A credit reporting error can wreck your finances without you even knowing it. Wrong information on your credit report leads to denied loans, higher interest rates, and years of financial struggle.

We at Bontrager Law help California residents fight back against these errors. Our free case review can show you exactly what’s damaging your credit and how to fix it.

How Credit Reporting Errors Destroy Your Financial Opportunities

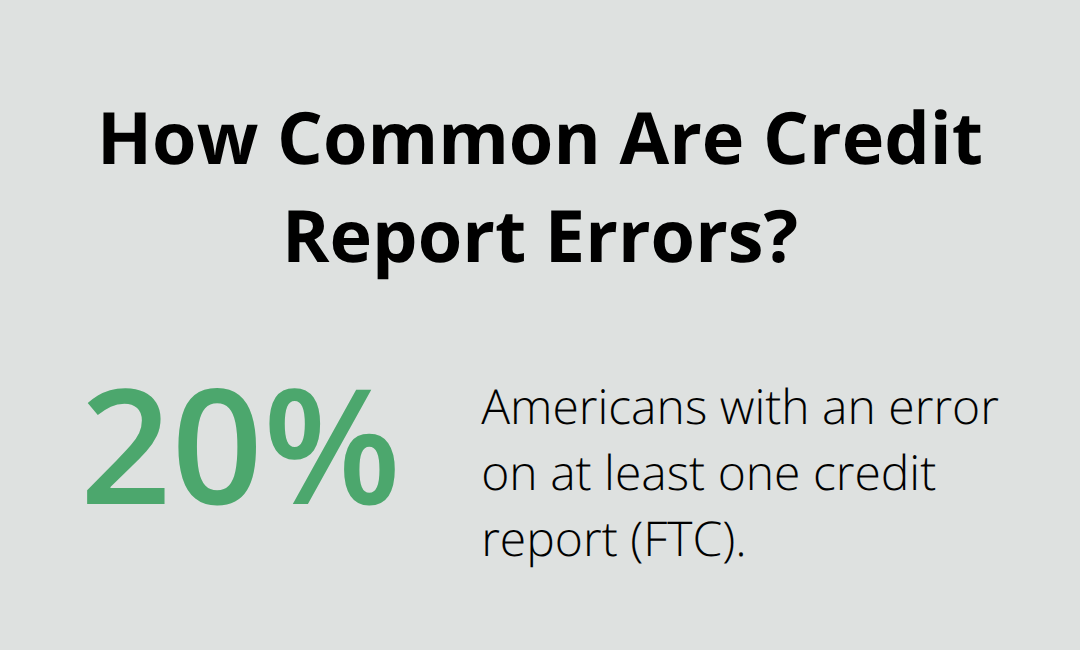

A single error on your credit report costs you thousands of dollars over your lifetime. When inaccurate information appears on your file, lenders view you as a riskier borrower than you actually are. Equifax, Experian, and TransUnion control the data that determines whether you qualify for mortgages, car loans, credit cards, and apartment rentals. According to the Federal Trade Commission, approximately one in five Americans has an error on at least one of their three credit reports. These errors range from accounts that don’t belong to you to late payments incorrectly reported as recent.

A single negative mark can drop your credit score by 100 points or more, depending on your current score and the severity of the error.

Your Score Determines Your Financial Future

Lenders use credit scores to decide whether to approve you and what interest rate to charge. If your report contains false information showing missed payments or high debt levels that aren’t actually yours, you’ll face rejection or predatory rates. A borrower with a 620 credit score pays approximately 2-3% more interest on a 30-year mortgage than someone with a 760 score. On a $300,000 home loan, that difference equals roughly $60,000 to $90,000 in additional interest payments over three decades. Credit bureaus rarely catch these errors on their own. They process millions of reports monthly and rely heavily on creditors to submit accurate information. When a creditor reports false data, the bureau adds it to your file without independent verification.

You Must Initiate the Dispute Process

You must start the dispute process yourself, which most people don’t know how to do effectively. Credit bureaus won’t remove errors without your formal challenge. The process requires documentation, persistence, and knowledge of your rights under the Fair Credit Reporting Act. Most consumers attempt one dispute, receive a rejection, and then give up. This passivity allows false information to remain on your report indefinitely, continuing to damage your financial opportunities.

