumers who implement this habit catch errors within two to four weeks of starting regular reviews. The FTC found that roughly 20% of consumers identified errors on their credit reports, but that percentage climbs significantly higher among people who actually review their files regularly. Your action this week sets the foundation for catching problems before they damage your credit score or expose you to fraud.

Spot Red Flags in Your File

When you review your disclosure, look for accounts you do not recognize, inquiries from lenders you never applied with, and incorrect personal information like wrong addresses or phone numbers. Medical debt may still appear on your file following the vacated medical information rule, so verify that any medical accounts listed are actually yours and not billing errors from healthcare providers. Unauthorized accounts signal identity theft or fraud, and catching them early prevents months of damage to your credit profile. The sooner you identify these red flags, the sooner you can take action to protect yourself.

File Disputes Without Delay

Dispute inaccurate information immediately through the bureau’s website rather than waiting for your next scheduled review. Furnishers have 30 days to investigate disputes under FCRA requirements, so starting disputes in January means corrections arrive by early February, keeping errors off your file during the critical months when lenders, employers, and insurers make decisions about you. The three major bureaus process disputes submitted online within minutes, and you receive written confirmation of your dispute within five business days. This rapid timeline means errors disappear from your report faster than ever before.

Protect Yourself With a Security Freeze

California law gives you additional protections beyond federal FCRA requirements, including the right to place a security freeze on your credit file at no cost, which prevents unauthorized accounts from opening in your name. Place a freeze with all three bureaus if you have experienced identity theft or suspect fraudulent activity. Remove the freeze temporarily when you actually apply for credit, then reinstate it afterward. This simple step eliminates most identity theft risk without blocking legitimate credit applications.

Final Thoughts

The 2026 FCRA updates shift your power from passive waiting to active control over your credit file. Free weekly disclosures let you catch errors, fraud, and inaccurate information within days instead of months, while furnishers still must investigate disputes within 30 days. Medical debt remains reportable and data brokers face fewer restrictions, but your core rights to dispute inaccurate information stay unchanged and strong.

Start reviewing your credit file this week using free disclosures, spot errors before they damage your score, and file disputes immediately when you find problems. The combination of free access and your unchanged dispute rights creates an advantage that previous generations of consumers never had. You no longer wait passively for problems to surface during a loan application or job interview.

If you discover errors on your credit report, identity theft, or unlawful debt collection practices, we at Bontrager Law represent California consumers in these matters against banks, collectors, and large corporations. Contact us at https://njb.legal/ to discuss your situation and learn how we can help you recover damages and protect your credit file.