Your credit report affects major financial decisions-from mortgage approvals to job offers. Errors on that report can derail your plans, yet many credit reporting agencies fail to investigate disputes properly or remove outdated information.

At Bontrager Law, we help Californians understand their rights under the Fair Credit Reporting Act and hold agencies accountable when they violate them. This guide walks you through what the FCRA protects, common violations, and how to dispute inaccurate information on your credit file.

What the FCRA Actually Protects

Your Right to Accurate Information

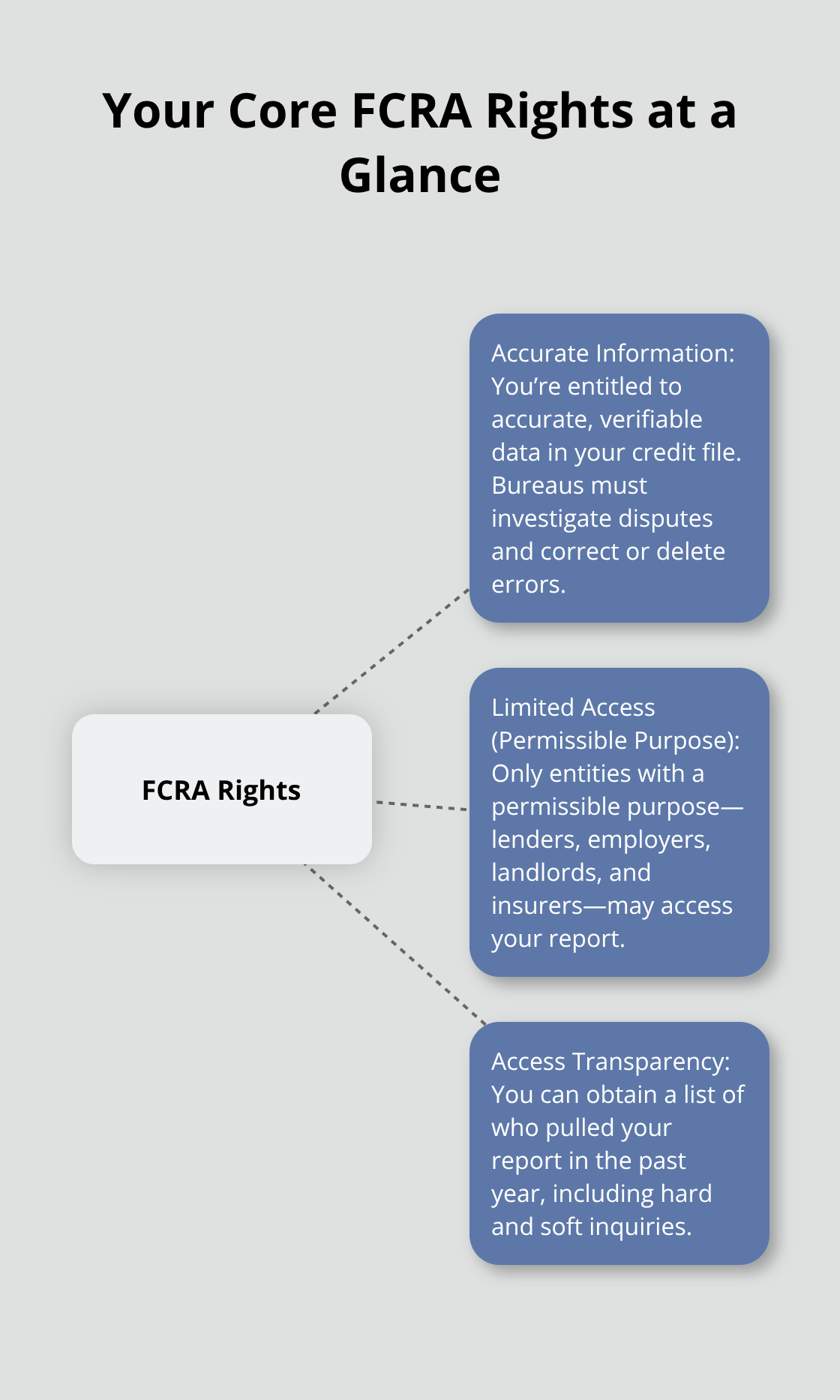

The Fair Credit Reporting Act gives you three core protections that matter most when dealing with credit reporting agencies. First, you have the right to accurate information on your credit file. The FCRA requires credit bureaus like Equifax, Experian, and TransUnion to maintain reasonable procedures to verify information before reporting it and to investigate disputes within 30 days. When you report an error, the bureau must contact the data furnisher, review the information, and correct or delete inaccurate items. Many agencies ignore this obligation entirely, which is why disputes often fail.