Debt Collectors Weaponize Reporting Errors

Many credit reporting errors originate from debt collection agencies that purchase old accounts and report them incorrectly. Some collectors deliberately report false information knowing that most consumers won’t fight back. They count on your lack of awareness regarding your rights under the Fair Credit Reporting Act and the California Consumer Financial Protection Law. When you contact a collector to dispute an error, they typically ignore you unless you have legal representation. The DFPI expanded consumer protections on January 1, 2026, through SB 825, which now allows action against unlawful practices by previously unregulated debt-relief and credit repair companies. This expansion creates more pathways to hold bad actors accountable, but you need someone who understands these laws to navigate them. Without professional support, collectors continue reporting false information while your credit deteriorates month after month. Understanding what legal options exist to fight back becomes your next critical step.

How to Fix Credit Reporting Errors

File a Formal Dispute With Documentation

Filing a dispute with a credit bureau requires more than a simple complaint. The Federal Trade Commission allows you to challenge inaccurate information directly with Equifax, Experian, or TransUnion, but your dispute must include specific documentation proving the error exists. Gather your bank statements, payment records, or correspondence showing the discrepancy rather than simply claiming an account isn’t yours or a payment date is wrong. Send your dispute in writing to the credit bureau’s dispute department, not their general customer service line. Include copies of your supporting documents and a clear explanation of what’s inaccurate. Credit bureaus have 30 days to investigate, though many take longer. If they don’t verify the information within that window, they must remove it.

The verification process often fails consumers. Many bureaus claim they verified the error when they actually contacted the creditor who reported it, and that creditor simply confirmed their original report. This circular verification accomplishes nothing for you. When the bureau denies your dispute, you have the right to add a consumer statement to your file, but that statement rarely influences lending decisions.