Protection Against Unauthorized Access

Second, you have protection against unauthorized access. Credit bureaus can only provide your report to entities with a permissible purpose under the FCRA-lenders, employers, landlords, insurers, and similar parties. They cannot sell your report to anyone who asks or use it for purposes unrelated to credit, employment, insurance, or housing decisions. This restriction exists because your credit file contains sensitive financial information that affects your ability to borrow, work, and secure housing.

The Right to Know Who Accesses Your File

Third, you have the right to know who has accessed your file. You can request and receive a disclosure showing everyone who has pulled your report in the past year, including hard inquiries that may affect your credit score and soft inquiries that do not. This transparency allows you to spot unauthorized access or suspicious activity before it causes further damage.

When Violations Trigger Liability

What makes these protections actionable is knowing when agencies violate them. Equifax, Experian, and TransUnion handle reports for millions of consumers, yet disputes often go unanswered or receive form-letter responses without real investigation. If a bureau fails to investigate within 30 days, ignores documentation you provide, or refuses to remove information after you dispute it, that violation can trigger statutory damages under the FCRA. Willful violations can result in damages ranging from $100 to $1,000 per violation, and class actions have recovered millions when agencies fail to follow proper procedures.

Your Access to Free Reports and Adverse Action Notices

The FCRA also requires bureaus to provide you a free copy of your report annually through AnnualCreditReport.com, and you can obtain additional copies if you dispute information or experience adverse action based on your report. If a lender denies you credit, a landlord rejects your application, or an employer does not hire you based on your credit report, the entity must notify you and provide the bureau’s contact information so you can investigate the accuracy of the report used against you. Understanding these violations and your rights positions you to take action when agencies fail to meet their legal obligations-which brings us to the specific violations that occur most frequently.

Common FCRA Violations by Credit Reporting Agencies

Bureaus Fail to Investigate Disputes Properly

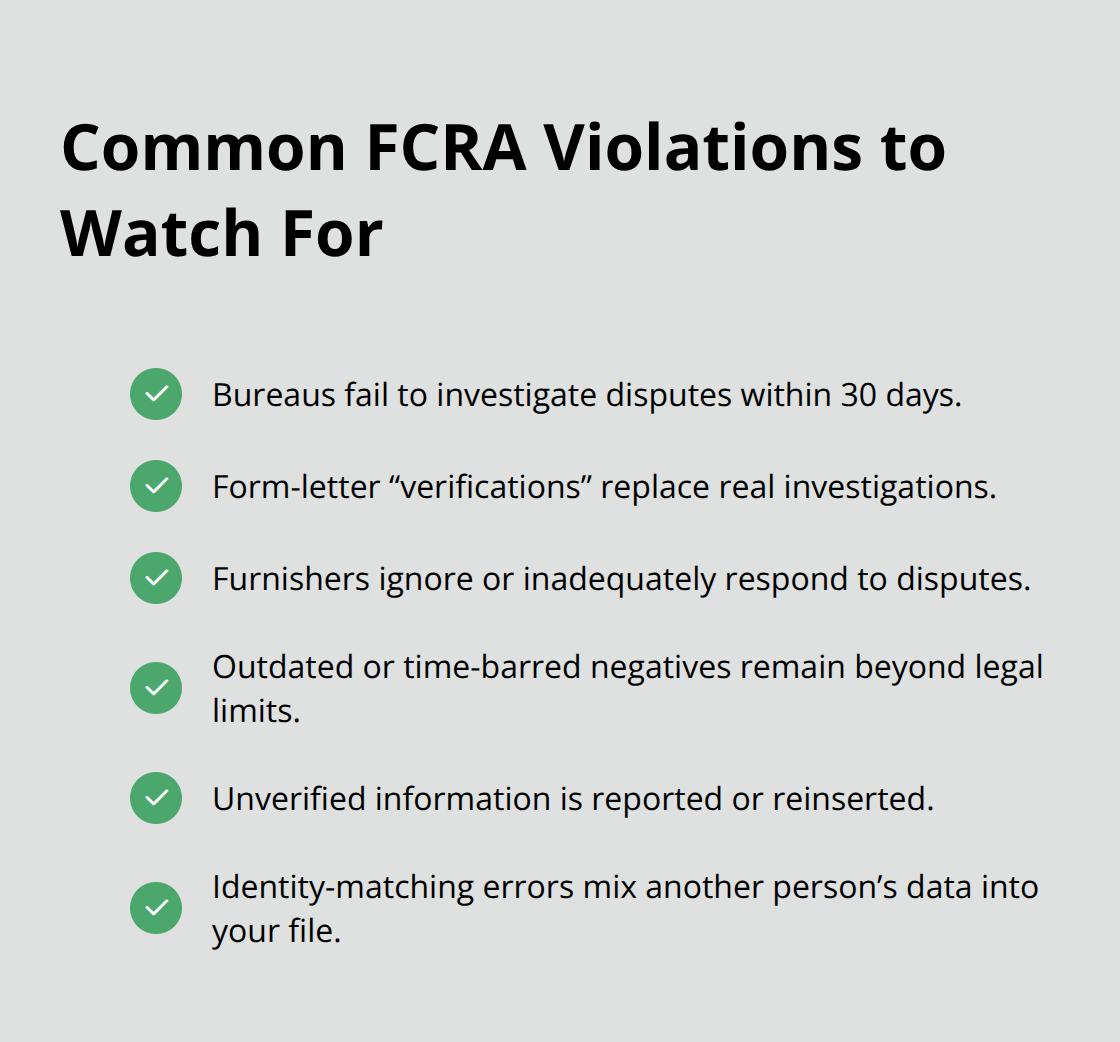

The 30-day investigation window exists for a reason. When you dispute an item on your credit report, the FCRA requires the bureau to contact the data furnisher, review your documentation, and resolve the dispute within 30 days. In practice, Equifax, Experian, and TransUnion often send generic form letters to furnishers without reviewing the evidence you submitted. The Federal Trade Commission has documented repeated failures where bureaus marked disputes as investigated without contacting the furnisher at all.

Many consumers report receiving closure notices stating the item was verified when no actual investigation occurred.

This pattern reflects how the three major bureaus process millions of disputes annually. Their systems prioritize speed over accuracy. When a bureau fails to investigate properly, that violation qualifies as willful under the FCRA, and you can pursue damages of $100 to $1,000 per violation. The Hebert v. Barnes & Noble case demonstrates how courts view corporate negligence in compliance matters-even when a company reviews its practices with legal counsel, failure to update procedures proactively can establish willfulness.

Data Furnishers Ignore Their Own Obligations

Furnishers bear responsibility alongside bureaus. Data furnishers must investigate disputes about information they provide to credit bureaus and correct or delete inaccurate data. Many furnishers ignore dispute requests entirely or respond without verifying the account details you questioned. If a furnisher fails to investigate or respond, the bureau should remove the item after 30 days. Instead, some bureaus reinsert unverified information into your file months later, creating a cycle where the same error reappears.

Inaccurate and Outdated Information Persists

Inaccurate and outdated information remains on credit files far longer than it should. Items with payment history errors, incorrect account balances, or accounts marked as delinquent when you paid on time damage your credit score and deny you access to credit at reasonable rates. The FCRA requires bureaus to remove information that is inaccurate, unverified, or older than the legal reporting period-typically seven years for negative items and ten years for bankruptcy. Yet many bureaus report charged-off accounts, late payments, and collection accounts well past these dates.

When you request removal of time-barred information, bureaus often ignore the request or claim the furnisher verified it without conducting independent review. Furnishers also fail to update information when accounts are resolved. If you pay a collection account in full, the furnisher should report the status as paid-in-full, but many report it as unpaid or do not update the status at all.