Send a Cease and Desist Letter to Stop Unlawful Reporting

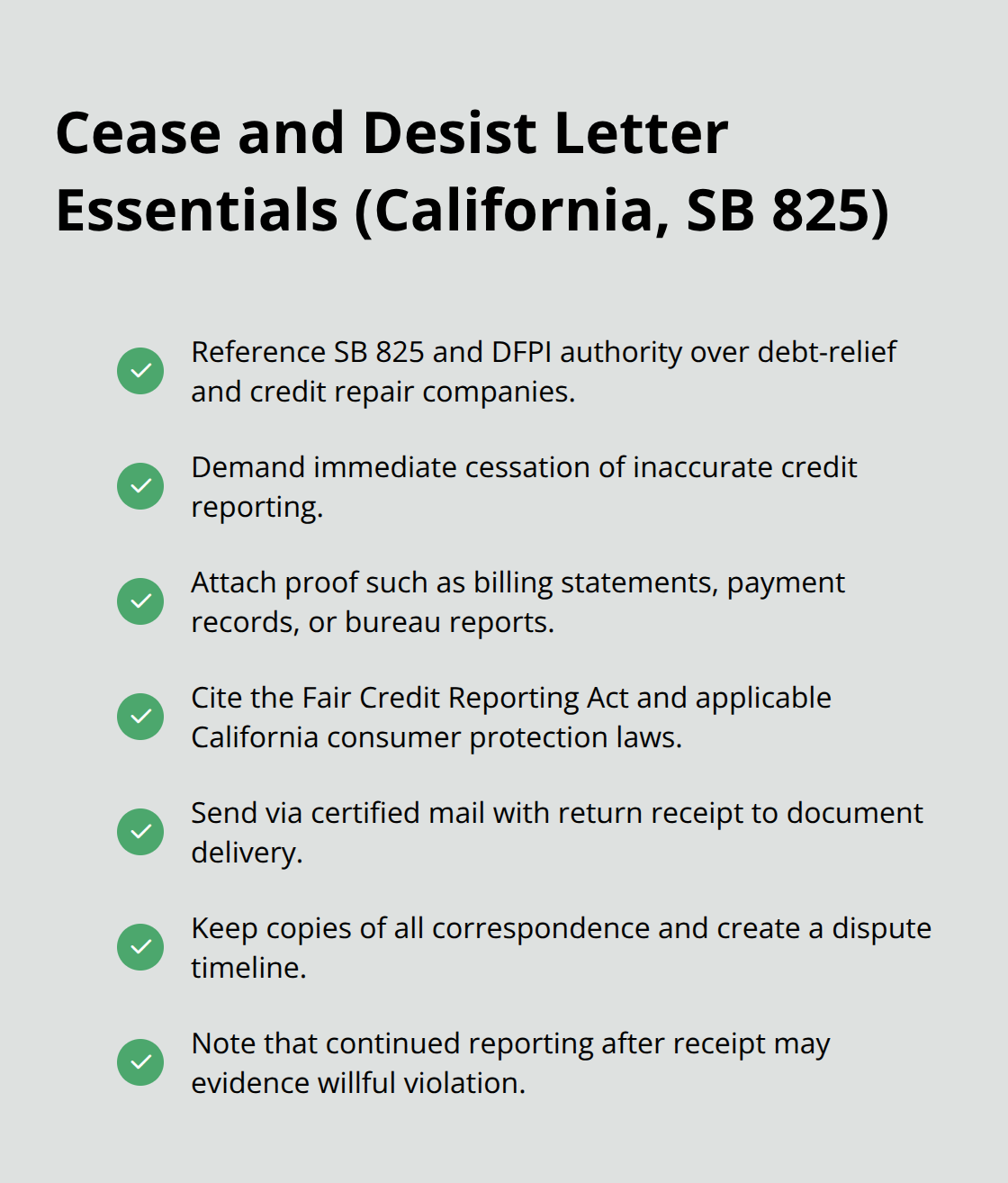

Debt collectors often ignore consumer disputes because they operate under the assumption that most people won’t follow through legally. A cease and desist letter forces them to acknowledge your complaint and creates a paper trail for potential legal action. California’s expanded consumer protections under SB 825 (effective January 1, 2026) give the Department of Financial Protection and Innovation authority to take action against unlawful practices by debt-relief and credit repair companies that were previously unregulated.

Your cease and desist letter should reference this law and demand that the collector stop reporting the inaccurate information immediately. Include copies of documents proving the error appears on your credit report and explain why their reporting violates consumer protection statutes. Send the letter via certified mail with return receipt so you have proof of delivery. If the collector continues reporting after receiving your letter, you have evidence of willful violation that strengthens any future legal claim.

Know When Professional Intervention Becomes Necessary

At this point, consulting with a firm experienced in California consumer protection law becomes your strongest move. A firm that handles these cases regularly can determine whether the collector’s actions violate the Fair Credit Reporting Act or California’s consumer protection statutes, opening pathways to compensation you wouldn’t access alone. The difference between handling this yourself and having professional representation often determines whether you recover damages or simply remove the error from your report.

Why You Need Legal Help for Credit Recovery

Handling credit reporting errors alone puts you at a fundamental disadvantage. Debt collectors operate under a simple calculation: most consumers won’t pursue legal action, so ignoring disputes costs them nothing. When you send a cease and desist letter without legal representation, collectors often view it as a bluff. They’ve seen thousands of consumer complaints and know that few people follow through with actual litigation.

How Legal Representation Changes Collector Behavior

The moment a collector realizes you have legal representation, their behavior shifts dramatically. They stop ignoring your communications because they understand that continued violations now carry financial consequences. This change happens not because your underlying facts altered, but because the threat of legal accountability suddenly becomes real. Collectors know that a firm experienced in consumer protection law can document violations and file claims for statutory damages and attorney fees.

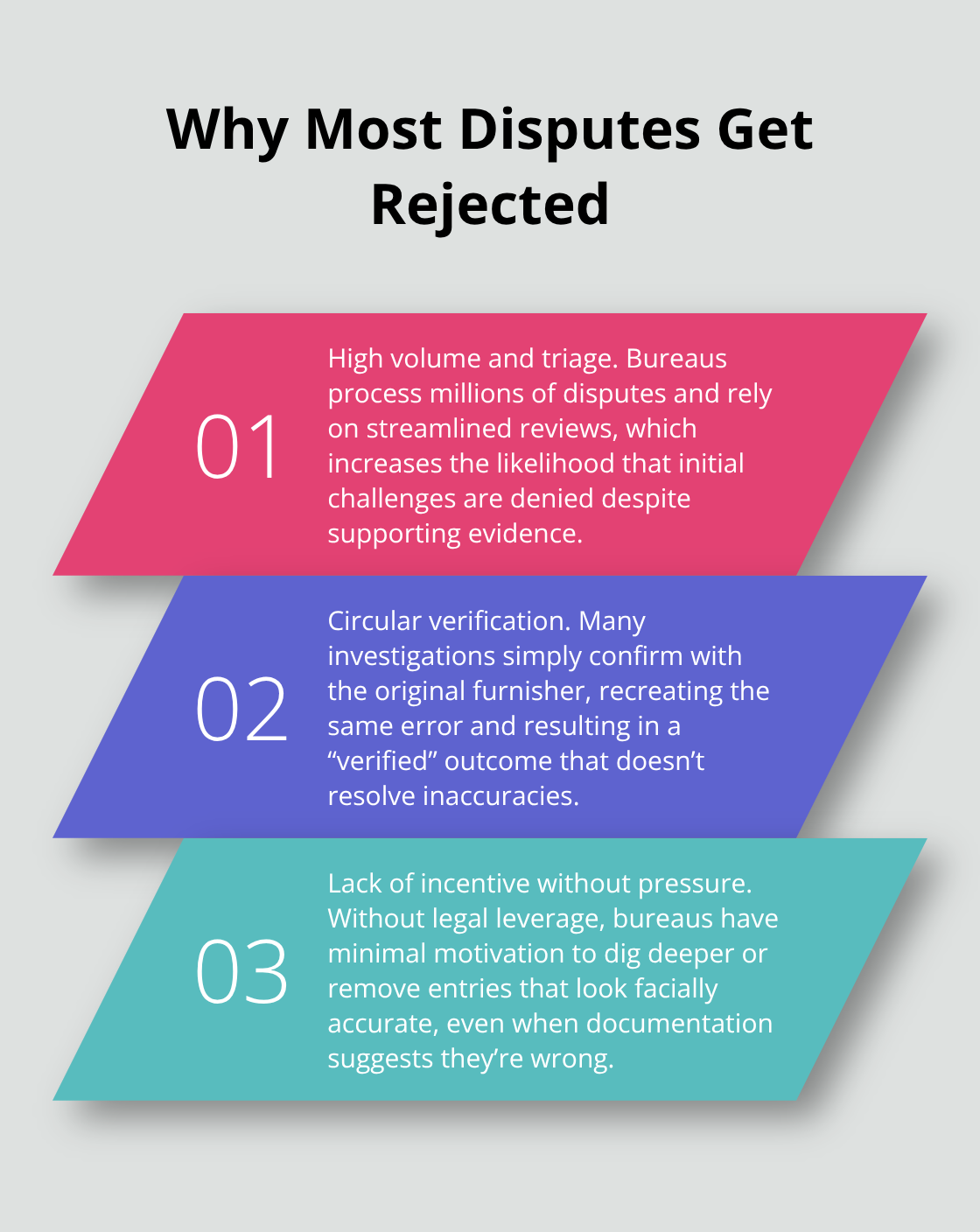

Why Credit Bureaus Reject Most Disputes

Credit bureaus process millions of disputes annually and reject most of them. According to data from consumer advocacy groups, bureaus uphold their initial decision in the majority of first disputes, forcing consumers to file appeals or abandon their cases entirely. The verification process they use often amounts to contacting the creditor who reported the error in the first place, creating a circular confirmation that accomplishes nothing for you. Without legal pressure, bureaus have zero incentive to conduct thorough investigations or remove accurate-looking entries, even when substantial evidence supports their removal.

What Legal Tools Actually Accomplish

The Fair Credit Reporting Act and California’s expanded Consumer Financial Protection Law under SB 825 give you powerful legal tools, but only if someone knows how to wield them effectively. A firm experienced in these cases can identify whether a collector’s behavior constitutes willful noncompliance, which opens the door to statutory damages and attorney fees-compensation that solo disputes never generate. The difference between your own efforts and professional representation often means the difference between removing an error and recovering thousands in damages from the entity that caused the harm.

Taking Action With Professional Support

We at Bontrager Law represent individuals across California in disputes over credit reporting errors and unlawful debt collection. Our free case review can show you whether your situation qualifies for legal action and what compensation you might recover. The experience of handling thousands of claims across California reveals patterns that solo consumers never see-tactics collectors use, verification shortcuts bureaus take, and violations that courts recognize as willful noncompliance.

Final Thoughts

Credit reporting errors will not fix themselves, and waiting only allows damage to compound. California’s expanded consumer protection laws under SB 825 give you legal weapons that did not exist before January 1, 2026, and the Department of Financial Protection and Innovation now oversees previously unregulated debt-relief and credit repair companies. These laws exist to protect you, but only if someone with knowledge of consumer protection statutes applies them to your situation.

A free case review CA with Bontrager Law shows you exactly what damages your credit and whether your situation qualifies for legal action. With nearly 20 years of experience handling thousands of claims across California, we identify patterns that solo consumers never see and represent individuals in disputes over credit reporting errors, identity theft, unlawful debt collection, and related claims against banks, collectors, and large corporations. This experience reveals which violations courts recognize as willful noncompliance and what compensation you might recover.

The difference between handling this alone and having professional representation often determines whether you simply remove an error or recover thousands in damages from the entity responsible. Your rights under California law are substantial, but exercising them effectively requires someone who understands how collectors operate and how bureaus cut corners. Contact Bontrager Law today for your free case review and take control of your financial future.