Verification Failures Allow Wrong Information to Spread

These failures compound when bureaus lack verification procedures. Before initially reporting information, furnishers should verify account details match your identifying information and that the debt belongs to you. Mistakes in Social Security numbers, account numbers, or identity matching lead to information appearing on your file incorrectly. If you have a common name, similar account numbers may be mixed with your file. Furnishers often report information without this basic verification step, and bureaus accept it without question.

Taking action requires documentation of each failure and clear communication with the bureau about what you are disputing and why. The patterns we observe repeatedly show bureaus treating disputes as administrative tasks rather than legal obligations and furnishers reporting information without verification. A credit protection attorney can help you identify violations in your file and take the next step-filing a formal dispute that creates a documented record of the bureau’s response.

How to File and Win Your Credit Report Dispute

Send Your Dispute in Writing with Proof of Delivery

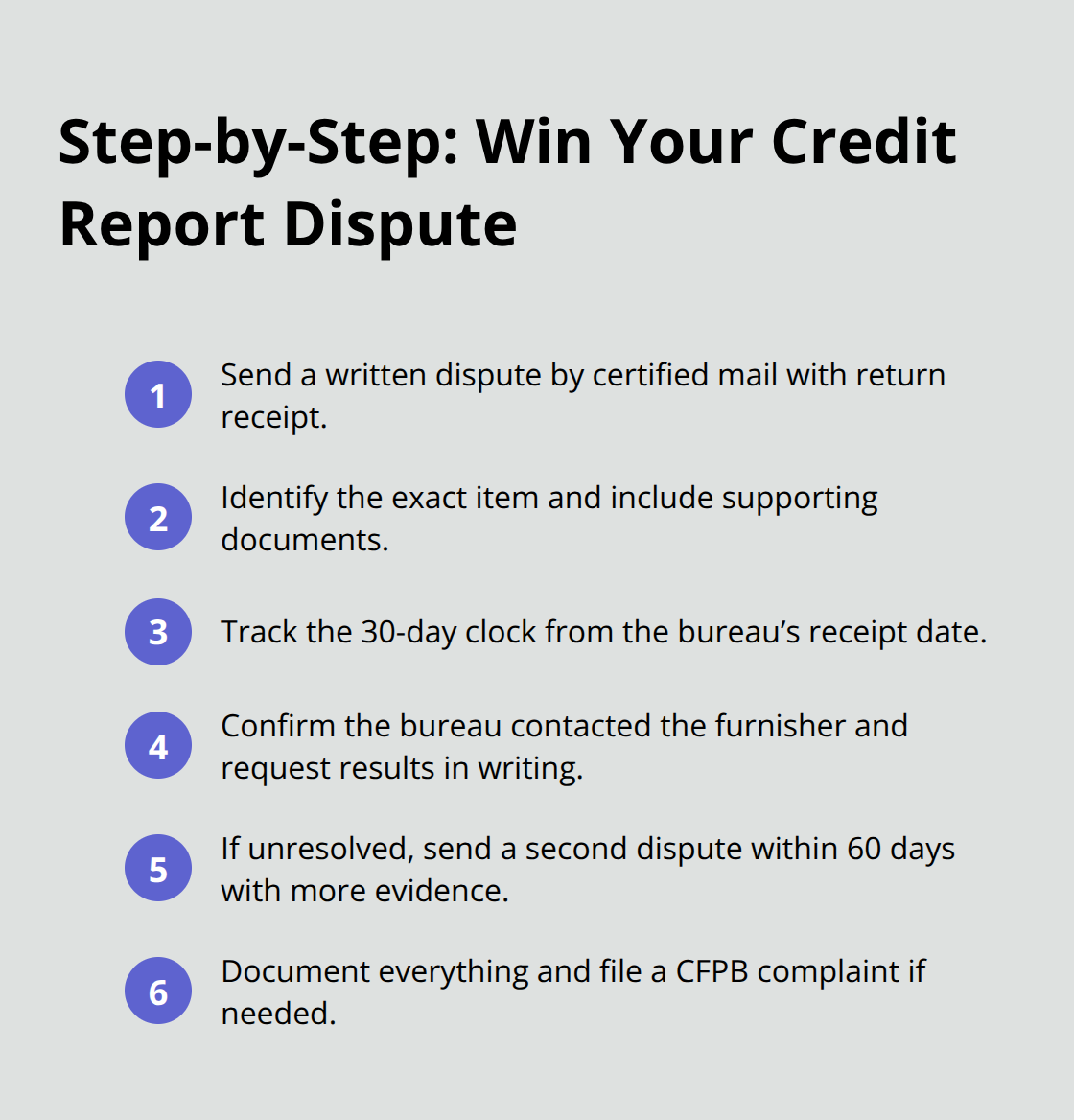

Start with a written dispute letter sent directly to the credit bureau by certified mail with return receipt requested. The Federal Trade Commission requires bureaus to accept disputes in writing, and certified mail creates proof that your dispute arrived on a specific date-critical if the bureau later claims it never received your challenge. Address your letter to the bureau’s dispute department, not a general customer service line. Equifax, Experian, and TransUnion each maintain separate dispute addresses on their websites.

In your letter, identify the specific item you dispute and explain why it is inaccurate or outdated. State whether the account does not belong to you, the balance is wrong, the payment status is incorrect, or the item exceeds the seven-year reporting period. Include copies of documents that support your claim-bank statements showing payment, correspondence with the creditor, proof the account was closed, or evidence the debt was settled. Do not send originals; bureaus lose documents routinely. Attach a cover page listing each document so the bureau cannot claim items went missing.

The 30-day investigation window begins when the bureau receives your letter, not when you mail it. The certified receipt proves your start date and protects you if the bureau later claims it received your dispute late.

Verify the Bureau Contacted the Data Furnisher

Once you file a dispute, the bureau must contact the data furnisher and request verification within five business days. If the furnisher cannot verify the information, the bureau must remove it. Most bureaus fail at this step-they either skip contacting furnishers altogether or accept vague responses without pressing for actual verification.

After 30 days, request written confirmation of the investigation results. If the bureau removed the item, ask for an updated credit report showing the deletion. If it kept the item, the bureau must include your dispute statement in your file. This written confirmation creates a record of what the bureau claims to have investigated.

File a Second Dispute if the First Investigation Fails

If nothing changed and you believe the investigation was inadequate, send a follow-up letter within 60 days stating the investigation was incomplete and requesting reinvestigation with your additional documentation. This second dispute creates a second 30-day window and stronger evidence of the bureau’s indifference if it again fails to correct the error.

The pattern of ignored disputes-first investigation, then reinvestigation, both producing no results-demonstrates willful violation under the FCRA. Courts recognize this pattern as evidence that the bureau treated your dispute as an administrative task rather than a legal obligation.

Document Everything and File a Complaint

Track all correspondence with dates and reference numbers. Save copies of your dispute letters, the certified mail receipts, the bureau’s responses, and any documents you submitted. This documentation becomes essential if you later pursue legal action or file a complaint with the Consumer Financial Protection Bureau.

The CFPB accepts complaints about credit bureaus, and documented patterns of ignored disputes strengthen your position significantly. When you file a complaint, reference the specific dates your disputes were sent, the dates the bureau responded (or failed to respond), and the items that remain uncorrected. The CFPB shares complaint data with the Federal Trade Commission and state attorneys general, creating pressure on bureaus to improve their dispute-handling processes.

Final Thoughts

Your credit file shapes your financial future, and the FCRA gives you concrete rights to protect it. You can demand accurate information, challenge errors within 30 days, and hold credit bureaus accountable when they ignore your disputes. California FCRA compliance requires bureaus to investigate properly, furnishers to verify before reporting, and both parties to correct mistakes without delay.

The violations we outlined-failed investigations, unverified information, outdated items that persist-happen repeatedly because bureaus treat disputes as volume operations rather than legal obligations. Your documentation of each failure strengthens your position significantly, and certified mail receipts, written dispute letters, and the bureau’s responses create a record that courts recognize as evidence of willful violation. Statutory damages under the FCRA range from $100 to $1,000 per violation, and class actions have recovered millions when agencies fail systematically.

You should pursue legal help when a bureau ignores your dispute after 30 days, when reinvestigation produces no results, or when inaccurate information continues damaging your credit score. We at Bontrager Law represent Californians in credit reporting disputes, identity theft claims, and related consumer protection matters, and we can identify whether your situation qualifies for damages and handle communication with the bureau on your behalf. Contact us for a free case review to discuss your credit report errors and take action now.